Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

Highlights:

- Markets on a firmer footing after First Republic deposit plan, ECB rate decision

- PBoC takes action to shore up local bank liquidity

- Prelim inflation expectations take focus in UMich sentiment survey

US TSYS: A Calmer Start To The Day, Awaiting Further Bank News

- Cash Tsys see a mild rally on the day in a move that only chips away at yesterday’s sell-off on major US banks coordinating support for First Republic, with today’s PBOC RRR cut for banks potentially providing a modest tailwind to rates. Futures volumes are low by this week’s standards as we await further drivers, likely from banks, as the US session starts to get underway.

- 2YY -1.9bp at 4.138%, 5YY -4.5bp at 3.691%, 10YY -4.9bp at 3.530% and 30YY -3.8bp at 3.660%.

- TYM3 trades 9+ ticks higher at 114-15+ as it drifts upwards within a relatively tight 20 tick range to date. Cumulative volumes are low by this week’s standards, at a more typical 300k so far. The outlook remains bullish with resistance seen at 116-01 (Mar 16 high) whilst support is seen at 113-28 ((38.2% retrace of rally from Mar 2, cont).

- Data: IP for Feb after continued weakness of manufacturing surveys (0915ET), Conf Board Leading Index for Feb (1000ET) and U.Mich preliminary consumer survey for March (1000ET).

- Bill issuance: US Tsy $60B 4W, $50B 8W bill auctions (1000ET)

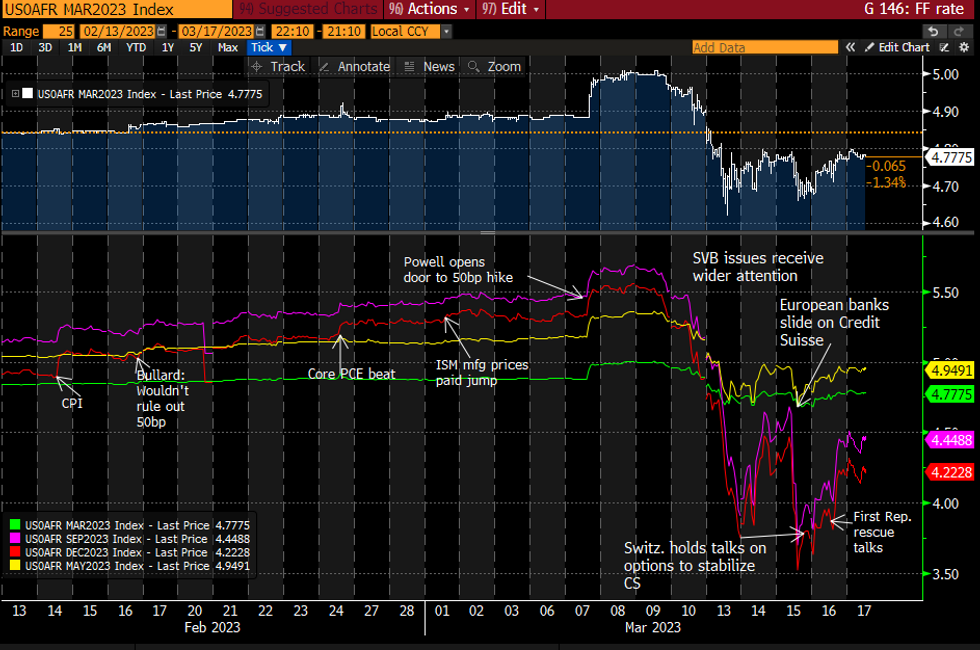

STIR FUTURES: Fed Rate Path Holds Higher But Still Nearly 75bps Of Cuts

- Fed Funds implied hikes are off overnight highs but have still pushed on from yesterday’s close.

- 21bp for next week’s FOMC (+1bp), having not sustainably fully priced a 25bp hike this week, before a cumulative 39bp to a peak 4.96% for May (+3.5bp).

