Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

MNI US MARKETS ANALYSIS - Mixed Trading

HIGHLIGHTS

- Govies traded weaker early in the session, with EGBs managing to recover losses.

- European equities have been mixed following broad gains in Asian markets

- Global political risk themes simmer in the background

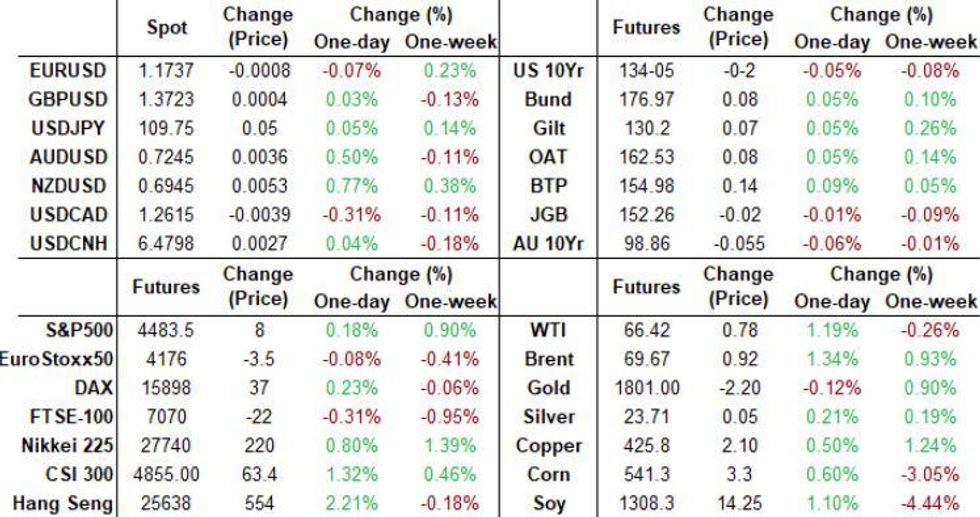

US TSYS SUMMARY: Weaker But Off Intraday Lows

Treasuries are a little weaker Tuesday, though off intraday lows.

- Modest steepening in the cash curve: 2-Yr yield is up 0.6bps at 0.2304%, 5-Yr is up 0.7bps at 0.7754%, 10-Yr is up 1bps at 1.2617%, and 30-Yr is up 1.2bps at 1.8823%.

- Sep 10-Yr futures (TY) trading well within the ranges of the past few sessions, last down 1.5/32 at 134-05.5 (L: 134-01 / H: 134-07.5).

- Short-end supply highlights Tuesday's calendar: $60B 2Y Note auction at 1300ET (we also get $40B of 67-day bills at 1130ET). NY Fed buys ~$2.025B of 1-7.5Y TIPS.

- A limited data slate today, with Richmond Fed Manufacturing at 1000ET (the latest in what has so far been a series of disappointing August surveys), with Jul new home sales at 1000ET.

- Some attention on Afghanistan: G7 holds a videoconference at 0930ET, with Pres Biden delivering remarks at 1200ET.

- On Capitol Hill, the Democratic Caucus meets at 0900ET to further debate next steps on fiscal legislation (after the House adjourned after midnight last night without a deal).

EGB/GILT SUMMARY - Recovering Early Losses

EGBs have pared some of the early selling, coming under pressure as risk extended higher, and German final GDP was revised higher

- .Upside in Equities have lagged momentum, although Mini S&P did print a new all time high this morning.

- Govies are back towards to top end of the ranges, but well within yesterday's price action.

- Peripheral spread are leaning tighter against the German 10yr.Spain and Italy lead, by 0.7bp tighter.

- Gilt has been dominated by more rolls this morning, with the front contract trading more volumes than Bund and similar to US Treasuries.

- More than half of the front month volumes is spread related.

- Looking ahead, we no real market moving data scheduled. ECB Schnabel in the panel "The implications of the rise in non-bank financial intermediation".

- But given the subject, shouldn't move the needle.

- The US President meets virtually with G7 leaders to discuss Afghanistan policy.

- And later today, Ursula von der Leyen and President of the European Council Charles Michel give joint press conference following the G7 leaders' meeting.

