Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

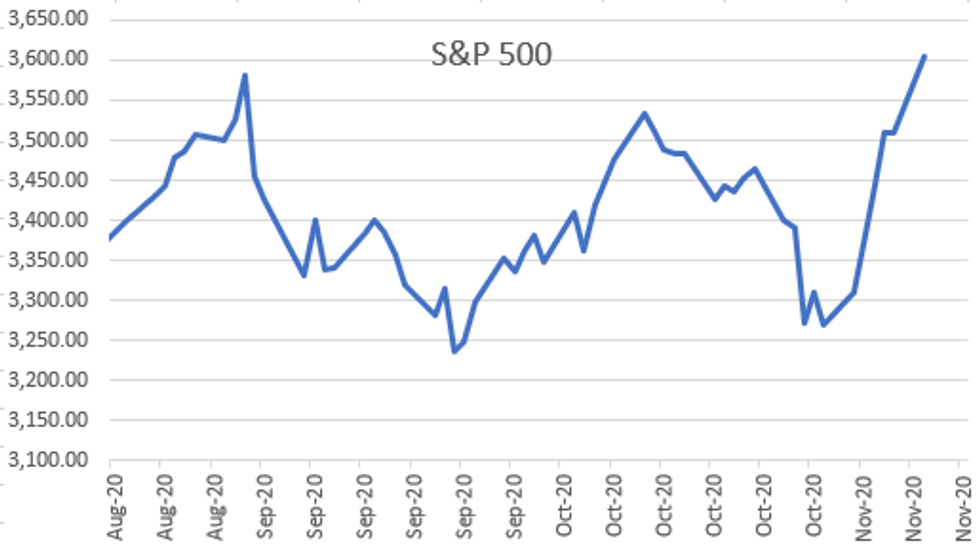

US TSY SUMMARY: Risk On Surge, Scaling Back Late

Already trading with a risk-on tone following weekend news former VP Biden now President Elect, rates gapped lower/equities surged to new all-time highs before the NY open after Pfizer announced vaccine is 90% effective in combatting Covid-19.

- Heavy Tsy volumes (TYZ 175% 20D avg, FVZ 184% 20D avg). Obviously better selling included huge Blocks (-23,500 TYZ 137-19 for example) helped push 10YY to eight month high of 0.9730% midmorning. Curve steepeners back on (+10,865 TYZ vs. -4,553 USZ)

- S&P futures extended rally to new high of 3668.0 (appr +155.0) after the open but scaled back to +85.0 after the close.

- After holding to sidelines do to election uncertainty, corporate issuance returned with a bang w/ $18.5B, lion's share tied to $7B Bristol-Myers Squibb 6pt. US Tsy $54B 3Y Note auction (91282CAW1) stopped through: awarded 0.250% (0.193% last month) vs. 0.252% WI, on a bid/cover 2.40 vs. 2.44 previous.

- The 2-Yr yield is up 2.8bps at 0.1806%, 5-Yr is up 8.3bps at 0.444%, 10-Yr is up 13.6bps at 0.9542%, and 30-Yr is up 14.6bps at 1.7464%.

