Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

MNI (London)

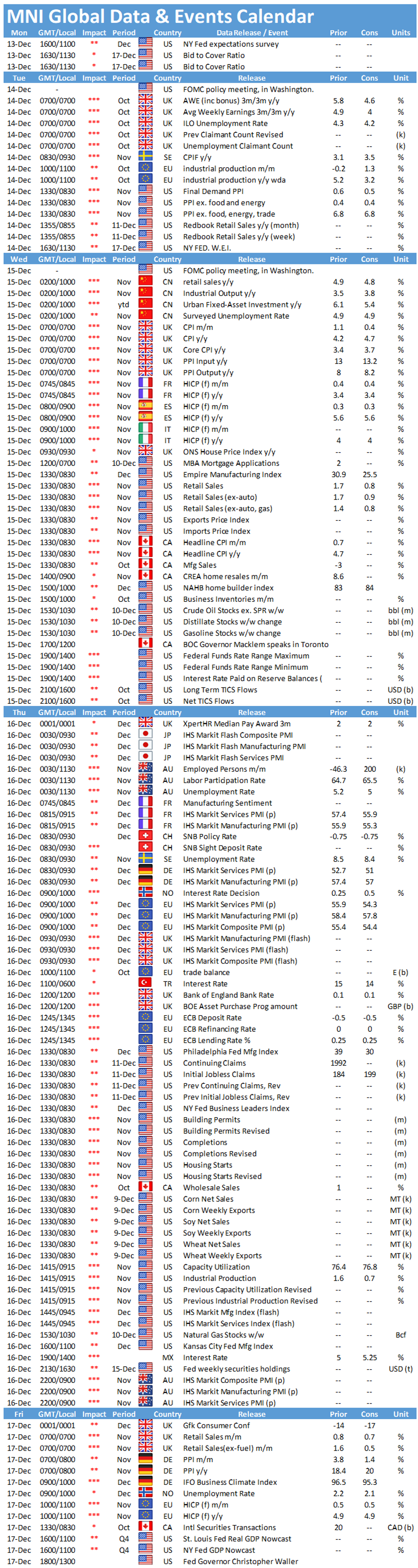

The coming week sees policy decisions from many of the world's leading central banks, with the Fed, ECB and BOE to the fore.

UK PPI and CPI (Wednesday)

- Markets will be watching Wednesday’s PPI and CPI data, although it is unlikely to convince the BoE to hike before the February MPC meeting.

- Analysts forecast annual headline inflation to hit 4.8% for November, but with more downside risks. This is up from 4.2% in October, reflecting both high energy prices from the October 1st increase in the Ofgem energy price cap. Monthly CPI is expected to come in at 0.4% in November, down from 1.1% in October.

- Annual producer prices for inputs and outputs are forecasted to bump up .2 percentage points to 13.2% and 8.2% respectively. On the flipside, monthly producer prices are both projected to fall by over half a percentage point to 0.6% for inputs and 0.5% for outputs, down from 1.6% and 1.1% respectively. Oil and petroleum are the key forces driving prices up, notably input PPI which is more volatile.

Fed to quicken taper (Wednesday)

- The tight labour market and high inflation expectations represent a green light for the Fed to accelerate tapering faster to finish in March, with markets pricing a hike shortly after.

- Friday's data saw November's annual headline inflation hit a 39-year high of 6.8%.

- Powell hinted at this a couple weeks ago stating, “it is…appropriate in my view to consider wrapping up the taper of our asset purchases, which we actually announced at the November meeting, perhaps a few months sooner”.

- However, this comment was made before the first Omicron variant case was found in the US, which is likely to provide considerable downside growth risks for the upcoming Winter months.

- Former Fed economists and policymakers told MNI that the Fed’s dot plot looks likely to include two hikes in 2022, with some even seeing three if inflationary pressures persist.

ECB decision time as PEPP in final furlong (Thursday)

- Thursday will likely to see the ECB continue with the planned PEPP until March 2022, whilst exploring options to allow more flexibility with the programme, for example to smooth into April with more flexible increased APP purchasing.

- In line with the ECB’s medium-term inflation outlook, a rate hike in 2022 is all but out of the picture. November’s eurozone headline inflation record of 4.9% y/y coupled with price surges from struggling supply chains put further dovish policy under pressure.

BoE to hold off on hiking (again) (Thursday)

- The BoE looks set to again postpone their rate hike, maintaining the level 0.1%.

- In November it seemed almost certain that a 15bp December hike would follow, especially following October CPI hitting a 10-year high of 4.2% y/y and the labour market looking tight.

- Doubts were casted though following Friday's disappointing GDP data, which saw the UK economy practically stall in October at a monthly growth rate of just 0.1%.

- As for all central bank policy decisions this week, the recently emerged Omicron variant appears to be commanding more cautionary dovish behaviour, with markets pricing a hike to be postponed to February 2022.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok