Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

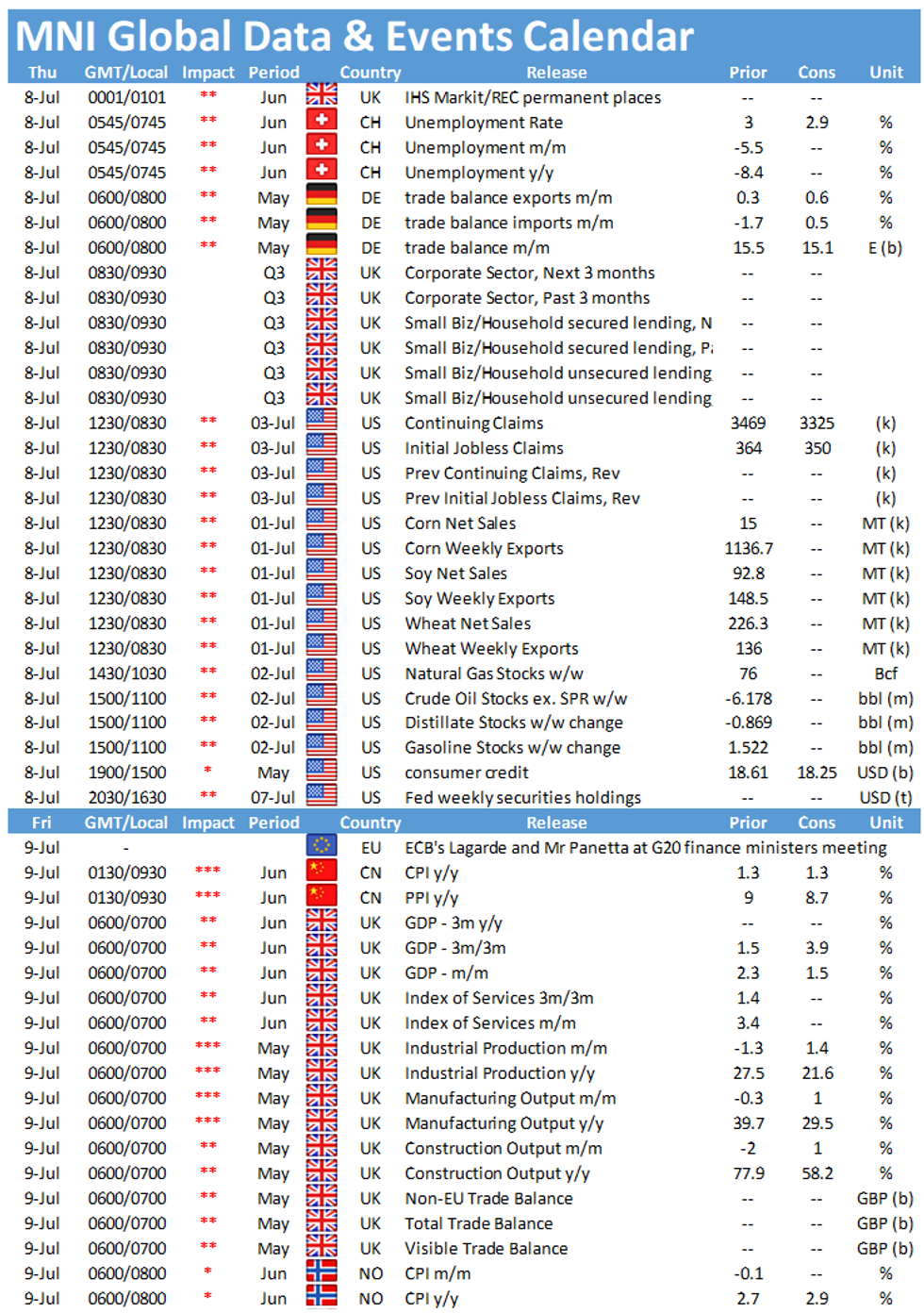

Thursday sees a quiet data schedule in terms of European releases, with the highlights being the publication of Swiss unemployment at 0645BST, followed by the German trade balance at 0700BST. In the US, the release of the initial jobless claims will be watched closely again.

Swiss jobless rate seen lower

The Swiss unemployment rate is forecast to ease further in June to 2.9%, down from 3.0% recorded in May, as the economy is gradually reopening. While the number of unemployed people is steadily declining, vacancies are rising, indicating the ongoing recovery of the labour market. The KOF Consensus Forecast suggests a better development of the labour market than previously expected. In their June survey they expect unemployment to rise by 3.1% in 2021 and by 3.0% in 2022, up from 3.6% and 3.3%, respectively.

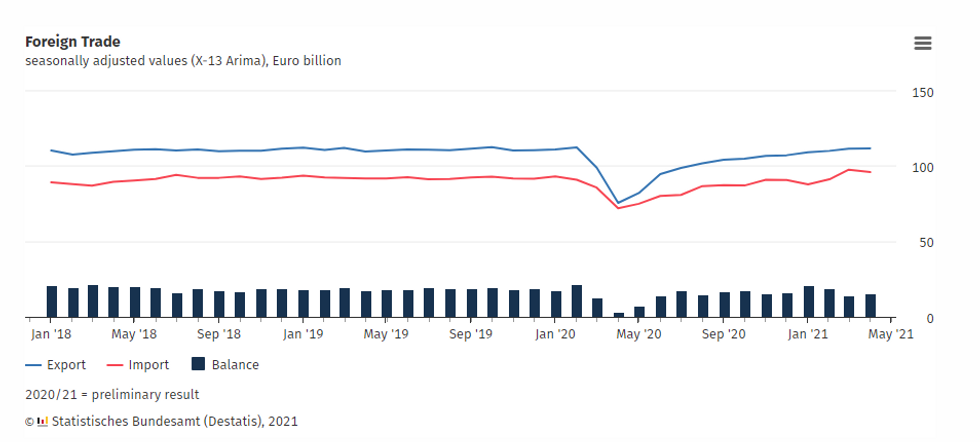

German trade surplus forecast to narrow

The German trade surplus stood at EUR 15.5bn in April and markets look for a small decline to EUR 15.4bn in May. Monthly exports rose 0.3% in April, while imports declined by 1.7%. Annual exports (47.7%) as well as imports (33.2%) surged in April, which was mainly due to base effects. In May, market analysts project monthly exports to rise further by 0.5% and imports are forecast to rebound to 0.4%.

Survey evidence indicates an uptick in export business. The services PMI noted that export orders returned to growth in June as travel activity was picking up, while the manufacturing PMI stated that export orders remained historically high.

Source: Destatis

US jobless claims seen lower

U.S. jobless claims filed through July 3 should decrease modestly, with Bloomberg forecasting a modest decline to 350,000 from 364,000 through June 26, a new pandemic low. Continuing claims filed through June 26 are expected to ease to 3,325,000, after recording 3,469,000 through June 19.

The labour market continues to recover, indicated by the latest labour report showing that nonfarm payrolls increased by more than markets expected.

The events calendar remains quiet with no speeches scheduled for the day.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.