- July and Sept meetings have seen the largest increases on the day (+9/8bp) but a smaller rise in the Dec rate of 4.24% (+4.5bp) broadly maintains 72bps of cuts from peak to year-end after yesterday’s 33bp trimming on First Republic rescue talks and subsequent action from major US banks.

FOMC-dated Fed Funds futures implied ratesSource: Bloomberg

FOMC-dated Fed Funds futures implied ratesSource: Bloomberg

ECB: Limited Early TLTRO Repayments Seen This Month Amid Bank Stresses

Reminder that the announcement of early TLTRO repayments for March are announced at 1105GMT/1205CET.

- Fairly low takeup is expected given ongoing systemic liquidity concerns (banks had to tell the ECB on Wednesday how much they wanted to repay).

- Prior to the recent banking uncertainty there had been speculation that takeup could be fairly sizeable in March.

- The most recent Bloomberg survey median for early repayments was E25bln (high E125bln, low E10bln). By comparison, E36.6bln was repaid early in February's window.

US 10y Techs: Outlook Remains Bullish

- RES 4: 117-00 61.8% of the Aug - Oct 2022 bear leg (cont)

- RES 3: 116-28+ High Jan 19 and key resistance

- RES 2: 116-08 High Feb 2

- RES 1: 116-01 High Mar 16

- PRICE: 114-12+ @ 10:16 GMT Mar 17

- SUP 1: 113-28 38.2% retracement of the rally from Mar 2 (cont)

- SUP 2: 113-06+ 50-day EMA

- SUP 3: 112-27 20-day EMA

- SUP 4: 112-17+ 61.8% retracement of the rally from Mar 2 (cont)

Treasury futures failed to hold on to yesterday’s high of 116-01. Despite the pullback, a bullish short-term outlook remains intact. Key support to watch lies at 113-06+, the 50-day EMA and this level also represent a short-term pivot level. A break of yesterday’s high would open 116-08, the Feb 2 high and 116-28+, the Jan 19 high and a key resistance. On the downside, a clear breach of the 50-day EMA would expose 112-21, the Mar 13 low.

RATINGS: Friday’s Sovereign Rating Slate

Sovereign rating reviews of note slated for after hours on Friday include:

- Fitch on Turkey (current rating: B; Outlook Negative)

- Moody’s on Greece (current rating: Ba3; Outlook Stable) & Luxembourg (current rating: Aaa; Outlook Stable)

- S&P on Belgium (current rating: AA; Outlook Stable), Croatia (current rating: BBB+; Outlook Stable) & Spain (current rating: A; Outlook Stable)

- DBRS Morningstar on Latvia (current rating: A, Stable Trend) & the Netherlands (current rating: AAA, Stable Trend)

FOREX: CNH Edges Off Highs as PBoC Look to Shore Up Liquidity

- The Chinese currency trades softer after the PBoC announced a 25bps cut to the reserve requirement ratio, effective March 27th. While policy action was expected, the decision may be coming sooner-than-expected, as Chinese authorities look to shore up banking sector liquidity given the recent spell of global uncertainty.

- Spot USD/CNH trimmed losses on the headline, with bears looking for a break below the 50-DMA at CNH6.8375 after piercing that moving average but failing to close below it on Mar 13. USD/CNY sits -127 pips at CNY6.8853 and bears would be pleased by a move through the 50-DMA, which intersects at CNY6.8438. Below there we have a key trendline which capped gains in December and then turned into a support this year, it kicks in at CNY6.8242.

- The greenback is weaker, extending the recovery in the major pairs off yesterday's lows, as the risk drop takes a breather and allows equities to hover close to the week's best levels.

- Elsewhere, NOK trades well, with USD/NOK over 1% lower on the day amid a stabilising oil price and local rate re-pricing. Prices are still some way off testing the next key support at 10.5105, the Wednesday low - and slippage here would open 10.4563, the 38.2% Fib for the Jan - Mar upleg. Norges Bank pricing took a knock late last week/early this week alongside the global rate re-pricing, but has recovered off lows, with the 3x6 NOK FRA clearing 3.50% today for the first time since late November.

