Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

MNI (London)

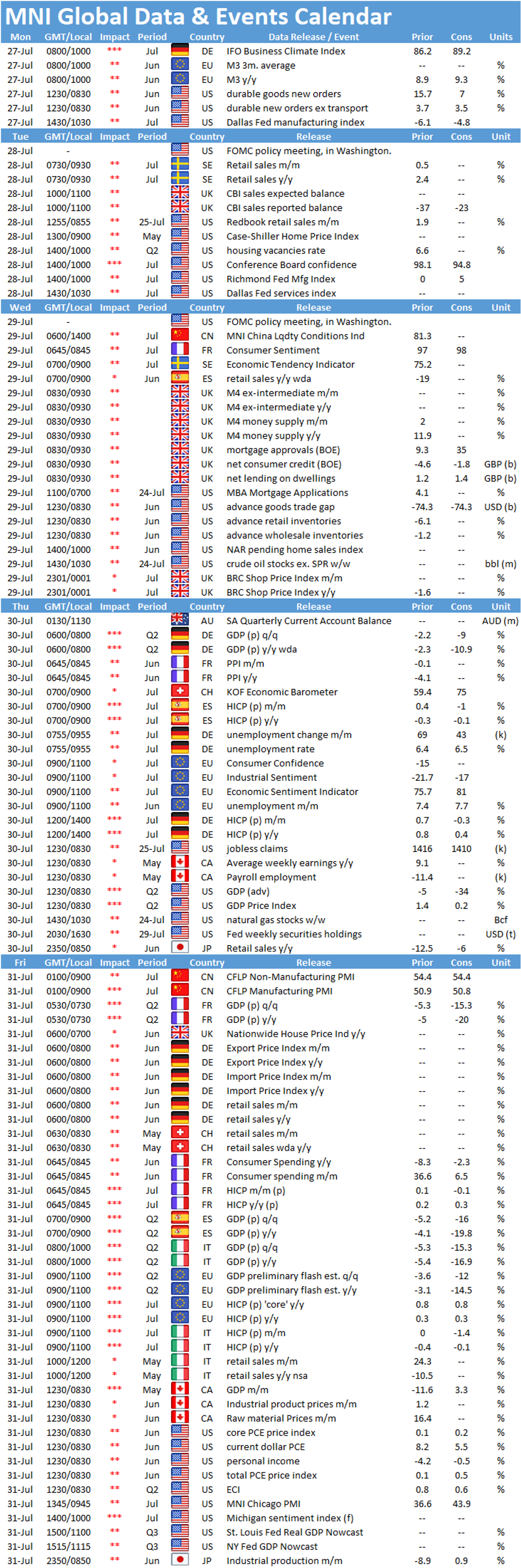

Key Things to Watch For:

- Wednesday, July 29 – FOMC Policy Decision

- No major policy announcements are expected at the July FOMC meeting as the committee gathers for another working session to finalize its policy framework review and lay groundwork for outcome-based forward guidance.

- The Fed is likely to switch to targeting average inflation in September, in a much-anticipated move, but former policymakers told MNI it will opt not to reveal how long it would allow prices to increase at faster than its 2% target to maximize flexibility.

- As the economic outlook darkens and caseloads climb, former top officials also said the Fed's plan to set conditions on its forward guidance may be pushed back to later in the year.

- No major policy announcements are expected at the July FOMC meeting as the committee gathers for another working session to finalize its policy framework review and lay groundwork for outcome-based forward guidance.

- Thursday, July 30 – U.S. Q2 GDP (Advance Estimate)

- Thursday's advance estimate of U.S. Q2 GDP will unearth the depth of the Covid-19 recession, with markets expecting a record-shattering 34% annualized drop after a 5% decline in Q1 that was the largest fall since 2008.

- Consumption fell sharply in the second quarter as businesses nationwide remained closed and state-mandated lockdowns persisted, restricting travel in some cases into mid-June.

- Momentum from state reopenings beginning in April wasn't nearly strong enough to bring about a rebound in activity in Q2, and consumer sentiment stumbled in June as surging new Covid-19 cases resurfaced concerns about leaving the home.

- Thursday's advance estimate of U.S. Q2 GDP will unearth the depth of the Covid-19 recession, with markets expecting a record-shattering 34% annualized drop after a 5% decline in Q1 that was the largest fall since 2008.

- Friday, July 31 – Eurozone Q2 GDP (Advance Estimate)

- Friday sees the publication of the eurozone Q2 advance flash GDP report, giving the first official reading on just how deep the contraction was in the first three months of the pandemic fall out.

- Expectations are for a q/q decline of 11.5%, with Q2 GDP seen down 14% year-on-year (Q1 -3.6% q/q and 3.1% y/y), perhaps slightly better than some of the worst-case scenario's envisaged back in April.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok