Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Gilts outperform peers on wage metrics In BoE DMP survey.

- USD recovers from lows.

- ECB expected to deliver 25bp cut, U.S. weekly jobless claims also due.

US TSYS: Narrow Range Ahead ECB Rate Annc, Weekly Claims, ULC

- Treasuries are hovering around steady to mildly lower, inside a narrow overnight range as they trade off recent lows. Focus on upcoming ECB rate announcement at 0815ET, a well telegraphed rate cut widely anticipated.

- US Data follows with Weekly Claims, Unit Labor Cost and Trade Balance at 0830ET with the main focus on Friday's headline employment report for May (185k jobs gain anticipated vs. +175k prior).

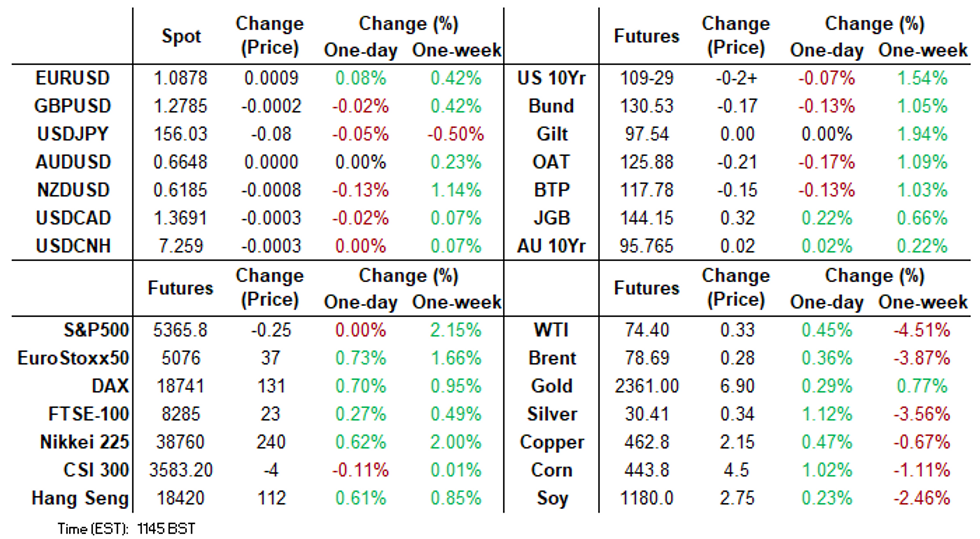

- Cash yields are currently mildly higher: 2s +.0081 at 4.7303%, 10s +.0135 at 4.2890%, 30s +.0102 at 4.4399%, while curves look steeper: 2s10s +0.547 at -44.340, 5s30s +0.074 at 13.455.

- Sep'24 10Y Treasury futures are trading -1 at 110-08.5 after trading 110-12 early overnight -- through the bull trigger at 110-09 next, the May 16 high. Next technical resistance at 110-17 (High Apr 4).

MNI ECB Preview - June 2024: Expect an Insurance Cut in June

A June cut has been so well-telegraphed by the ECB that failing to deliver would result in significant loss of credibility.

- However, uncertainties over inflation persistence, the geopolitical backdrop, and the outlook for global monetary policy (principally the Fed) suggest that the June decision will be no more than an insurance cut at this stage with no new policy signals.

- Although still a relatively low probability outcome for now, we cannot fully discount the potential for a ‘one and done’ rate cut in 2024.

- For the full publication please click here.

FOREX: EUR Vol Steady Ahead of the Awaited ECB

The dollar started the overnight and the early European session on the back foot, not too surprising given the risk on tone, and the push lower in yield in what has been a disappointing week on the data front for the US. Still, the greenback has recovered from session lows.

- US ISM Services and price paid was more mixed yesterday though, and attention will now turn towards the US NFP/AHE tomorrow for the US.

- For today, going into the ECB meeting when a 25bps cut is widely expected, and should happen unless the ECB wants to lose some credibility, EUR option vol has stayed fairly subdued ahead of the meeting.

- Early mover was again the yen during the early European session, with the yen paring most of its overnight gains, versus the EUR, GBP, USD and AUD.

- The resistance noted at 156.49, Tuesday's high, held yesterday, after printing a 156.48 high, and has held again today, only managing a 156.38 high print.

- Going into the US session, the Swissy is still the best performer against the greenback in G10.

- Looking ahead, main focus will be on the ECB and presser, while on the data front, US IJC, will be the only notable Data release.

FX OPTIONS: Expiries for Jun06 NY cut 1000ET (Source DTCC)

- EURUSD: 1.0830 (300mln), 1.0835 (384mln), 1.0840 (559mln), 1.0850 (758mln), 1.0860 (1.21bn), 1.0865 (463mln), 1.0895 (396mln), 1.0900 (2.12bn), 1.0905 (882mln), 1.0915 (1.57bn).

- USDJPY: 155.15 (1.23bn), 155.45 (1.32bn), 155.50 (1.13bn), 156.00 (758mln), 157.00 (1.52bn).

- USDCAD: 1.3675 (275mln), 1.3685 (340mln).

- AUDUSD: 0.6700 (519mln).

- USDCNY: 7.2450 (696mln), 7.2500 (262mln), 7.2550 (896mln).

EUROPEAN ISSUANCE UPDATE

Bono/Obli/ObliEi Auction Results

- E1.98bln of the 2.50% May-27 Bono. Avg yield 3.039% (bid-to-cover 1.81x).

- E2.001bln of the 0.10% Apr-31 Obli. Avg yield 3.003% (bid-to-cover 1.72x).

- E1.884bln of the 4.00% Oct-54 Obli. Avg yield 3.853% (bid-to-cover 1.53x).

- E510mln of the 2.05% Nov-39 Obli-Ei. Avg yield 1.392% (bid-to-cover 1.95x).

OAT Auction Results

- E7.174bln of the 3.00% Nov-34 OAT. Avg yield 3.05% (bid-to-cover 1.97x).

- E2.87bln of the 1.25% May-38 OAT. Avg yield 3.21% (bid-to-cover 2.33x).

- E1.959bln of the 3.25% May-55 OAT. Avg yield 3.46% (bid-to-cover 2.86x).

EGBS: Weaker As Markets Await Likely ECB Cut

Core/semi-core EGBs are weaker this morning, trading in a similar fashion to Tsys and widening vs. gilts, as markets await the ECB decision at 1315 BST.

- A 25bp cut is unanimously expected and ~95% discounted by OIS.

- Our full preview of the event is available here.

- Although German factory orders data was weaker-than-expected, the resulting rally in bonds was small and short-lived, with the details of the data a little more upbeat than the soft headline readings.

- This morning’s Spanish and French supply will have weighed in the run-up to the bidding deadlines, countering any impact from the softer than expected Eurozone retail sales reading.

- Bund futures are -36 ticks at 131.13, near the the low of today’s 39-tick range.

- The contract sticks comfortably within yesterday’s boundaries.

- The German cash curves has bear steepened.

- 10-year peripheral spreads are generally little changed vs. Bunds, except for BTPs, which sit slightly tighter.

GILTS: Dip In DMP Wage Expectations Provides Support, A Little Under 40bp Of '24 BoE Cuts Priced

The decline in the expected wage growth metrics in the latest BoE DMP survey supports gilts and allows SONIA futures to rally, with the news no doubt welcomed by the BoE (albeit with the pace in the moderation still being somewhat disappointing).

- That leaves yields flat to 6bp lower across the curve, bull steepening.

- Gilt futures still stick to a narrow 39-tick range.

- Tuesday’s low and high (97.08 & 97.86) present initial support and resistance, with recent gains in the contract still deemed corrective.

- SONIA futures are flat to +6.0 through the blues, with the reds leading the rally. Contracts are back from initial DMP-driven highs, operating in a similar manner to gilts.

- ~39bp of BoE cuts are priced through year end, with a little over 15bp showing through the Sep MPC and ~30bp of easing showing through the Nov meeting.

- More broadly, local headline flow remains centred on political matters, with the Conservatives still trailing heavily in the polls and Monday’s Sunak-Starmer debate still being assessed/critiqued.

- Further afield, the ECB’s latest monetary policy decision will provide the macro focal point today. Any guidance surrounding the future path of monetary policy is set to garner the most attention, assuming the widely telegraphed and expected 25bp rate cut is delivered

| BoE Meeting | SONIA BoE-Dated OIS (%) | Difference Vs. Current Effective SONIA Rate (bp) |

| Jun-24 | 5.197 | -0.3 |

| Aug-24 | 5.112 | -8.8 |

| Sep-24 | 5.029 | -17.1 |

| Nov-24 | 4.897 | -30.3 |

| Dec-24 | 4.812 | -38.8 |

UK DATA: DMP survey shows continued slow progress towards disinflationary pressures

The BOE DMP survey showed reducing pressure on wage growth, price growth and unit costs growth, but still only at a moderate pace. While expected employment growth remained steady and realised employment growth fell on a 3ma basis, but saw an uptick in the single month measure.

- The 3-month average of expected wage growth declined 0.3ppt to 4.5%/Y in the 3-months to May 2024, down from 4.8%Y/Y in the 3-months to April. The last three 3ma readings have now all been below 5%, and this followed 8 consecutive periods of either 5.1%Y/Y or 5.2%Y/Y (and was higher for the 10 periods before that). This is the lowest print of since the survey was begun in May 2022.

- Realised wage growth fell to 6.0%Y/Y in the 3-months to May, a 0.2ppt fall from April in a gradual decline seen since the 6.9%Y/Y in the 3-months to January (and from a peak of 7.0%Y/Y in the 3 months to November). This was the lowest since August 2022 (but the single month print increased to the same 6.1%Y/Y seen in March and 5.9%Y/Y - the first time it has been below 6% since July 2022).

- The single month figure for realised employment growth increased from 1.0% in April to 1.7% in May (returning to March levels). This was still below February's 2.3% print, however, so the 3-month average has fallen by 0.2ppt to 1.5% (and follows two consecutive falls of 0.3ppt). This is the lowest 3-month average since the 3-months to November 2021.

- Expected employment growth has remained steady at 1.3%Y/Y in the 3-months to May (and remaining below Nov23-Mar24 levels).

- Expected price growth declined further to 3.9% in the 3-months to May, down 0.1ppt from last month, and from a peak of 6.6%Y/Y in September 2022. The single month reading for mean expected price growth was 3.8%Y/Y in May, down from 4.2%Y/Y in April but a little higher than the 3.7%Y/Y in March.

- The survey also included questions on unit cost growth for the first time since July 2023. Realised unit cost growth was 6.2%Y/Y (down from 9.5%Y/Y in July 2023) while expected unit cost growth was 5.4%Y/Y (down from 6.8%Y/Y in July 2023).

EQUITIES: S&P E-Minis Resumes The Uptrend

- In the equity space, the uptrend in S&P E-Minis remains intact and this week’s gains reinforce this set-up. Price has traded above 5368.25, the May 23 high and bull trigger. The break confirms a resumption of the uptrend. A continuation higher would signal scope for a climb towards the 5400.00 handle next. On the downside, key short-term support has been defined at 5205.50, the May 31 low.

- Recent weakness in EUROSTOXX 50 futures appears to have been a correction. The recovery from 4947.00, the Jun 4 low, signals the end of the corrective cycle and a continuation higher would refocus attention on key resistance and the bull trigger at 5110.00, the May 16 high. Clearance of this level would confirm a resumption of the uptrend. Key support is 4947.00.

COMMODITIES: Oil Futures Remain Vulnerable

- On the commodity front, a short-term bear cycle in Gold remains in play for now. The medium-term trend structure is bullish and the recent move down appears to be a correction that is allowing an overbought condition to unwind. A resumption of gains would open $2452.5 next, the 2.618 projection of the Oct 6 - 27 - Nov 13 price swing. The 50-day EMA, at $2311.9, represents a key support.

- In the oil space, WTI futures have traded sharply lower this week and the contract remains soft. Price has cleared $73.24, the 76.4% retracement of the Dec 13 - Apr 12 bull leg. This reinforces the current bearish theme and signals scope for a continuation. Sights are on $71.33 next, the Feb 5 low. Initial resistance is at $76.15, the May 24 low and a recent breakout level.

| Date | GMT/Local | Impact | Flag | Country | Event |

| 06/06/2024 | 1215/1415 | *** |  | EU | ECB Deposit Rate |

| 06/06/2024 | 1215/1415 | *** | | EU | ECB Main Refi Rate |

| 06/06/2024 | 1215/1415 | *** | | EU | ECB Marginal Lending Rate |

| 06/06/2024 | 1230/0830 | *** |  | US | Jobless Claims |

| 06/06/2024 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 06/06/2024 | 1230/0830 | ** | | US | Trade Balance |

| 06/06/2024 | 1230/0830 | ** | | US | Non-Farm Productivity (f) |

| 06/06/2024 | 1230/0830 | ** |  | CA | International Merchandise Trade (Trade Balance) |

| 06/06/2024 | 1245/1445 | | EU | ECB Monetary Policy Press Conference | |

| 06/06/2024 | 1400/1000 | * | | CA | Ivey PMI |

| 06/06/2024 | 1415/1615 | | EU | ECB's Lagarde presents monpol decision on podcast | |

| 06/06/2024 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 06/06/2024 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 06/06/2024 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 07/06/2024 | 0600/0800 | ** |  | DE | Trade Balance |

| 07/06/2024 | 0600/0800 | ** | | DE | Industrial Production |

| 07/06/2024 | 0645/0845 | * |  | FR | Foreign Trade |

| 07/06/2024 | 0800/1000 | | EU | ECB's Schnabel participates in panel discussion at the Federal Ministry of Finance | |

| 07/06/2024 | 0900/1100 | *** | | EU | GDP (final) |

| 07/06/2024 | 0900/1100 | * | | EU | Employment |

| 07/06/2024 | - | *** |  | CN | Trade |

| 07/06/2024 | 1230/0830 | *** | | US | Employment Report |

| 07/06/2024 | 1230/0830 | *** | | CA | Labour Force Survey |

| 07/06/2024 | 1400/1000 | ** | | US | Wholesale Trade |

| 07/06/2024 | 1415/1615 | | EU | ECB's Lagarde in Atelier Maurice Allais | |

| 07/06/2024 | 1700/1300 | ** | | US | Baker Hughes Rig Count Overview - Weekly |

| 07/06/2024 | 1900/1500 | * | | US | Consumer Credit |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.