Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

Highlights:

- UK CPI tops forecast, markets hasten rate tightening expectations

- Treasury curve bear steepens ahead of retails, 20y sale and Fed minutes

- Futures indicate softer equity open after new S&P500 recovery high posted Tuesday

US TSYS SUMMARY: Bear Steepening With Retail Sales, 20Y Note And FOMC All Ahead

- Cash Tsys have cheapened in a move that was sparked by a strong beat for UK inflation in headline and core alike, building on yesterday’s strength in Canadian core CPI.

- It has helped the terminal rate implied by Fed Funds push back to pre-US CPI levels of 3.70%, more consistent with past FOMC commentary on the need for higher rates for longer, which rather than dampening growth expectations and weighing on long end yields, has instead seen the curve steepen a little further off recent lows with 2s5s at -28bps and 2s10s at -43bps.

- 2YY +3.2bps at 3.289%, 5YY +6.0bps at 3.103%, 10YY +5.8bps at 2.862% and 30YY +4.2bps at 3.131%.

- TYU2 trades 11+ ticks lower at 119-01, nudging support at 118-30+ (Aug 12 and Jul 22 lows). The move lower has been considered corrective but could extended with the opening of 118-05 (50% retrace of Jun 14 – Aug 2 bull cycle).

- Data: Retail sales for July headline plus business inventories for June and weekly MBA applications.

- Fed: FOMC minutes plus two appearances from Governor Bowman although topics could limit direct mon pol implications.

- Bond issuance: US Tsy $15B 20Y Bond auction (912810TK4) – 1300ET

- Bill issuance: US Tsy $30B 119D bill CMB auction – 1130ET

Source: Bloomberg

Source: Bloomberg

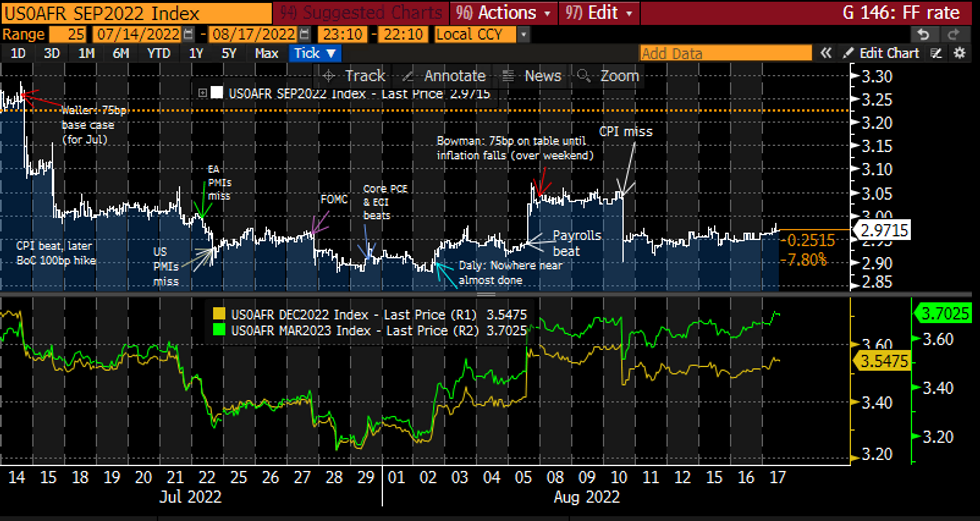

STIR FUTURES: Fed Hikes Firm With Spillover From UK CPI Beat

- Fed Funds implied hikes have firmed this morning, helped by a sizeable beat in UK inflation with double digit CPI adding to yesterday’s firming in Canadian core CPI even if headline cooled as expected. There was no immediate impact overnight from an expected 50bp RBNZ hike to 3% whilst seeing rates peak with a 4 handle.

- Sitting with 64bp for the Sept FOMC, a cumulative 121bp for Dec and 137bp to a peak of 3.70% in Mar’23 with just over 40bps of cuts to end-2023. The terminal rate has more than retraced the hit from last week’s CPI even if pricing for September still hasn’t.

- Ahead, FOMC minutes plus Governor Bowman either side on technology & financial services and Covid & women’s role in the economy, both with text and Q&A.

Cumulative hikes implied by FOMC-dated Fed Funds futuresSource: Bloomberg

Cumulative hikes implied by FOMC-dated Fed Funds futuresSource: Bloomberg

EGB/GILT SUMMARY: UK Inflation Surprises Higher To 40-Year High

European government bonds have sold off sharply this morning alongside losses for equities and G10 FX vs the dollar.

- UK inflation data surprised higher in July and has breached into double-digit territory for the first time in around 40 years. The headline print came in at 10.1% Y/Y (vs 9.8% expected) and marks a significant acceleration from the 9.4% reading from the previous month with no let up in the surge in the energy price component.

- Elsewhere, the ONS reported a slowdown in house price growth in June (7.8% Y/Y vs 12.8% the previous month).

- Gilts have progressively sold off through the morning with the curve sharply bear flattening. Cash yields are now 10-20bp higher on the day with the 2s30s spread 9bp narrower.

- The preliminary read on Eurozone GDP for the second quarter was a touch weaker than expected (0.6% Q/Q vs 0.7% & 3.9% Y/Y vs 4.0% survey).

- Bunds have lagged the move in gilts with cash yields up 7-13bp.

- OAT yields are up 5-12bp.