EUROPE ISSUANCE UPDATE

GILT AUCTION RESULTS: The DMO Sells GBP3bn of the 0.375% Oct-26 Gilt

- Average yield 0.324% (0.334%), bid-to-cover 2.11x (2.50x), pre-auction mid-price 100.24

GERMAN AUCTION RESULTS: Germany Allots E2.4797bn of the 0% Nov-28 Bund

- Average yield -0.65% (-0.58%), Buba cover 1.6x (1.57x), bid-to-cover 1.28x (1.32x), pre-auction mid-price 104.83

EUROPEAN OPTIONS SUMMARY

RXZ1 173.5/172.5ps vs 175/176cs, bought the ps for flat in 1k

3RZ1 100.25/100ps 1x2, bought for 2 in 2.5k

FOREX: USD Fades Some of its Weakness

- USD has pared some of its overnight and early morning losses, as Equities loses upside momentum.

- It is still worth noting that the Mini S&P printed another record high, trading just short of the next psychological target at 4500, printed 4492 high.

- The Dollar is now more mixed in G10, up 0.14% versus the EUR, and down 0.55% against the NZD.

- The Kiwi has been the standout currency during our morning European session.

- A weaker Dollar and overnight Retail Sales Ex inflation QoQ beat, has keep the currency underpinned.

- The Kiwi is up across the board in the majors, beside the KRW, just flat on the session.

- AUDNZD is through the August double bottom (1.0420) and the December low (1.0418), now lowest level since 13th April 2020.

- Next support in the pair is now at 1.0392.

- Looking ahead, we have very little in terms of market moving data.

- At 14.30BST/09.30ET The US President meets virtually with G7 leaders to discuss Afghanistan policy.

- And at 16.00BST/11.00ET: President of the European Commission Ursula von der Leyen and President of the European Council Charles Michel give joint press conference following the G7 leaders' meeting.

FX OPTION EXPIRY

Of note:EURUSD, light again for today, but we have 1.29bn from 1.23bn at 1.1700 (Thurs), and 1.44bn from 1.3bn at 1.1700 (Friday)

- EURUSD: 1.1725 (409mln), 1.1750 (569mln), 1.1775 (689mln)

- USDJPY: 109.45 (200mln), 109.65 (951mln), 109.90 (653mln)

- GBPUSD: 1.3700 (355mln)

- AUDUSD: 0.7300 (1.21bn)

- NZDUSD: 0.6900 (735mln), 0.6925 (260mln)

- USDCNY: 6.47 (645mln), 6.518 (1bn)

Price Signal Summary - USDCAD Shooting Star Reversal

- On the equity front, S&P E-minis have extended their recovery and traded at fresh all-time highs. This confirms a resumption of the underlying uptrend and attention turns to the 4500.00 handle. EUROSTOXX 50 key support has been defined at 4078.00, Aug 19 low.

- In the FX space, the USD remains in an uptrend and yesterday's weakness is considered corrective. EURUSD last week cleared 1.1704, Mar 31 low. This signals scope for a move to 1.1621 next, 1.00 projection of the Jan 6 - Mar 31 - May 25 price swing. Firm resistance to watch is 1.1805, Aug 13 high. GBPUSD remains vulnerable despite yesterday's strong bounce. The focus is on the bear trigger at 1.3572, Jul 20 low. Resistance is at 1.3786, Aug 18 high. USDCAD stalled last week at 1.2949, Aug 20 high. Friday's price pattern is a bearish shooting star candle and yesterday's weak close reinforces the bearish pattern. An extension would expose 1.2603, the 20-day EMA and potentially 1.2509, the 50-day EMA.

- On the commodity front, Gold has cleared its 50-day EMA at $1796.50. The break signals scope for a climb towards $1834.1, Jul 15 high and a bull trigger. WTI futures support has been defined at $61.74, Aug 23 low. Note, yesterday's price action appears to be a bullish engulfing reversal. Further gains would open $68.15, the 50-day EMA.

- In FI, Bunds support to watch is unchanged at 176.21, Aug 11 low. Trend conditions remain bullish. The bull trigger is 177.61, Aug 05 high. The Gilt futures outlook is bullish too and attention is on 130.72, Aug 4 high and the bull trigger. The support to watch is at 129.16, the 50-day EMA.

EQUITIES: S&P Eyes 4,500

- European stocks have had a mixed performance so far Tuesday, with materials / energy leading (on higher commodity prices) and utilities and healthcare dragging on the broader indices. The German Dax is last up 57.28 pts or +0.36% at 15852.79, FTSE 100 down 15.89 pts or -0.22% at 7109.02, CAC 40 down 22.53 pts or -0.34% at 6683.1 and Euro Stoxx 50 up 3.69 pts or +0.09% at 4176.42.

