Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

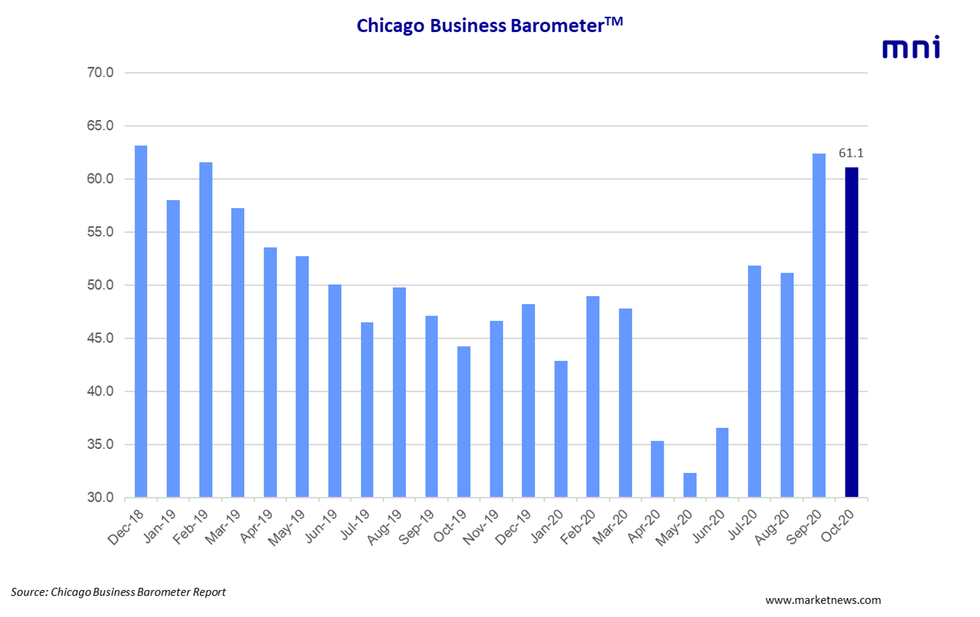

The Chicago Business Barometer edged lower in October, but still outpaced beating market expectations looking for a steeper decline.

The headline index eased to 61.1 in October after September's sharp increase. However, it still marks the fourth consecutive reading above the 50-mark after sitting below it for a whole year.

Among the five main indicators, New Orders was the only category to show a monthly uptick, while Production recorded the largest decline.

Demand picked up modestly in October with New Orders rising 0.2* points to 65.0, its highest level since November 2018. Production saw the largest fall, down 5.9* points to 62.1. Anecdotal evidence provided mixed signals, with some firms noting a drop in demand, while others saw a stable level of orders and production or a gradual improvement in business activity.

Order Backlogs eased 2.4 points to a two-month low of 50.5. The index remains in expansion territory for the second month in a row. Meanwhile, Inventories cooled marginally to 47.7 in October, static from 47.8 recorded in September

Employment is the only major category to record a sub-50 reading. It backtracked to 43.2 in October with firms noting staff reductions as a result of the pandemic.

Supplier Deliveries eased to 65.3 in October with firms emphasising the impact of the current crisis. Prices at the factory gate were stable in October, dipping 0.1 points to 64.6 with firms reporting higher prices for wood, steel and chemicals.

This month's special question asked: "Are you planning to make working remotely a permanent option for your employees after the pandemic?". A majority 45.8% were unsure, 35.6% were not planning to make it a permanent option, while 18.6% supported it. The second question asked: "Have you re-evaluated your supply chains, attempting to take China out of the equation?". The majority 47.4% had not re-evaluated their supply chains, while one third of respondents had adjusted their supply chains.

This month's survey ran from October 1 to 19.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.