Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS:

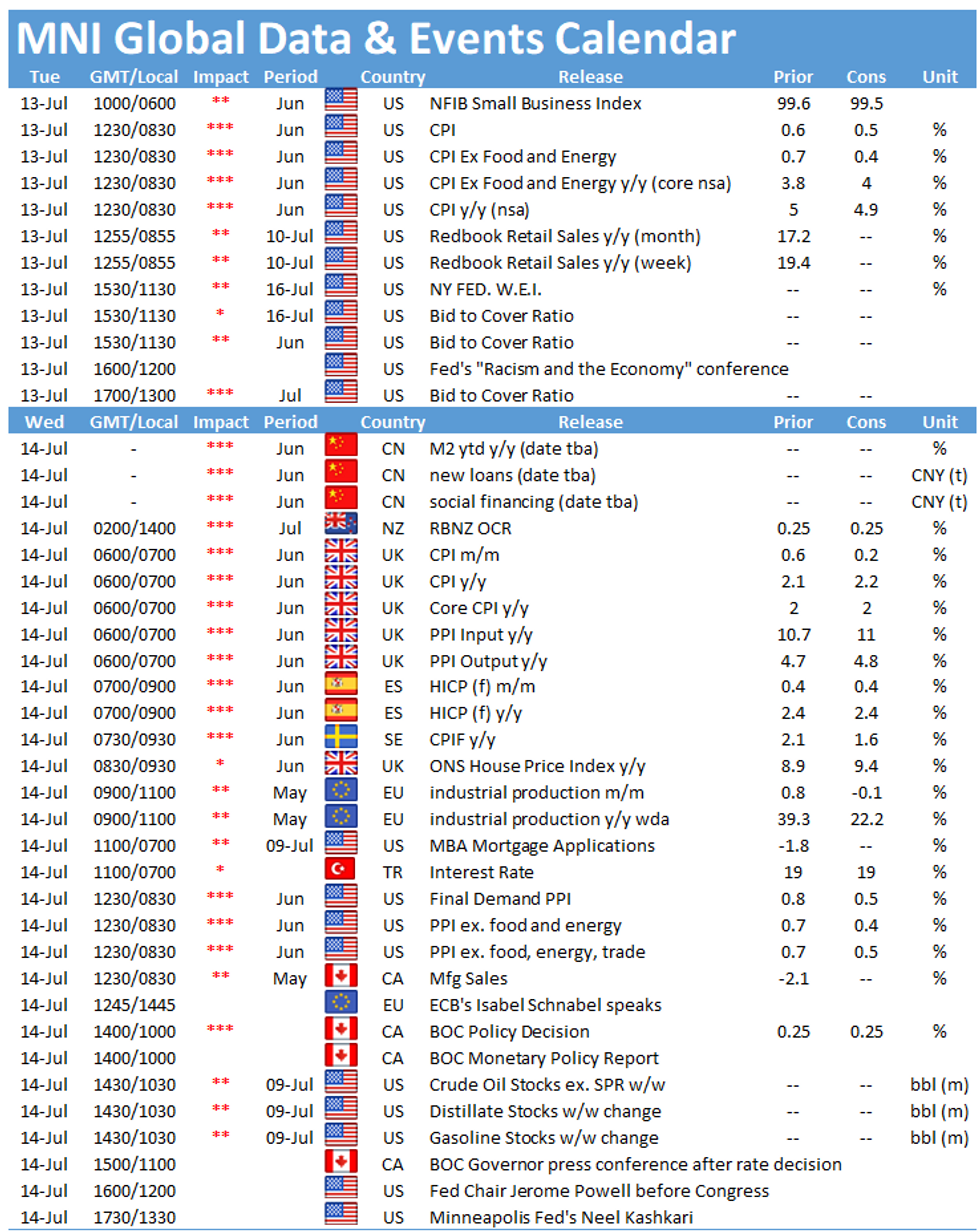

- Treasuries, USD in a tight range pre-Inflation release

- Eyes on CPI, with markets expecting a slowdown in price growth

- Earnings season kicks off, with JPM and GS both due Tuesday

US TSYS SUMMARY: Tight Ranges Ahead Of CPI, 30Y Supply

Tsys are off lows but flat overall in early Tuesday trade, with inflation data taking center stage shortly.

- Very moderate flattening in the curve thus far, with few macro catalysts overnight and the U.S. CPI report patiently awaited. The 2-Yr yield is up 0.4bps at 0.2308%, 5-Yr is down 0bps at 0.7945%, 10-Yr is down 0.5bps at 1.3594%, and 30-Yr is down 0.9bps at 1.9882%.