- Focus Friday turns to final revisions for February Eurozone CPI and the prelim reading for the Uni of Michigan sentiment survey.

FX OPTIONS: Expiries for Mar17 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0500(E1.2bln), $1.0660-80(E1.7bln), $1.0690-10(E5.1bln), $1.0775(E1.4bln)

- USD/JPY: Y130.00($3.3bln), Y130.92-00($937mln), Y132.00($1.7bln), Y133.00-10($2.0bln), Y133.60-68($698mln), Y134.00-20($1.2bln), Y134.90-00($1.5bln)

- EUR/JPY: Y131.00(E1.0bln)

- AUD/USD: $0.6580(A$831mln), $0.6650(A$1.1bln), $0.6700(A$611mln)

- USD/CNY: Cny6.8500($1.5bln)

EQUITIES: E-Mini S&P Trade Above $4000 Despite Bearish Technical Conditions

- The Eurostoxx 50 futures outlook remains bearish following recent weakness and Wednesday’s strong sell-off reinforces the current bear cycle. Short-term gains are considered corrective. The break of the 4000.00 handle signals scope for weakness towards 3865.00, the Jan 4 low and further out towards the 3800.00 handle. Initial resistance is seen at 4143.60, the 20-day EMA. Key resistance has been defined at 4268.00, the Mar 6 high.

- The trend condition in S&P E-Minis remains bearish and recent short-term gains are considered corrective. Price recently cleared a key short-term support at 3960.75, Mar 2 low to confirm a resumption of the bear cycle that has been in place since Feb 2. The move lower signals scope for an extension towards 3822.00 next, the Dec 22 low. Initial firm resistance is seen at 4030.01, the 50-day EMA.

COMMODITIES: Gold Trades Close to Recent Highs, Targets $1959.7 Feb 2 High

- WTI futures remain vulnerable. Wednesday’s move lower resulted in the break of key support at $70.86, the Dec 9 low. The breach confirms a resumption of the medium-term downtrend and reinforces current bearish conditions. Note too that price has also cleared the psychological $70.00 handle. Attention is on $65.60, the Dec 3 2021 low. Initial resistance is at $72.56, Wednesday’s high.

- Gold remains bullish and the metal is trading at its recent highs. Resistance at $1858.3, the Mar 6 high, has recently been cleared and the latest rally signals scope for an extension towards $1959.7, the Feb 2 high and a key near-term resistance. On the downside, initial firm support is seen at $1854.6, the 50-day EMA. A break of this level is required to signal a top - this would expose the bear trigger at $1804.9, the Feb 28 low.

| Date | GMT/Local | Impact | Flag | Country | Event |

| 17/03/2023 | 0700/0800 | ** |  | SE | Unemployment |

| 17/03/2023 | 0930/0930 | ** |  | UK | Bank of England/Ipsos Inflation Attitudes Survey |

| 17/03/2023 | 1000/1100 | *** |  | EU | HICP (f) |

| 17/03/2023 | 1230/0830 | * |  | CA | International Canadian Transaction in Securities |

| 17/03/2023 | 1230/0830 | * | | CA | Industrial Product and Raw Material Price Index |

| 17/03/2023 | 1315/0915 | *** |  | US | Industrial Production |

| 17/03/2023 | 1400/1000 | *** | | US | University of Michigan Sentiment Index (p) |

| 20/03/2023 | 0700/0800 | ** |  | DE | PPI |

| 20/03/2023 | 0730/0730 | | UK | DMO to Confirm Gilts on Offer at 4/5 April Auctions | |

| 20/03/2023 | 1000/1100 | * | | EU | Trade Balance |

| 20/03/2023 | - | | UK | DMO Quarterly Consultation with GEMMs / Investors | |

| 20/03/2023 | 1400/1500 | | EU | ECB Lagarde Intro at ECON Hearing | |

| 20/03/2023 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 20/03/2023 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 20/03/2023 | 1600/1700 | | EU | ECB Lagarde Intro as ESRB Chair at ECON |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.