TECHNICALS

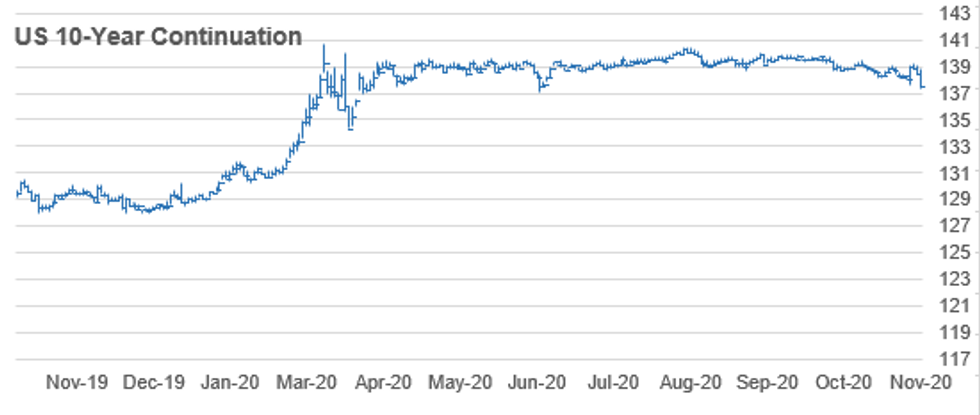

US 10YR FUTURE TECHS: (Z0) Hit Hard on Vaccine Headlines

- RES 4: 139-30 1.?0% 10-dma envelope

- RES 3: 139-26 High Sep 29 and a key resistance

- RES 2: 139-13+ Bear channel top drawn off the Aug 4 high

- RES 1: 139-08+ High Nov 5

- PRICE: 138-20+ @16:07 GMT Nov 9

- SUP 1: 138-12+ Low Nov 6

- SUP 2: 137-20+ Low Nov 4 and key support

- SUP 3: 137-15 1.382 proj of Aug 4 - 28 decline from Sep 3 high

- SUP 4: 137-08 1.500 proj of Aug 4 - 28 decline from Sep 3 high

After establishing a bullish tone following the rally Nov 4th, markets reversed sharply Monday as vaccine headlines boosted risk. Late last week, price cleared trendline resistance, drawn off the Oct 2 high. The break was confirmed by a breach of resistance at 139-03, Oct 28 high and a recent bull trigger. This highlights a likely significant reversal of the entire decline since early August and opens 139-13+, a bear channel top drawn off the Aug 4 high. Pullbacks, for now, are considered corrective, 138-12+ is initial support.

AUSSIE 3Y

AUSSIE 3-YR TECHS: (Z0) Strong on RBA Support

- RES 3: 100.00 - Psychological round number

- RES 2: 99.886 - 3.0% Upper Bollinger Band

- RES 1: 99.860 - All time High Nov 3 and the bull trigger

- PRICE: 99.835 @ 16:15 BST Nov 9

- SUP 1: 99.760 - Low Oct 1 and 2

- SUP 2: 99.705 - Low Sep 18, 21 and 22

- SUP 3: 99.675 - Low Sep 7 and key support

Aussie 3yr futures got further support last week as the RBA cut their 3-yr yield target, boosting prices to new alltime highs up at 99.860. This further confirms bullish trend conditions, leaving the downside argument particularly fractious. A break of 99.860, the Nov 3 high opens 99.889. Support is at 99.760.

Aussie 10Y

AUSSIE 10-YR TECHS: (Z0) Steps Lower on Vaccine News

- RES 3: 99.480 - High Mar 10 and the all-time high

- RES 2: 99.360 - High Apr 2 (cont)

- RES 1: 99.290 - High Oct 16

- PRICE: 99.090 @ 16:17 BST Nov 9

- SUP 1: 99.075 - Low Nov 9

- SUP 2: 99.055 - Low Sep 18 and 21

- SUP 3: 98.970 - Low Sep 8

Aussie 10y futures fell sharply Monday alongside the global bond market, slipping to 99.075 before stabilising. Overall, markets remain bullish despite Monday's pullback. The break above 99.180, an area of congestion reflecting highs in Sep and early October confirmed a resumption of the uptrend that started on Aug 28. Attention turns to 99.300 and 99.360. The latter is the Apr 2 high (cont). The near-term bull trigger is 99.290, Oct 16 high. On the downside, firm trend support remains at 99.075, Oct 5 low.

Yen 10Y

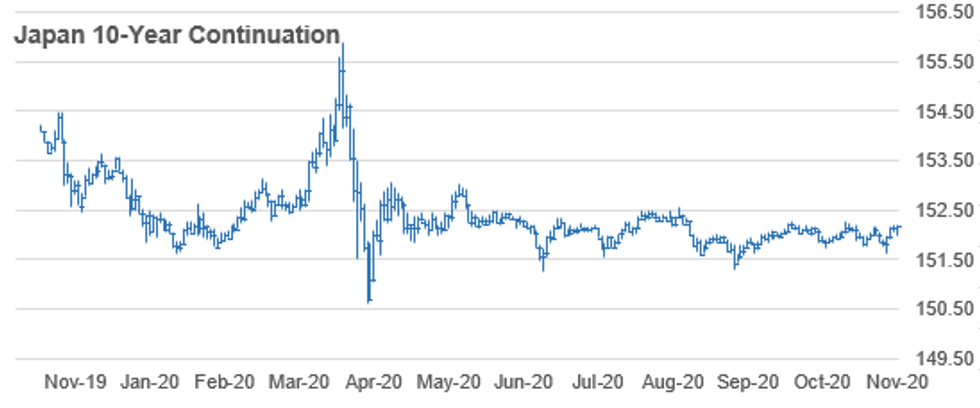

JGB TECHS: (Z0) Drops with Global Bonds

- RES 3: 152.55 - High Aug 5 (cont)

- RES 2: 152.36- 3.0% Upper Bollinger Band

- RES 1: 152.29 - High Sep 24 and the bull trigger

- PRICE: 151.79 @ 16:45 BST Nov 9

- SUP 1: 151.75 - Low Oct 08 and trend support

- SUP 2: 151.54 - Low Sep 7

- SUP 3: 151.43 - Low Sep 1

Following the Pfizer vaccine headlines, global bonds slumped and JGBs were no exception. Prices slipped to hit support at the 151.75 trend support before stabilising. A break below here is needed to reverse the currency positive outlook. Attention remains on 152.29, Sep 4 high, a key resistance and the bull trigger. A break of this level would confirm a resumption of the uptrend and open 152.36, a Bollinger band objective and 152.55, Aug 5 high (cont).

TSY FUTURES CLOSE: Risk Appetite Surge After Positive Pfizer Annc

Rates gapped lower ahead the NY open on the back of Pfizer vaccine headlines annc 90% success rate in combatting Covid-19. Equities surged to new all-time highs (S&P eminis paring late, Dec futures +90.0 late vs. +155.0 on the open). Sharp bear steepen in yield curves. Update:

- 3M10Y +13.323, 86.043 (L: 70.283 / H: 87.67)

- 2Y10Y +10.793, 77.167 (L: 64.585 / H: 78.452)

- 2Y30Y +11.857, 156.317 (L: 141.794 / H: 157.636)

- 5Y30Y +6.34, 130.012 (L: 122.198 / H: 132.657)

- Current futures levels:

- Dec 2Y -1.75/32 at 110-11.25 (L: 110-10.75 / H: 110-13.37)

- Dec 5Y -11.75/32 at 125-9.25 (L: 125-06 / H: 125-24)

- Dec 10Y down 30/32 at 137-19.5 (L: 137-13 / H: 138-24.5)

- Dec 30Y down 2-30/32 at 170-12 (L: 169-29 / H: 173-24)

- Dec Ultra 30Y down 5-30/32 at 211-02 (L: 210-07 / H: 218-06)

US EURODLR FUTURES CLOSE: Sharply Lower, Long End Leads On Heavy Volumes

Mirroring Tsy futures, Eurodollar futures sharply lower across the strip, short end outperforming. Lead quarterly held steady much of day since 3M LIBOR set -0.00088 to new all-time low of 0.20500% (-0.00275 net last wk).

- Dec 20 -0.005 at 99.765

- Mar 21 -0.010 at 99.790

- Jun 21 -0.015 at 99.785

- Sep 21 -0.020 at 99.780

- Red Pack (Dec 21-Sep 22) -0.045 to -0.02

- Green Pack (Dec 22-Sep 23) -0.085 to -0.05

- Blue Pack (Dec 23-Sep 24) -0.145 to -0.095

- Gold Pack (Dec 24-Sep 25) -0.18 to -0.15

US DOLLAR LIBOR: New All-Time Low 3M Rate

Latest settles:

- O/N -0.00150 at 0.08113% (+0.00125 net last wk)

- 1 Month +0.00213 to 0.12988% (-0.01250 net last wk)

- 3 Month -0.00088** to 0.20500% (-0.00275 net last wk)

- 6 Month -0.00163 to 0.24175% (+0.00125 net last wk)

- 1 Year -0.00088 to 0.33250% (+0.00325 net last wk)

- ** 3M New record Low 0.20500% on 11/9/20 ** (prior 0.20588% on 11/6/20)

US TSY: Short End Rates

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 0.09% volume: $64B

- Daily Overnight Bank Funding Rate: 0.08%, volume: $165B

- Secured Overnight Financing Rate (SOFR): 0.10%, $888B

- Broad General Collateral Rate (BGCR): 0.08%, $343B

- Tri-Party General Collateral Rate (TGCR): 0.08%, $315B

- (rate, volume levels reflect prior session)

- Tsy 20Y-30Y, $1.733B accepted vs. $4.067B submission

- Next scheduled purchases:

- Tue 11/10 1010-1030ET: TIPS 1Y-7.5Y, appr $2.425B

- Thu 11/12 1010-1030ET: Tsys 7Y-20Y, appr $3.625B

- Fri 11/13 1010-1030ET: Tsy 2.25Y-4.5Y, appr $8.825B

- Fri 11/13 Next forward schedule release at 1500ET

OUTLOOK: Look Ahead To Tuesday

- US Data/Speaker Calendar (prior, estimate)

- 10-Nov 0600 Oct NFIB Small Business Index (104.0, 104.2)

- 10-Nov 0730 Dallas Fed Kaplan, Bbg event

- 10-Nov 0855 7-Nov Redbook retail sales m/m

- 10-Nov 1000 Sep JOLTS quits rate (2.0%, --)

- 10-Nov 1000 Sep JOLTS job openings level (6.493M, 6.500M)

- 10-Nov 1000 Boston Fed Rosengren, financial stability conf

- 10-Nov 1200 Dallas Fed Kaplan, foreign relations council

- 10-Nov 1200 15/16 commodity crop stocks data

- 10-Nov 1230 Atl Fed Bostic, recorded opening remarks

- 10-Nov 1300 US Tsy $41B 10Y Note auction (91282CAV3)

- 10-Nov 1000 Fed VC Quarles, Senate Banking panel testimony

- 10-Nov 1600 Boston Fed Rosengren, expected repeat of 1000ET

- 10-Nov 1700 Fed Gov Brainard, comm reinvestment act

PIPELINE: Bristol-Myers Squibb 6pt Launched; $18.5B Total/

$18.5B Total debt to price Monday

- Date $MM Issuer (Priced *, Launch #

- 11/09 $7B #Bristol-Myers Squibb 6pt: $1.5B 3NC1 +30, $1B 5Y +35, $1B 7Y +45, $1.25B 10Y +55, $750M 20Y +65, $1.5B 30Y +85. Last multi-tranche jumbo issue from Bristol-Myers: total $19B in 9-parts on May 7, 2019: $750M 1.5Y +20, $1B 2Y +35, $1.5B 3Y fix +45, $500M 3Y FRN L+38, $3.25B 5Y +73, $2.25B 7Y +90, $4B 10Y +105, $2B 20Y +30, $3.75B 30Y +145.

- 11/09 $4.5B #Morgan Stanley $1.75B 3NC2 +37.5, $2.75B 11.25NC10.25 +85

- 11/09 $2.5B #Westpac 15NC10 +175, 20Y +125

- 11/09 $1.2B #Vereit $500M +7Y +165, $700M 12Y +200

- 11/09 $1.1B #Republic Srvcs $350M 5Y +45, $750M 11Y +80

- 11/09 $1B #Caterpillar 5Y +38, (adds to $2B issued on May 12 and Jan 9)

- 11/09 $600M #Entergy LA $300M 10Y +70, $300M Tap 2.9% +95

- 11/09 $600M #Consolidated Edison 40Y +128

- 11/09 $4B *Fannie Mae 5Y +13.5

EURODOLLAR/TREASURY OPTIONS

Eurodollar Options:

- +10,000 Jun 100 calls, 1.0

- -30,000 Sep 97 puts, 2.5

- 17,500 Blue Mar 90 puts, 2.0

- 5,600 Blue Mar 96 calls

- +3,000 Blue Mar 97/98 call spds, 0.5

- -3,000 Blue Dec 90/92 put spds, 1.0

- +3,000 Blue Jun 91 puts, 8.5

- -5,000 Green Dec 95/96/97 put flys, 6.5

- +5,000 Blue Feb 93/95/96 put flys, 3.0

- Overnight trade, Surge In Put Trades

- * +24,500 Green Mar 95/96/97 2x3x1 put flys, 1.0

- * +10,000 Blue Dec 90/92 put spds, 1.0

- * Recent call trade

- * +10,500 Blue Feb 93/95/96 call flys, 3.0

Tsy Options:

- +5,000 TYF 139 calls, 5/64

- 3,000 TYF 136/137/137.5/138 put condors, 45/64

- -5,000 TYF 136/137 put spds, 17/64

- +5,000 TYF 138 calls, 20/64 last

- 4,100 TYG 137.5 straddles, 146-144

- -3,000 TYZ 139 puts 1-11, 137-26.5 ref

- 8,300 USZ 178 calls, 2/64

- 4,500 TYZ 138 calls, 17/64

- over 23,000 TYZ 137.5 puts, 10-16 adds to 50k Block

- Overnight trade

- BLOCK, -50,000 TYZ 137.5 puts, 10 vs. 137-30/0.33%

- 22,400 TYZ 138 puts, 25/64

- +8,000 FVZ 124/125.5 put spds, 12/64

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.