- Sep 10-Yr futures (TY) up 0.5/32 at 133-13.5, on weak volumes (~180k) and within the narrowest of ranges (L: 133-10 / H: 133-13.5)

- June headline CPI (0830ET/1330BST) slipping to +0.5% M/M vs +0.6% in May (and +4.9% Y/Y vs +5.0 prior), with core falling to +0.4% M/M vs +0.7% in May (though ticking up to a 30-yr high of +4.0% Y/Y vs +3.8% prior). We've put out a few sell-side expectations on our Bullets feed and IB.

- Apart from CPI, NFIB small biz optimism came in better than expected (102.5 vs 99.5 exp.). Monthly budget statement out at 1400ET.

- Supply takes focus later in the session: $34B 52-W and $35B 42-day bill auctions at 1130ET, and the $24B 30Y re-open at 1300ET. NY Fed buys ~$6.025B of 4.5-7Y Tsys.

- In Fed speak, Kashkari, Bostic and Rosengren attend an event on racism and the economy starting 1200ET. WSJ interviewed Bullard but nothing new there (though slightly notable that softer-than-expected recent econ data has not dissuaded him from taper talk / hike by end-2022).

EGB/GILT SUMMARY: Two "I"s: Inflation and Issuance

The focus for fixed income markets is on the two "I"s: inflation and issuance.

- The data calendar has already seen final prints of German and French HICP (inline with the flash estimates) but the real focus of the day will be on USCPI. The Bloomberg consensus looks for 0.5% M/M headline reading (although only 31/68 analysts forecast the 0.5% figure).

- There are almost as many forecasts for 0.4% and 0.6% with slightly more going for the higher print. For the ex-food and energy print, analysts are split between 0.4% and 0.5%M/M.

- It has also been a big day for issuance. The EU has held a dual-tranche transaction, selling E5.25bln of 10-year EFSM/MFA and E10bln of 20-year NGEU bonds. The UK a GBP7bln syndication for its new 1.125% Jan-39 gilt. The Netherlands and Italy have also held auctions for E2.42bln and E9bln respectively. Germany is still due to sell Schatz for E5bln and the US will reopen its 30-year bond for USD24bln.

- Against this backdrop core fixed income is largely unchanged on the day.

EUROPE ISSUANCE UPDATE:

Germany allots:

E3.999bln 0% Jun-23 Schatz, Avg yield -0.67% (Prev. -0.68%), Bid-to-cover 0.95x (Prev. 0.97x), Buba cover 1.18x (Prev. 1.19x)

Italy sells:

E4.5bln 0% Aug-24 BTP, Avg yield -0.19% (Prev. -0.22%), Bid-to-cover 1.34x (Prev. 1.35x)

E2.75bln 0.50% Jul-28 BTP, Avg yield 0.38% (Prev. -0.46%), Bid-to-cover 1.50x (Prev. 1.48x)

E1.75bln 0.95% Mar-37 BTP, Avg yield 1.19% (Prev. 1.26%), Bid-to-cover 1.54x (Prev. 1.47x)

Netherlands sells:

E2.415bln 3.75% Jan-42 DSL, Avg yield 0.113%

UK Syndication:

1.125% Jan-39: allocations out

Size set at GBP7bln, Spread set at 4.75%, Dec-38 Gilt +8.5bp (original guidance +8.5-9.0bps)

Books in excess of GBP60bln (inc JLM interest of GBP8.45bln)

EU 10/20-year dual-tranche syndication: Final terms

Guidance for the 10/20-year EU transaction has been issued:

- 10-year 22-Apr-2031 EFSM/MFA transaction, Size set yesterday at E5.25bln WNG

Spread set at MS-6bp (original guidance MS-4bps area)

Books over E47bln (ex JLM)

- 20-year 4-Jul-2031 NGEU, Size set yesterday at E10bln WNG

Spread set at MS +7bps (original guidance MS+9bps area)

Books over E81bln (ex JLM)

EUROPE OPTION FLOW SUMMARY

Eurozone:

RXU1 173/172ps 1x1.5, bought for 10 in 2k

3RU1 100.25/100.37cs vs 100.12/99.87ps, bought the cs for 3 in 2k (ref 100.25)

3RU1 100.25^ vs 100.37c, sold at 9.75 in 2k

3RZ1 100.12/99.87/99.62p fly sold at 2.5 in 1.5k

3RZ1 100.50c, sold at half in 2.5k

FOREX: USD Outlook Remains Constructive

- The USD outlook remains constructive, with European hours seeing some modest greenback buying against most other majors. EUR/USD and GBP/USD have been dragged off the overnight highs of 1.1875 and 1.3905 respectively, as markets also took the opportunity to keep the equity uptrend in tact. The e-mini S&P is already gravitating toward the alltime highs posted late Monday.

- Antipodean currencies continue to trade favourably, with the AUD and NZD among the strongest in G10 so far. Moves come ahead of the RBNZ rate decision due overnight, at which the bank are expected to open up the possibility of policy tightening to head off any simmering overheating pressures.

- CNH is firmer for a third consecutive session, with USD/CNH back below the 100-dma at pixel time. A break below 6.4586 would open further losses for the pair, with the 6.4354 level the next downside target.

- The June US CPI release is expected to slow slightly from the previous, with consensus seeing 0.5% M/M (Prev. 0.6%) and 4.9% Y/Y (Prev. 5.0%).

- Separately, the Fed are holding an event discussing racism and the economy from 1700BST/1200ET onwards. Fed's Kashkari, Bostic and Rosengren are due to appear.

FX OPTIONS: Expiries for Jul13 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1740-45(E1.2bln), $1.1875(E605mln), $1.1900-15(E1.3bln)

- USD/JPY: Y109.70-85($883mln), Y110.30($545mln)

- EUR/JPY: Y132.85(E536mln)

Price Signal Summary - S&P E-Minis Sights Set On 4400.00

- In the equity space, bullish conditions continue to dominate in the S&P E-minis and price continues to climb resulting in fresh all-time highs once again. With the bullish cycle still dominating, attention is on 4400.00 next. EUROSTOXX 50 futures recovered again yesterday extending the bounce from last week's low of 3951.50. The contract is approaching initial resistance at 4101.50, Jul 1 high where a break would neutralise recent bearish price signals and signal scope for a stronger recovery.

- In FX, the USD outlook remains bullish despite recent weakness. EURUSD is consolidating but remains below initial resistance at 1.1895, Jul 6 high. Attention is on 1.1782, Jul 7 low and the bear trigger. The GBPUSD outlook remains bearish. The focus is on the support and bear trigger at 1.3733, Jul 2 low. Resistance is at 1.3946, the 50-day EMA. USDJPY traded lower last week but found support at 109.53, Jul 8 low. The recent bear leg is considered corrective and a bullish theme remains intact. Initial resistance to watch is 110.82, Jul 7 high, a break would be bullish.

- On the commodity front, Gold continues to test the 50-day EMA, today at $1813.6. A clear break of the EMA is required to confirm the next leg higher and open $1833.7, 50.0% retracement of the Jun 1 - 29 decline. Brent (U1) futures have recovered from last week's lows. Key resistance is defined at $77.84, Jul 6 high with key support initially at $72.11, Jul 8 low. WTI (Q1) key resistance is at $76.98, Jul 6 high and the bull trigger. Initial firm support lies at 70.76, Jul 8 low.

- Within FI, Bund futures are unchanged and consolidating. Price has recently cleared key resistance at 173.16, Jun 11 high. The focus is on 174.97 High Mar 3 (cont). Gilt futures are off recent highs but maintain a bullish tone. Recent gains have resulted in a clear break of a key short-term resistance at 128.39, Jun 11 high. This has opened 129.99, Feb 24 high (cont).

S&P Futs Still Around All-Time Highs, With Earnings Looming

- Asian markets closed stronger, with Japan's NIKKEI up 149.22 pts or +0.52% at 28718.24 and the TOPIX up 14.31 pts or +0.73% at 1967.64. China's SHANGHAI closed up 18.686 pts or +0.53% at 3566.522 and the HANG SENG ended 448.17 pts higher or +1.63% at 27963.41.

- European equities are trading mixed but basically flat, with the German Dax down 5.51 pts or -0.03% at 15769.61, FTSE 100 up 21.52 pts or +0.3% at 7140.55, CAC 40 down 8.69 pts or -0.13% at 6550.52 and Euro Stoxx 50 down 0.19 pts or 0% at 4091.61.

- U.S. futures are flat, with the Dow Jones mini up 3 pts or +0.01% at 34878, S&P 500 mini up 0.5 pts or +0.01% at 4377, NASDAQ mini up 29.25 pts or +0.2% at 14898.5.

COMMODITIES: Oil Ticks Higher As Metals Stall

- WTI Crude up $0.58 or +0.78% at $74.52

- Natural Gas down $0.01 or -0.21% at $3.744

- Gold spot up $2.61 or +0.14% at $1811.55

- Copper down $1.75 or -0.41% at $432.55

- Silver up $0.04 or +0.14% at $26.3006

- Platinum down $2.81 or -0.25% at $1123.82

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.