Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

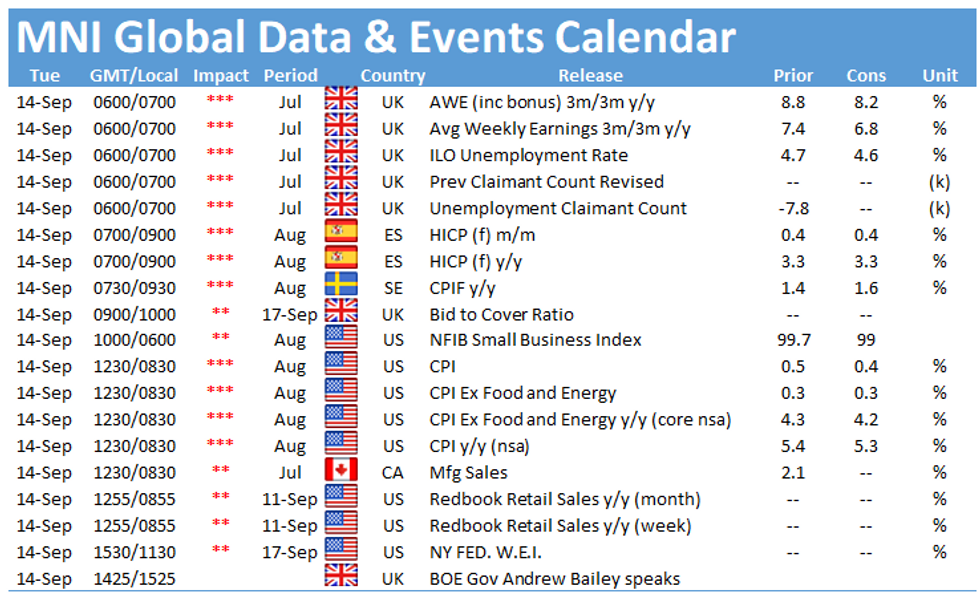

UK employment data will dominate the early part of Tuesday's session, but the U.S. inflation report will undoubtedly be the highlight of the day.

UK May-July Earnings To Decelerate Modestly From Record High (0700BST)

UK earnings growth decelerated slightly in the three months to July, but likely remained at highly-elevated levels, while employment continued to improve over the period. Total earnings rose by an annual rate of 8.2% between May and July, according to City analysts, a rate previously regarded as astronomical, but below the record-high 8.8% pace hit in the second quarter.

Earnings were elevated by a 41.1% surge in bonuses in the latest three months, a combination of incentives and benchmark effects that could be repeated between May and July. Regular earnings are likely to decelerate to 6.8% from 7.4% in the second quarter. Meanwhile, anecdotal reports of a tight jobs market are likely to be reflected in a fall in the jobless rate to 4.6%, say forecasters, from 4.7% in the second quarter. However, analysts will be eyeing the inactivity rate, which has recovered only slowly, to 21.1% in the three months to July from 20.2% in the three months to February of 2020.

Vacancies will also be in focus after rising by 290,000 in the three months to July over the February-to-April period, taking the number of advertised jobs to 953,000, above pre-pandemic levels. Vacancies rise by 50,000 between June and July to a record-high 1.034 million.

U.S. CPI likely slowed in August (1330BST)

CPI growth slowed marginally in August, with Bloomberg predicting a monthly gain of 0.4% following a 0.5% increase in July. From a year earlier, CPI is expected to be up 5.3% compared to 5.4% in July. August's increase is likely to be driven by rising gasoline and food prices, and analysts say previous wage increases and supply bottlenecks could have also translated through consumer prices.

Excluding food and energy prices, CPI should increase 0.3% m/m, according to Bloomberg, and 4.2% y/y.

Among policymakers due to speak Thursday is Bank of England governor Andrew Bailey.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.