Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

MNI U.S. Weekly Macro Wrap

MNI U.S. Weekly Macro Wrap

Executive Summary

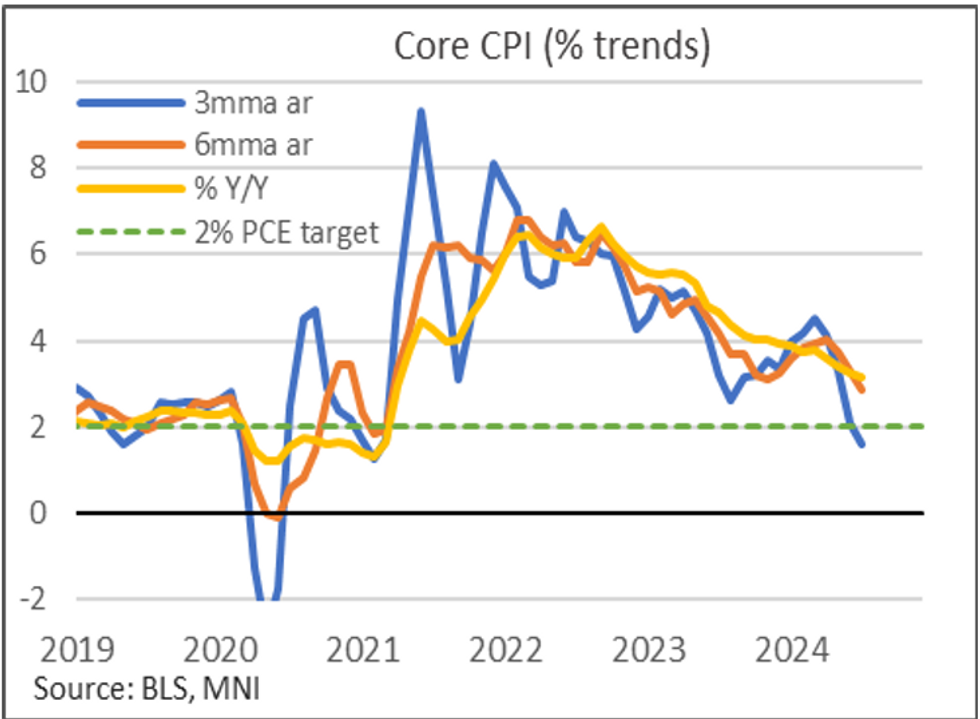

- PPI inflation unusually landed before CPI, surprising lower in July with trade services in particular extremely weak but only after spiking in June.

- Core CPI inflation was then marginally softer than expected in July at 0.165% M/M but the details were arguably stronger, primarily from an acceleration in heavily-weighted rental components.

- The CPI report broadly supported the disinflationary trend that’s been seen in recent months and helps warrant rate cuts ahead, but we didn’t see anything in it that justified a 50bp cut at the September FOMC.

- The rest of the week saw stronger than expected prints for the two other most notable releases – retail sales and jobless claims – although other areas saw misses for both industrial production and housing starts/building permits.

- The latter have seen Q3 GDP tracking estimates lowered by 1pp to 2.0% annualized although as we noted in the MNI Inflation Insight we only need to see releases not show signs of anything “breaking” to see a further fading of 50bp cut expectations.

- That’s what’s happened this week, with September cut expectations trimmed to 33bp vs 40bp at the start of the week. However, whilst the cumulative 95bp of cuts for the three meetings left this year has also been reduced from over 100bps, it still implies sizeable odds of a 50bp cut at one of those meetings.

- Next week sees the FOMC minutes and Powell’s appearance at the Jackson Hole Symposium, but the ultimate test for September rate cut expectations will likely be the August payrolls report on Sep 6.

PLEASE FIND THE FULL REPORT HERE:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok