MNI (LONDON) - Highlights:

- NZD slips to new YTD lows against AUD as RBNZ switches language

- JPY trade-weighted index at new lows, keeping pressure on carry trades

- BoE's Pill set to speak, could hold decisive vote at August MPC meeting

US TSYS: Rally Builds As US Filters In, Powell Part Two and 10Y Supply Headline

- Treasuries have bull flattened overnight, with moves driven by a larger rally in EGBs with the same flattening bias and mild spillover from a dovish RBNZ.

- Cash yields sit 1-2.5bp lower on the day, with 2s10s at -34.1bp (-1.3bps) reversing yesterday’s increase. Both 2Y and 10Y yields approach recent lows seen after Friday’s payrolls report but remain off prior March lows.

- TYU4 has lifted to 110-18+ (+ 05+) on solid cumulative volumes of 330k. Resistance is watched at Monday’s high of 110-20+ before a more important bull trigger at 111-01 (Jun 14 high), whilst support is seen at 109-28+ (50-day EMA).

- Today’s session should be affected by tomorrow’s CPI report looming on the horizon (preview), whilst the 10Y re-open provides interest later on (before further supply with the 30Y tomorrow). Yesterday’s 3Y stopped through by 0.6bps along with a sharp increase in the bid-to-cover.

- Data: MBA weekly mortgage data (0700ET), Wholesale sales/inventories May/May f (1000ET)

- Fedspeak: Powell speaks to the House committee (1000ET), Goolsbee & Bowman on childcare opening remarks (1430ET), Cook on global monetary policy (1930ET) – see STIR.

- Note/bond issuance: US Tsy $39B 10Y Note re-open auction (1300ET)

- Bill issuance: US Tsy $60B 17W Bill auction (1130ET)

STIR: Day Two Of Powell Before Governor Cook Late On

- Fed Funds implied rates are almost unchanged from yesterday’s close, having ticked a touch higher after Powell to only slightly trim last week’s sizeable decline on softer labor data - table below.

- Cumulative cuts from 5.33% effective: 1bp Jul, 19.5bp Sep, 30bp Nov, 50bp Dec and 66bp Jan.

- Chair Powell speaks in day two of the semiannual testimony, this time to the House with the Q&A watched in the low likelihood of any surprises.

- Powell yesterday failed to provide a meaningfully dovish deviation vs. recent remarks, perhaps disappointing some who were looking for a bolder dovish tone in the wake of the recent run of soft labor market and economic activity data, although he did acknowledge that the labor market is now fully back in balance.

- Today’s possibly more notable Fedspeak comes late on with Gov. Cook (voter) at 1930ET on global inflation and monetary policy (text + Q&A) when speaking in Australia. She said Jun 25 that the Fed is paying attention to the rising unemployment rate [before a further increase in June payrolls], talked on policy lags and also the better balance between jobs and inflation goals.

- Other Fedspeak is likely to be limited, with Goolsbee (’25 voter) and Gov. Bowman (voter) giving opening remarks at a Fed Listens event focused on childcare (just text).

US TSY FUTURES: OI Points To Mix Of Short Setting & Long Cover On Tuesday

Yesterday’s weakness in Tsy futures and preliminary OI data points to a mix of net short setting (TU & TY) and long cover (FV, UXY, US & WN), with the latter more dominant in net curve terms.

- We still believe that a ‘hawkish’ CPI surprise presents the greatest risk to prevailing market positioning, raising the bar for dovish market interpretation of tomorrow’s data.

| 09-Jul-24 | 08-Jul-24 | Daily OI Change | OI DV01 Equivalent Change ($) | |

| TU | 4,306,183 | 4,291,317 | +14,866 | +566,706 |

| FV | 6,354,401 | 6,367,065 | -12,664 | -535,102 |

| TY | 4,497,750 | 4,486,285 | +11,465 | +741,844 |

| UXY | 2,072,030 | 2,087,473 | -15,443 | -1,383,364 |

| US | 1,665,203 | 1,678,320 | -13,117 | -1,727,629 |

| WN | 1,661,107 | 1,663,107 | -2,000 | -404,531 |

| Total | -16,893 | -2,742,077 |

STIR: OI Points To Short Setting Bias In SOFR Futures Post-Powell

Yesterday’s downtick in SOFR futures and preliminary OI points to net short setting dominating in most contracts.

- Fed Chair Powell failed to provide a meaningfully dovish deviation vs. recent remarks, disappointing some who were looking for a bolder dovish tone in the wake of the recent run of soft labour market and economic activity data.

- Still, that data and the incremental shifts seen in Powell’s recent addresses leave the door open for a September rate cut.

- As a result, Fed fund futures discount 80% odds of a cut through the Sep FOMC and 50bp of easing through year end, essentially little changed vs. levels seen ahead of Powell’s address.

| 09-Jul-24 | 08-Jul-24 | Daily OI Change | Daily OI Change In Packs | ||

| SFRM4 | 1,200,970 | 1,194,405 | +6,565 | Whites | +28,971 |

| SFRU4 | 1,114,370 | 1,104,916 | +9,454 | Reds | +19,613 |

| SFRZ4 | 1,083,376 | 1,075,274 | +8,102 | Greens | +8,701 |

| SFRH5 | 831,036 | 826,186 | +4,850 | Blues | +14,012 |

| SFRM5 | 771,123 | 769,538 | +1,585 | ||

| SFRU5 | 679,874 | 669,001 | +10,873 | ||

| SFRZ5 | 843,565 | 833,263 | +10,302 | ||

| SFRH6 | 560,136 | 563,283 | -3,147 | ||

| SFRM6 | 484,881 | 487,645 | -2,764 | ||

| SFRU6 | 426,333 | 421,623 | +4,710 | ||

| SFRZ6 | 392,012 | 386,261 | +5,751 | ||

| SFRH7 | 251,175 | 250,171 | +1,004 | ||

| SFRM7 | 248,858 | 243,249 | +5,609 | ||

| SFRU7 | 188,906 | 186,169 | +2,737 | ||

| SFRZ7 | 181,453 | 177,025 | +4,428 | ||

| SFRH8 | 117,093 | 115,855 | +1,238 |

FX OPTIONS: Hedging Markets Still See Downside Risks for EUR/GBP

- EUR/GBP 3m vols capture not only possible policy moves at upcoming BoE and ECB meetings, but also the near-term risks present across both the French and UK parliaments. While vols have normalized considerably (back to ~4 points from mid-June's ~6 points) since Macron's snap election call, there remains a bias toward downside insurance via options, evident in both the popularity of EUR/GBP puts, and the 0.25ppts gap between 3m risk reversals and the rolling 12m average.

- Since July 4th, over €3 in puts have traded for every €2 in calls in the cross, driven by demand for put strikes layered between 0.82-0.83 and as low as 0.80 (at which over €850mln notional has traded). This has shifted the options-implied distribution for spot over the coming 3 months, which currently prices EUR/GBP below 0.83 with a 13.8% likelihood (vs. 9.3% pre-Macron election call). Should this trend be sustained, analyst consensus should come under further pressure from it's current 0.85 (vs. Forward 0.8483).

- The normalization of outright vol cheapens hedging for this outcome - a 3m 0.83 vanilla put costs ~28 EUR pips, cheapened to ~13 EUR pips when adding a 0.80 knock-out barrier.

- Positioning offers further clues - CFTC data shows the GBP net position as a % of open interest rose to a new 52w high just ahead of the UK election, aiding the recent rally, while some sell-side analysts bolstered their UK growth outlook following the vote.

UK FISCAL: When could the Budget be?

- We think that the most likely dates for a UK Budget are 30 October (or 6/13 November) with an outside chance that Reeves announces today a 18 September date.

- The biggest constraint to when a Budget can be held is the 10 weeks notice the OBR must be given to begin producing forecasts (the Office for Budget Responsibility (OBR) is the UK's official independent forecaster of public finances). Given that a Budget is normally held on a Wednesday, if notice was given to the OBR today that would mean a Budget date of 18 September (the day before the MPC announces its policy decision).

- However, from a political standpoint this would be seen as poor form. This would come in the middle of the party conference season (the Lib Dems conference is 14-17 September, Labour 22-25 September and Conservatives 29 September - 2 October). Moving these conferences around to accommodate a Budget would be a very unpopular political move.

- Furthermore, benefits and pensions are based on the September CPI figures - which are not due for release until 16 October. The Low Pay Commission also uses the September CPI figures as an input into its recommendations for the minimum / National Living Wage - and usually reports to the government within a few weeks of the September CPI release.

- Given that the Labour party wanted to provide as much certainty to businesses as possible and also stated that only one major fiscal event would be held annually, a comprehensive Budget - including plans for all of next year's allowances - would be unlikely before Wednesday 30 October (or possibly even 6/13 November).

- Note that holding a Budget later does not prohibit isolated announcements of spending plans - but after the market reaction to the Truss Budget, the new government will be wary of announcing new spending plans that appear unfunded.

- However, those dates would still be 16-18 weeks away from now so there is a possibility that the government does decide to interrupt the party conference season and hold its first Budget on 18 September in order to benefit from the honeymoon period of goodwill from the electorate.

- Reeves has stated that the date of the Budget will be confirmed before the summer recess (with reports that the current session of parliament will sit until 31 July).

BOE: Pill and Mann both due to speak today

- Huw Pill will speak at Asia house at 14:30BST today (text to be released at that time here with a Q&A to follow). Pill is generally seen as the most hawkish of the internal members - if he strikes a more dovish tone it would likely be interpreted as a dovish shift for all of the internal members and increase the probability of an August cut. In our view this is the most important UK event of the week.

- Mann will appear on a panel on business investment this afternoon at 16:30BST in Manchester. She has been one of the most hawkish MPC members for some time, but her stance seemed to have softened a little in recent speeches. The panel is not directly covered monetary policy, but she is normally forthright with her views when she is asked (even if it is slightly off topic) and it will be interesting to see whether she is still some way from considering voting for a cut.

- These appearances follow Haskel's speech on Monday (ahead of his last MPC meeting on 1 August before his non-renewable term ends). He remained on the hawkish side, saying that "I would rather hold rates until there is more certainty that underlying inflationary pressures have subsided sustainably." His comments did not move markets as even if there is a cut in August - he was not expected to vote for it. It was notable, however, that he said that the labour market revisions made earlier this year suggested the UK was "much more indicative of travelling down the steep portion of the pre-pandemic Beveridge curve" which "suggests inflation could be returned to target at a lower interest rate" and that this was one of the "motivations" to change to voting on hold at the March meeting.

- At the time of writing markets price around a 60% probability of a 25bp cut at the August MPC meeting with a cumulative 48bp priced by year-end (and four 25bp cuts fully priced by the August 2025 meeting). If Pill's comments are explicitly one directional today we expect the probability of an August cut could fall to as low as 30%, or up to around 75-80%. However, despite downplaying the importance of individual data points in the June MPC statement / Minutes, next week's CPI / labour market data remain very important.

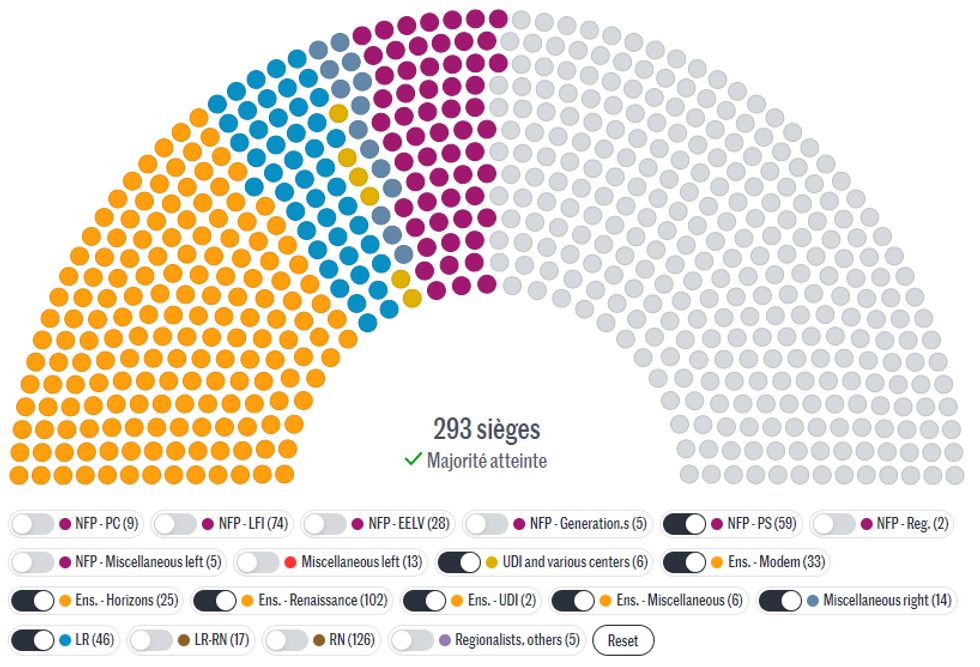

FRANCE: Macron Ministers Calls For Ensemble-LR Alliance To Outflank NFP

Minister of the Interior Gérald Darmanin and Minister for Gender Equality Aurore Bergé hailing from the centrist Renaissance party have this morning both called for the centrist Ensemble alliance supportive of President Emmanuel Macron and PM Gabriel Attal, to form an alliance with the conservative Les Republicains (LR) party (Darmanin and Bergé are both former LR members). According to figures from Le Monde, this grouping would command 214 seats in National Assembly, short of a majority but comfortably the largest alliance. This would put it in a stronger position to argue that PM Emmanuel Macron should appoint one of its figures to the position of prime minister.

- There are a number of potential obstacles to this plan. The French political tradition is not one accustomed coalition building, making any formal alliance between Ensemble and LR difficult.

- According to Le Monde, LR's price for joining with Ensemble could be steep: the office of the PM. It is unclear whether Ensemble would be willing to countenance this option, or if it would be worth paying the price in order to sit as the largest grouping.

- One of the only ways to reach a majority would be to bring in miscellaneous groups and the centre-left Socialist Party (PS). The PS sits in the leftist New Popular Front (NFP), currently the largest bloc in the Assembly. It splitting from the alliance would require significant concessions, which in turn could see the LR turn away from the coalition.

- Political paralysis is likely in the weeks and months ahead given the fairly even split between Ensemble, NFP and the right-wing nationalist National Rally (RN).

Chart 1. National Assembly with Hypothetical Majority Gov't

Source: Le Monde

Source: Le Monde

FOREX: AUD/NZD Lurches to Multi-Year High on Dovish RBNZ

- The single currency trades firmly, outstripping most others in G10 on the back of further horse-trading in France, as Macron's Ensemble look to secure the highest offices in parliament by making a potential cross-aisle deal with the right-of-centre Les Republicains in order to freeze Marine Le Pen's RN out of power.

- Resultantly, EUR/JPY has traded a new high in European trade, touching 174.89 and extending the recent bull run. The cross (much like other JPY crosses) remains technically overbought, but subdued vols continue to favour carry trade dynamics, working against the JPY.

- Lastly, NZD is weaker, falling against all others in G10 space after the dovish turn from the RBNZ. While the bank kept rates unchanged, they moderated their language on future policy considerably, suggesting that rates could be eased as inflation slows. AUD/NZD traded a new YTD high at 1.1103 - and holds the bulk of those gains into the NY crossover.

- The data schedule remains light Wednesday, with just wholesale trade sales and inventories data on the docket. This should, again, keep focus on the central bank speaker slate - BoE's Pill is set to speak, an MPC member that's seen potentially swinging a decision around an August rate cut at the BoE.

FX OPTIONS: Expiries for Jul10 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0600(E1.3bln), $1.0650(E1.6bln), $1.0760-80(E3.0bln), $1.0795-00(E705mln), $1.0875-80(E1.1bln), $1.0895-05(E1.3bln)

- USD/JPY: Y159.50($1.6bln), Y160.00($2.1bln), Y161.00-20($1.8bln), Y161.50($1.1bln)

- AUD/USD: $0.6770(A$1.0bln), $0.6810(A$716mln)

- USD/CNY: Cny7.2500($661mln), Cny7.3000($1.1bln)

EQUITIES: Bull Cycle in Eurostoxx 50 Futures Intact Despite This Week's Pullback

- A bull cycle in Eurostoxx 50 futures is intact, despite yesterday’s move down. Attention is on resistance at 5039.84, 61.8% of the May 16 - Jun 14 sell-off. It was pierced last Friday, a clear break of this level would be a positive development and suggest scope for an extension of the bull cycle that started Jun 14. This would open 5082.32, the 76.4% retracement. A stronger reversal would instead expose 4846.00, the Apr 19 low and a key support.

- The trend condition in S&P E-Minis is bullish and this week’s extension reinforces this set-up. The contract is trading at its latest highs. Fresh cycle highs confirm a resumption of the uptrend and maintain the bullish sequence of higher highs and higher lows. MA studies are in a clear bull-mode set-up too and this continues to highlight positive market sentiment. Sights are on 5668.00, a Fibonacci projection. Support is at 5536.81, the 20-day EMA.

WTI Futures Extend Pullback From Last Week's High

- WTI futures are trading lower today as the contract extends the pullback from last week’s high. The move down is likely a correction. Recent gains reinforced bullish conditions, signalling scope for a continuation higher near-term. Moving average studies are in a bull-mode set-up too, highlighting a rising trend. Sights are on $85.27, the Apr 12 high and a bull trigger. Initial firm support to watch is $79.70, the 50-day EMA.

- Recent gains in Gold resulted in a print above resistance at $2387.8, the Jun 7 high. This undermines a recent bearish theme and a clear break would be viewed as a bullish development and open the key resistance at $2450.1, the May 20 high. Initial support to watch lies at the 50-day EMA, at 2327.8. A clear break of this average would instead confirm a resumption of the reversal from May 20 and expose $2277.4, May 3 low.

| Date | GMT/Local | Impact | Country | Event |

| 10/07/2024 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 10/07/2024 | - | *** | Money Supply | |

| 10/07/2024 | - | *** | New Loans | |

| 10/07/2024 | - | *** | Social Financing | |

| 10/07/2024 | 1330/1430 | BoE Pill At Asia House | ||

| 10/07/2024 | 1400/1000 | ** | Wholesale Trade | |

| 10/07/2024 | 1400/1000 | Fed Chair Jerome Powell | ||

| 10/07/2024 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 10/07/2024 | 1530/1630 | BOE's Mann Panellist on UK Business investment | ||

| 10/07/2024 | 1700/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 10/07/2024 | 1830/1430 | Chicago Fed's Austan Goolsbee | ||

| 10/07/2024 | 2330/1930 | Fed Governor Lisa Cook | ||

| 11/07/2024 | 2350/0850 | * | Machinery orders | |

| 11/07/2024 | 0600/0700 | ** | UK Monthly GDP | |

| 11/07/2024 | 0600/0700 | ** | Trade Balance | |

| 11/07/2024 | 0600/0700 | ** | Index of Services | |

| 11/07/2024 | 0600/0700 | *** | Index of Production | |

| 11/07/2024 | 0600/0700 | ** | Output in the Construction Industry | |

| 11/07/2024 | 0600/0800 | *** | HICP (f) | |

| 11/07/2024 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 11/07/2024 | 1230/0830 | *** | Jobless Claims | |

| 11/07/2024 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 11/07/2024 | 1230/0830 | *** | CPI | |

| 11/07/2024 | 1430/1030 | ** | Natural Gas Stocks | |

| 11/07/2024 | 1515/1115 | Atlanta Fed's Raphael Bostic | ||

| 11/07/2024 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 11/07/2024 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 11/07/2024 | 1700/1300 | St. Louis Fed's Alberto Musalem | ||

| 11/07/2024 | 1700/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 11/07/2024 | 1800/1400 | ** | Treasury Budget | |

| 12/07/2024 | 0430/1330 | ** | Industrial Production | |

| 12/07/2024 | 0600/0800 | *** | Inflation Report | |

| 12/07/2024 | 0645/0845 | *** | HICP (f) | |

| 12/07/2024 | 0700/0900 | *** | HICP (f) | |

| 12/07/2024 | - | *** | Trade | |

| 12/07/2024 | 1230/0830 | *** | PPI | |

| 12/07/2024 | 1230/0830 | * | Building Permits | |

| 12/07/2024 | 1300/0900 | * | CREA Existing Home Sales | |

| 12/07/2024 | 1400/1000 | ** | U. Mich. Survey of Consumers | |

| 12/07/2024 | 1600/1200 | *** | USDA Crop Estimates - WASDE | |

| 12/07/2024 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |