Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

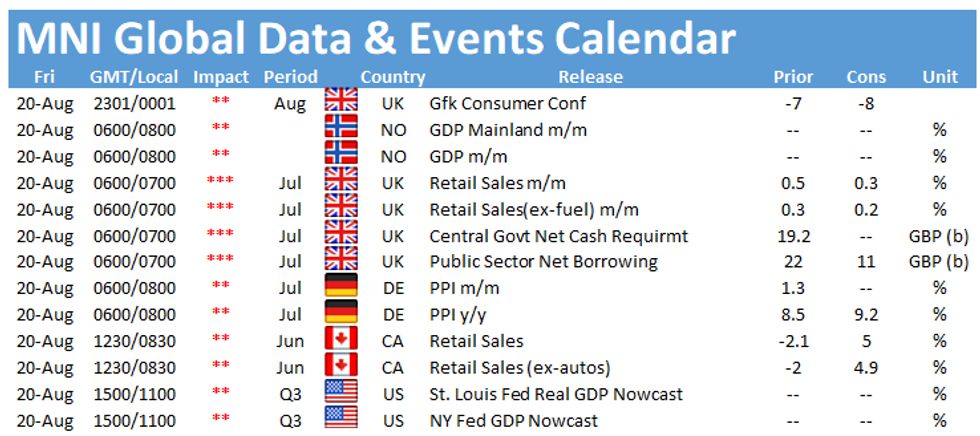

Friday sees a quiet end to the week, with the early UK data the session's highlight.

UK borrowing seen lower (Friday, 0700 BST)

UK public sector borrowing may have slipped as low as GBP 11.5 bn in July, the smallest since since January, when self-assessment tax receipts pushed borrowing to just GBP1.5 bn, and the second lowest level since March 2020. That would leave borrowing well below the OBR's GBP15.6 bn forecast, continuing a pattern of below-expected borrowing numbers.

June PSNB-ex banks of GBP22.754 bn was elevated by a 223% annual rise in index-linked Gilt interest payments by GBP6 bn to GBP8.7 bn, a sum unlikely to be replicated in July. June interest payments were derived from the change in RPI between March and April, when the index nearly doubled to 2.9% from 1.5%. RPI rose to 3.9% in June, translating into increased interest payments of just GBP1.6 bn more than a year ago.

Borrowing will again be inflated by a GBP 800 mn Brexit payment to the EU following a bill received in April. Last month, ONS officials warned of similar disbursements in August and September, when a new bill will be issued. Economists will also keep an eye on revisions to June borrowing, originally reported at GBP 22.754 bn, as data have been revised lower in every month of the calendar year, by GBP3.7 bn in June and GBP5.6 bn in May.

UK retail sales seen modestly higher (Friday 0700 BST)

UK retail sales likely rose modestly in July, extending a marginal increase seen in June, with clothing sales reviving as social events return to the summer calendar, key industry leaders told MNI.

Helen Dickinson, the CEO at the British Retail Consortium said July continues to see strong sales, albeit at a slower pace as lifting restrictions didn't bring an anticipated in-store boost. However, "with social events back on for the summer calendar, formalwear and beauty all began to see notable improvement," she said.

City analysts forecast a 0.3% gain between June and July, after a higher-than-expected 0.5% m/m improvement in June, and a 1.4% decline in May.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.