- BTPs have underperformed core EGBs with yields up 8-17bp.

- Focus later data shifts to US retail sales data for July.

FOREX: GBP Strength Limited as Yield Curve Aggressively Inverts

- GBP is stronger early Wednesday, with GBP/USD rallying to touch a react high of 1.2143 following the July CPI release which came in well ahead of expectations. Y/Y CPI surged to 10.1%, with core similarly rising ahead of forecast to again touch the highest levels since 1992. In response to the release, markets have brought forward their expectations for BoE policy in the coming quarters, and now see another 200bps of rate rises by the midpoint of 2023.

- Somewhat countering this hawkish outturn, however, is the continued curve inversion for the front end of the yield curve, reinforcing expectations for a looming recession in the UK. The 2y5y yield spread is now the most inverted since the Global Financial Crisis, limiting GBP's strength ahead of the NY crossover. The short-term trend outlook is bullish but a break of 1.2293 is required to reinforce this and signal a resumption of the bull cycle. A break would open 1.2406, the Jun 16 high. On the downside, clearance of support at 1.2004 would instead expose 1.1890, the Jul 21 low.

- NZD has entirely reversed initial strength garnered from the RBNZ rate decision overnight, at which the bank steepened their OCR track to bring forward the peak rate of 4% to Q2 next year. Initial NZD/USD strength (touching 0.6383) has unwound, putting the pair lower headed into NY hours.

- Lastly, AUD is the poorest performing currency in G10 as wage price index data fell short of forecast. EUR/AUD is now north of 1.46 and narrowing in on the early August highs at 1.4806.

- The US retail sales release takes focus going forward, with markets expecting the headline advance figure to have improved by 0.1% on the month. The FOMC minutes for their July meeting follow, due at 1900BST/1400ET. Central bank speakers today are limited to Fed's Bowman, who speaks on technology and women's role in the economy.

FX OPTIONS: Expiries for Aug17 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1000-15($1.2bln), $1.0190-00($727mln), $1.0300(E697mln)

- USD/CAD: C$1.2855($515mln), C$1.3065($864mln)

- USD/CNY: Cny6.7600-14($685mln)

Price Signal Summary – EUR/USD Fails to Clear Channel Resistance

- S&P E-Minis traded higher Tuesday and the outlook remains bullish. The move higher extends the positive price sequence of higher highs and higher lows. Moving average conditions are in a bull mode set-up too. Continued gains in EUROSTOXX 50 confirm a resumption of the current uptrend. The move higher maintains the bullish price sequence of higher highs and higher lows and attention is on resistance at 3840.00, the Jun 6 high.

- EURUSD remains below last week’s 1.0368 high (Aug 10). The recent move down appears to be a short-term reversal and means that the pair has failed to clear channel resistance. USDJPY traded higher Tuesday. Firm short-term resistance has been defined at 135.58, the Aug 8 high. The Aug 10 sell-off continues to highlight a reversal of the recent Aug 2 - 8 correction. The recent AUDUSD pullback is considered corrective - for now. The Aug 10 breach of 0.7047, Aug 1 high, confirmed a resumption of the uptrend that started Jul 14 and signals scope for a continuation higher.

- Gold is unchanged and the yellow metal maintains a bullish tone despite the latest retracement. Recent gains saw price trade above trendline resistance drawn from the Mar 8 high. WTI futures traded lower again Tuesday. This week’s move down has resulted in a print below support at $87.01, the Aug 5 low. The weakness reinforces bearish conditions and the break of $87.01 confirms a resumption of the downtrend.

- The recent retracement in Bund futures is still considered corrective and the short-term trend direction is up. Moving average studies are in a bull mode condition and the bullish price sequence of higher highs and higher lows is intact. Gilt futures still appear vulnerable. Last week’s extension lower resulted in a break of trendline support drawn from the Jun 16 low. The pullback this month is still considered corrective and the trend outlook remains bullish.

EQUITIES: Pulling Back On Higher Central Bank Hike Expectations

- Asian markets closed stronger: Japan's NIKKEI closed up 353.86 pts or +1.23% at 29222.77 and the TOPIX ended 25.03 pts higher or +1.26% at 2006.99. China's SHANGHAI closed up 14.641 pts or +0.45% at 3292.526 and the HANG SENG ended 91.93 pts higher or +0.46% at 19922.45.

- European futures are weaker, with the Health Care, Materials, and Industrials dragging down Eurostoxx: German Dax down 61.96 pts or -0.45% at 13847.56, FTSE 100 down 13.96 pts or -0.19% at 7521.73, CAC 40 down 18.73 pts or -0.28% at 6573.53 and Euro Stoxx 50 down 9.51 pts or -0.25% at 3795.33.

- U.S. futures are a little lower, with the Dow Jones mini down 85 pts or -0.25% at 34033, S&P 500 mini down 16.75 pts or -0.39% at 4291, NASDAQ mini down 69.75 pts or -0.51% at 13588.5.

COMMODITIES: Energy Rebounds, Metals Don't

- WTI Crude up $0.37 or +0.43% at $86.85

- Natural Gas up $0.07 or +0.74% at $9.397

- Gold spot down $1.23 or -0.07% at $1774.56

- Copper down $2.5 or -0.69% at $359.85

- Silver down $0.16 or -0.78% at $19.9923

- Platinum down $7.62 or -0.81% at $930.79

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok