Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

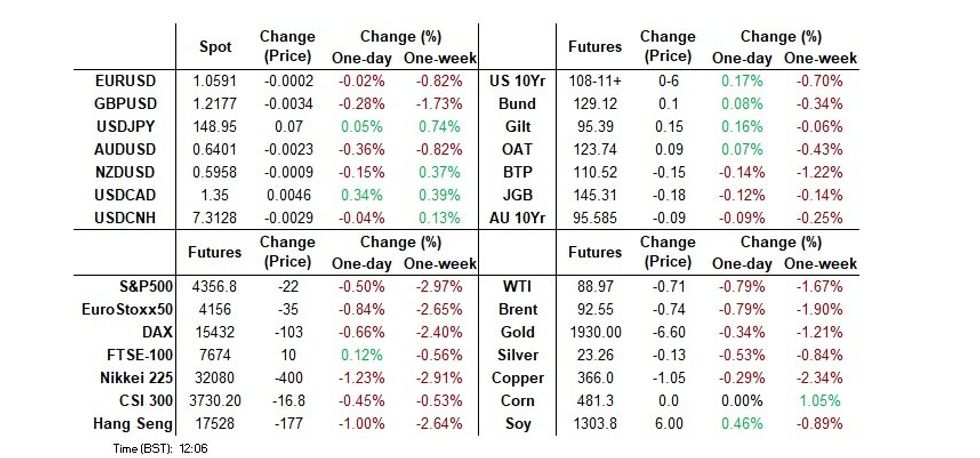

- Fresh highs for the BBDXY, owing to the early risk-off tone and higher Tsy yields, have given way amd the USD is now more mixed against G10 peers, with equities and core global FI off session lows.

- China worry, higher for longer narratives and German issuance plans provided the highlights of discussions in early European trade.

- Speakers due during the remainder of the session include Riksbank's Jansson, ECB's Holzmann and Fed's Bowman.

US TSYS: Bull Flatter Through London Trade - Data, 2Y Supply And Bowman Ahead

- After the 10Y yield touched fresh cycle highs in Asia hours, cash Tsys have since bull flattened through London hours to chip away at yesterday’s more notable bear steepening.

- Benchmarks range from 0.5bp to 2.5bp richer to leave 2s10s still elevated (by recent standards) at -61bps off latest highs of -58bps.

- TYZ3 trades 00-6+ higher at 108-12 for 1 tick below session highs, on decent volumes of 380k. It’s back within yesterday’s range after earlier extending lows with 108-00+ to build on yesterday’s clearance of 108-08. Resistance is seen at the round 108-00 after which lies 107-23 (1.236 proj of Jul 18 – Aug 4 – Aug 10 price swing).

- Today sees a range of data releases covering housing activity/prices and business & consumer surveys, before further Fedspeak from Gov. Bowman at 1330ET.

- Note/bond issuance: US Tsy $48B 2Y note auction (1300ET). 2Y yields have pulled back from post FOMC highs nearing 5.20% to currently 5.12%.

- Bill issuance: US Tsy $60B 42D bill CMB auction (1130ET)

US TSY FUTURES: Short Setting Seemed To Dominate On Monday

The combination of yesterday’s bear steepening of the curve and preliminary open interest data point to fresh short setting being the dominant factor from a positioning perspective on Monday.

- Net DV01 equivalent OI of ~$9.3mn was added across the curve, with the most sizable move coming in FV futures.

| 25-Sep-23 | 22-Sep-23 | Daily OI Change | OI DV01 Equivalent Change ($) | |

| TU | 3,885,976 | 3,855,156 | +30,820 | +1,166,122 |

| FV | 5,581,989 | 5,511,439 | +70,550 | +2,968,033 |

| TY | 4,727,455 | 4,724,663 | +2,792 | +179,451 |

| UXY | 1,860,056 | 1,848,157 | +11,899 | +1,070,261 |

| US | 1,397,347 | 1,380,315 | +17,032 | +2,201,865 |

| WN | 1,542,505 | 1,533,749 | +8,756 | +1,703,649 |

| Total | +141,849 | +9,289,381 |

STIR: Fed Rate Path Treading Water

- Fed Funds implied rates are near unchanged after a lacklustre session yesterday that helped limit the front end of the Treasury curve yesterday to exacerbate the bear steepening. With data in the driving seat, today sees various housing releases plus business and consumer surveys.

- The terminal is still seen at 5.45% in Jan (cumulative +12bp), after which lies a cumulative 24bp of cuts to Jun’24 and 78bp of cuts to Dec’24 – see table.

- Kashkari (’23 voter) late yesterday said he was one of 12 policymakers who pencilled in one more rate hike this year at last week’s dot plot. He added that there may be a need for higher rates for longer if the economy is too strong but there may also be a need to cut rates if real rates are tightening.

- Ahead, Gov. Bowman (voter) gives welcoming remarks at an event on rental housing affordability with text at 1330ET. She has already implied she was the lone dot at 6.1% for end-2024.

STIR: Mixed SOFR Positioning Swings On Monday

Preliminary open interest data and yesterday’s twist steepening of the curve points to the following SOFR positioning swings on Monday:

- Whites: short cover in SFRU3, questions over positioning moves in SFRZ3, SFRH4 & SFRM4 given unchanged prices.

- Reds: net short setting for the pack, although there was seemingly a mix of long cover and short additions across contracts.

- Greens: apparent short setting and long cover virtually offset.

- Blues: marginal net short setting in the pack.

| 25-Sep-23 | 22-Sep-23 | Daily OI Change | Daily OI Change In Packs | ||

| SFRU3 | 1,044,965 | 1,066,982 | -22,017 | Whites | -3,061 |

| SFRZ3 | 1,319,219 | 1,311,713 | +7,506 | Reds | +10,007 |

| SFRH4 | 999,027 | 991,302 | +7,725 | Greens | -245 |

| SFRM4 | 899,511 | 895,786 | +3,725 | Blues | +2,160 |

| SFRU4 | 790,356 | 780,649 | +9,707 | ||

| SFRZ4 | 915,261 | 922,245 | -6,984 | ||

| SFRH5 | 544,039 | 535,940 | +8,099 | ||

| SFRM5 | 574,552 | 575,367 | -815 | ||

| SFRU5 | 500,276 | 501,109 | -833 | ||

| SFRZ5 | 500,204 | 505,880 | -5,676 | ||

| SFRH6 | 321,268 | 318,043 | +3,225 | ||

| SFRM6 | 251,701 | 248,662 | +3,039 | ||

| SFRU6 | 200,121 | 196,737 | +3,384 | ||

| SFRZ6 | 181,049 | 183,188 | -2,139 | ||

| SFRM7 | 131,518 | 131,020 | +498 | ||

| SFRU7 | 134,782 | 134,365 | +417 |

FOREX: USD Paring Gains Going Into NY Session

After being in the green across the board, owing to the early risk-off tone and higher Tsy yields, the USD is now more mixed against G10 peers, with equities and core global FI off session lows.

- The yen saw a brief bid on the back of the latest offerings from Japanese Finance Minister Suzuki, but USD/JPY has unwound some of the limited knee-jerk lower to last trade around Y148.90. Highs of Y149.19 seen thus far. Resistance beyond today's high is seen at Y149.71, the Oct 24 2022 high, but the wider focus is on Y150.00.

- The SEK is the best performer and looking to test the SEK11.00 support after USD/SEK traded as high as SEK11.1022 earlier.

- EUR/USD has seen a two way price action, initially falling on the USD bid, but now back at $1.06, with option expiries at the figure eyed at today's 10AM NY cut.

- Speakers due during the remainder of the session include Riksbank's Jansson, ECB's Holzmann and Fed's Bowman.

CNH: Pre-Holiday Resilience Noted

USD/CNH looks to the move away from best levels in the USD, testing early Asia-Pac lows, but sticking to a contained range thus far.

- The redback had outperformed peers, with USD/CNH flat to a touch lower on the day during the Asia/early Europe bid in the USD.

- We note a couple of factors here:

- The mid-point USD/CNY fixing saw the PBoC deploy another record lean against CNY weakness (as monitored by the spread between the sell-side estimate provided by BBG and actual fixing outcome).

- An apparent focus on FX stability ahead of the Golden Week holiday.

- Well-documented Chinese economic headwinds remain evident. The latest survey from the Securities Times indicated Q3 GDP growth levels of sub-5%, although there seems to be continued hope of an economic rebound in Q4, keeping the official ’23 GDP target of around 5% in play.

- Well-defined technical parameters remain in place for USD/CNH:

- Key short-term support in USD/CNH lies at CNH7.2392, the Sep 1 low.

- For bulls, a break of resistance at CNH7.3682, the Sep 8 high, would resume the uptrend and open CNH7.3749, the Oct 25 high - a major resistance and the all-time high.

FX OPTIONS: Expiries for Sep26 NY cut 1000ET (Source DTCC)

- EURUSD: 1.0520 (964mln), 1.0575 (515mln), 1.0600 (1.56bn), 1.0650 (433mln), 1.0655 (500mln), 1.0700 (1.53bn)

- USDJPY: 148.50 (260mln)

- USDCAD: 1.3500 (1.35bn)

- AUDUSD: 0.6400 (600mln), 0.6455 (325mln), 0.6460 (223mln)

- USDCNY: 7.25 (930mln), 7.2795 (992mln), 7.3000 (354mln), 7.3200 (312mln), 7.3500 (1.05bn)

- EURSEK: 11.75 (720mln)

EQUITIES: EUROSTOXX 50 Heads South

- A bear cycle in the E-mini S&P contract remains in play and the price traded lower Monday. Last Thursday’s sell-off resulted in a break of support at 4397.75, the Aug 18 low. This breach reinforces bearish conditions and signals scope for a continuation lower. Sights are on 4318.00 next, the Jun 2 low. Initial firm resistance is 4492.05, the 50-day EMA. Short-term gains would be considered corrective.

- EUROSTOXX 50 futures maintain a softer tone following last week’s move lower, and Monday's extension reinforces current conditions. Key support at 4210.00, the Sep 8 low, has been breached. The clear break confirms a resumption of the downtrend that started late July and paves the way for a move towards 4109.90, the 1.236 projection of the Aug 10 - 18 - 30 price swing. Key short-term resistance has been defined at 4359.00, the Sep 15 high. Initial firm resistance is at 4279.40 the 20-day EMA.

CHINA STOCKS: On The Backfoot, Again

The CSI 300 closed below 3,700, nearing ’23 lows (-0.6%), while the Hang Seng printed at the lowest level seen since November (closing -1.5%), as did the HSCEI.

- Well-documented Chinese economic headwinds remain evident, pressuring equities. The latest survey from the Securities Times indicated Q3 GDP growth levels of sub-5%, although there seems to be continued hope of an economic rebound in Q4, keeping the official ’23 GDP target of around 5% in play.

- Property developer names continued to struggle, with a BBG index monitoring Chinese property developers retesting YtD lows.

- Flow wise, we saw another day of net selling of mainland equities via the HK-China Stock Connect schemes (~CNY6.3bn).

- Participants are now generally focused on Chinese economic performance during the impending Golden Week holiday period, which will see mainland markets closed from the end of Thursday trade through next week.

- Official PMI data will cross on Saturday, with the Caixin equivalents due to hit on Sunday.

COMMODITIES: Corrective Cycle In Oil Futures Remains In Play

- Gold traded higher last Wednesday from the session high. The yellow metal maintains a bearish theme and this week’s move lower reinforces this. Attention is on $1901.1, the Sep 14 low. This level marks a key near-term support and a breach would strengthen a bearish theme and expose $1884.9, the Aug 21 low. Resistance is at $1947.5, the Sep 20 high.

- The uptrend in WTI futures is intact, however, the contract has entered a short-term bearish corrective cycle. Today’s move lower reinforces this theme. Note that the trend condition is overbought and a move lower would allow this to unwind. The first key support to watch lies at $87.17, the 20-day EMA and is a potential short-term objective. On the upside, clearance of $92.43, the Sep 19 high, would confirm a resumption of the uptrend.

| Date | GMT/Local | Impact | Flag | Country | Event |

| 26/09/2023 | 1230/0830 | ** |  | US | Philadelphia Fed Nonmanufacturing Index |

| 26/09/2023 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 26/09/2023 | 1300/0900 | ** | | US | S&P Case-Shiller Home Price Index |

| 26/09/2023 | 1300/0900 | ** | | US | FHFA Home Price Index |

| 26/09/2023 | 1300/0900 | ** | | US | FHFA Home Price Index |

| 26/09/2023 | 1400/1000 | *** | | US | New Home Sales |

| 26/09/2023 | 1400/1000 | *** | | US | Conference Board Consumer Confidence |

| 26/09/2023 | 1400/1000 | ** | | US | Richmond Fed Survey |

| 26/09/2023 | 1430/1030 | ** | | US | Dallas Fed Services Survey |

| 26/09/2023 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 26/09/2023 | 1700/1300 | * | | US | US Treasury Auction Result for 2 Year Note |

| 26/09/2023 | 1730/1330 | | US | Fed Governor Michelle Bowman | |

| 27/09/2023 | 0130/1130 | *** |  | AU | CPI Inflation Monthly |

| 27/09/2023 | 0600/0800 | * |  | DE | GFK Consumer Climate |

| 27/09/2023 | 0600/1400 | ** |  | CN | MNI China Liquidity Survey |

| 27/09/2023 | 0645/0845 | ** |  | FR | Consumer Sentiment |

| 27/09/2023 | 0700/0900 | ** |  | SE | Economic Tendency Indicator |

| 27/09/2023 | 0800/1000 | ** |  | EU | M3 |

| 27/09/2023 | 0900/1000 | ** |  | UK | Gilt Outright Auction Result |

| 27/09/2023 | 1100/0700 | ** | | US | MBA Weekly Applications Index |

| 27/09/2023 | 1230/0830 | ** | | US | Durable Goods New Orders |

| 27/09/2023 | 1430/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 27/09/2023 | 1530/1130 | ** | | US | US Treasury Auction Result for 2 Year Floating Rate Note |

| 27/09/2023 | 1700/1300 | * | | US | US Treasury Auction Result for 5 Year Note |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.