- U.S. futures are pushing to new highs, with the Dow Jones mini up 54 pts or +0.15% at 35335, S&P 500 mini up 7.75 pts or +0.17% at 4483.25, NASDAQ mini up 42.25 pts or +0.28% at 15346.75. The S&P contract is hitting fresh all-time highs and the uptrend remains intact, with the next target 4,500.00.

- Asian stocks closed higher, with Japan's NIKKEI up 237.86 pts or +0.87% at 27732.1 and the TOPIX up 19.06 pts or +1% at 1934.2. China's SHANGHAI closed up 37.339 pts or +1.07% at 3514.471 and the HANG SENG ended 618.33 pts higher or +2.46% at 25727.92.

COMMODITIES: Short-Term Oil Outlook Remains Bullish

Oil is a standout performer again Tuesday, up nearly $5/bbl from Monday's low ($61.74, which now represents support). Our tech analyst says the short-term outlook appears bullish with Monday's price pattern representing a bullish engulfing candle, with gains to the 20day EMA next up at $667.35.

- Elsewhere, iron ore is soaring (Singapore futures +10%) on rebounding economic optimism (some pointing to potential PBOC credit support).

Latest levels:

- WTI Crude up $0.96 or +1.46% at $66.34

- Natural Gas down $0.02 or -0.51% at $3.931

- Gold spot down $0.34 or -0.02% at $1803.95

- Copper up $3.4 or +0.81% at $423.35

- Silver up $0.1 or +0.43% at $23.7033

- Platinum up $5.11 or +0.5% at $1020.45

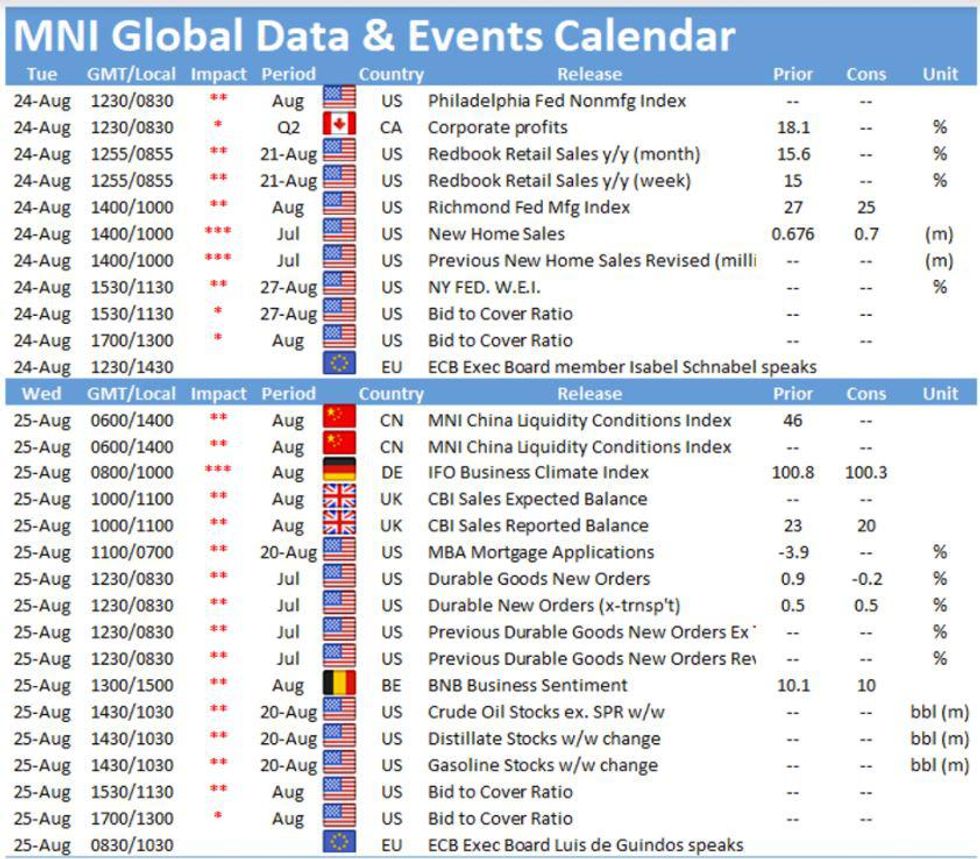

LOOK AHEAD

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok