Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS:

- NEW: USD/JPY, Treasury Yields, Equities slip as CDC moves to recommend a pause in the rollout of J&J's COVID vaccine

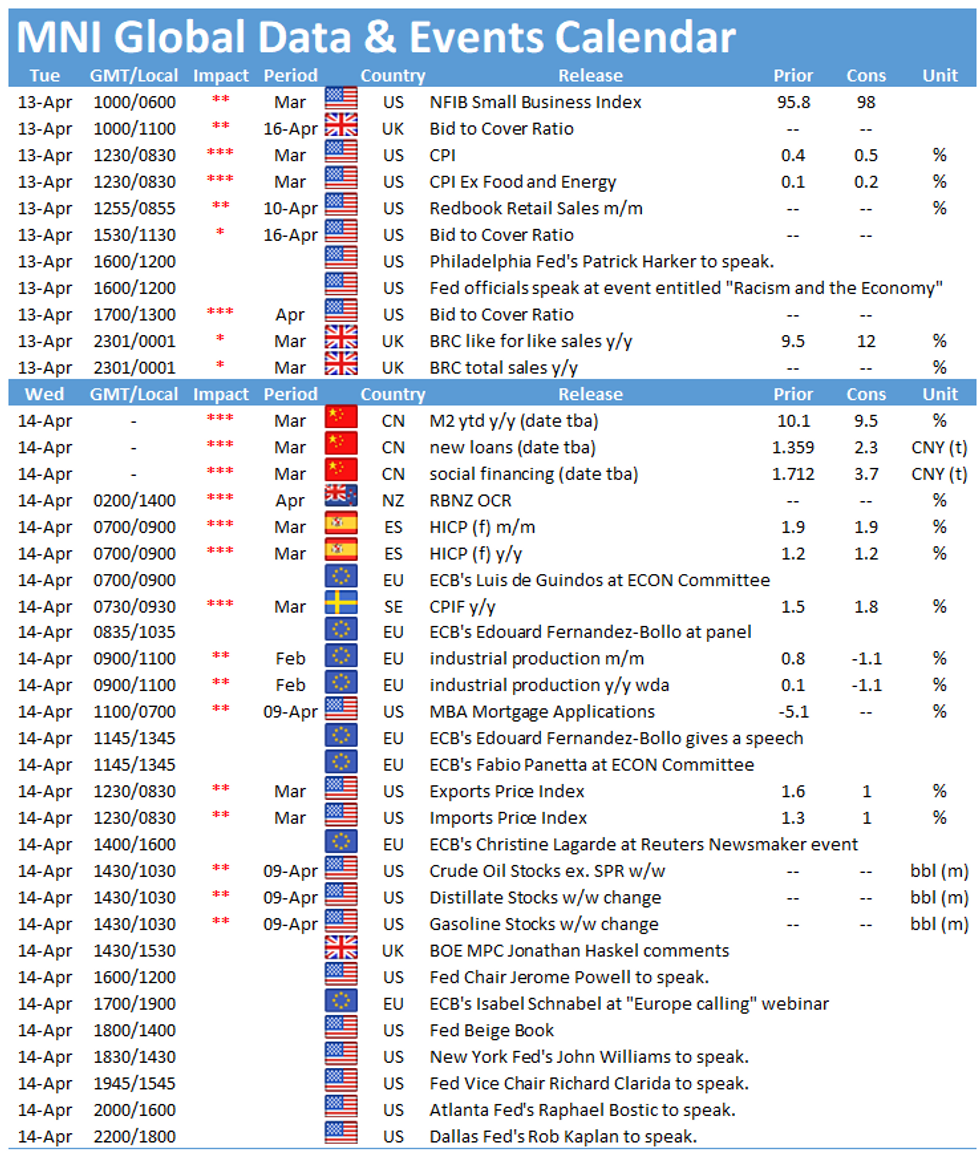

- CPI Y/Y expected to rise to 2.5%, highest since January 2020

- No fewer than six FOMC members due to speak Tuesday

CROSS ASSET: J&J Vaccine Pause in the US Prompts Risk Unwind

- New York Times reports that the US are to call for a pause in the rollout of the Johnson & Johnson vaccine on clotting cases, prompting some risk unwind trade over the past few minutes.

- The e-mini S&P inches back into negative territory and touches 4,101.25. Tsy yields move in tandem, with 10y slipping through 1.66% on the way lower.

- USD/JPY falls further, with the pair narrowing the gap with Y109.00 handle and falling through 109.25 support.

US TSYS SUMMARY: Tsys Lower Pre-CPI, Supply, And Possible Asset Purchase Tweaks

- A bit of bear steepening in the curve: the 2-Yr yield is up 0.6bps at 0.1729%, 5-Yr is up 2.1bps at 0.9017%, 10-Yr is up 2bps at 1.6854%, and 30-Yr is up 1.3bps at 2.3465%. Jun 10-Yr futures (TY) down 4/32 at 131-16 (L: 131-12 / H: 131-23.5)

- The focal point of the session is the 0830ET release of March CPI data. Earlier, NFIB small biz optimism came in at 98.2 in March (vs 98.5 exp.)

- A slew of Fed speakers, too, though we've heard from all of them recently. Separately at 1200ET are Philly's Harker and Richmond's Barkin, while KC Pres George intros a Minn Fed event on "Racism and the Economy" at that time. SF's Daly moderates a panel at that event starting 1315ET, and also at the event at 1450ET, Atlanta's Bostic, Cleveland's Mester and Boston's Rosengren participate in a discussion. Bostic closes the event at 1515ET.

- In supply, Monday's 3-/10-Yr sales are followed up by $40B 42-day bill auction at 1130ET, and $24B 30Y Bond auction at 1300ET.

- No NY Fed operational purchases, but we get a schedule update at 1500ET - which could show an adjustment in the composition of purchases (as alluded to by SOMA head Logan last week).

EGB/GILT SUMMARY: Fresh Vaccine Woes Trigger Core EGB Buying

European sovereign bonds traded weaker this morning before news that the US is calling for a pause on the Johnson & Johnson vaccine due to clotting fears triggered a leg higher for core EGBs.

- Gilts now trade above yesterday's close with the curve a touch flatter.

- The bund curve has similarly bull flattened with the 2s30s spread 1bp narrower on the day.

- OAT yields are 1bp lower at the longer end.

- The UK economy returned to positive growth in February, despite the national lockdown. The industrial sector has fared particularly well with output beating expectations.

- Supply this morning came from the UK (Gilt , GBP1bn), Germany (Linker, EUR0.387bn allotted), Italy (BTPs, EUR7.75bn), Spain (Letras, EUR6.752bn), Belgium (TCs, EUR2.0bn), Finland (RFTBs, EUR2.0bn), the ESM (Bills, EUR.1bn). Syndications today include: Spain (15-year bond) Austria (dual tranche for 4-/50-year issues) and the Netherlands (0% Jan-38 DSL).

EUROPE OPTION FLOW SUMMARY

Eurozone:

RXM1 174.00 call bought for 11 in 5k. Hearing closing

UK:

0LM1 99.625/99.75/100.125/100.25 broken call condor sold at 9.25 in 5k (v 99.75)

EUROPE ISSUANCE UPDATE: Heavy Supply Day

UK DMO sells GBP1bln of the 1.625% Oct-71 Gilt, Avg yield 1.117% (Prev. 0.741%), Bid-to-cover 2.23x (Prev. 2.32x), Tail 0.8bp (Prev. 0.2bp)

Italy sells:

- E4.000bln 0% Apr-24 BTP, Avg yield -0.170%, Bid-to-cover 1.38x

- E1.750bln 1.60% Jun-26 BTP, Avg yield 0.120%, Bid-to-cover 1.55x

- E2.000bln 0.95% Mar-37 BTP, Avg yield 1.260%, Bid-to-cover 1.47x

Germany allots E0.387bln 0.10% Apr-33 ILB, Avg yield -1.57% (Prev. -1.51%), Bid-to-cover 0.65x (Prev. 1.08x), Buba cover 1.18x (Prev. 1.45x)

Syndications:

Dutch DDA update (0% Jan-38 DSL)

- Cut-off spread confirmed at 0% May-36 plus 17.0bps

- Books of E18bln

Spain long 15y launched (Jul-37 Obli)

- Size set at E6bln

- Spread set earlier at Jul-35 Obli plus 15bps

- Books over E42bln

Austria dual-tranche 4y/50y update

4-year spread set at MS-18bp with books over E27.5bln

50-year revised guidance MS+32bps with books over E14.8bln

FOREX: Markets Await CPI, Fedspeak

- Currencies largely trade inside recent ranges, with traders awaiting today's CPI release and a deluge of Fedspeak ahead of the media blackout period that comes this weekend. The USD is mixed, with some pre-NY hours weakness emerging to erase modest gains seen in Asia-Pac trade.

- Price action again favours GBP, although GBP/USD is yet to top the Monday high. NOK and CAD are again softer as middling oil prices do little prop up the oil-tied currency outlook.

- Front-end implied vols are inching lower, with GBP implieds seeing the most notable decreases. The 1m contract now trades below the early April lows to rival February's post-pandemic low.

- After a quiet Monday, the events calendar gets considerably busier Tuesday, starting with US CPI, which is forecast to have risen 0.5% in March. There are also a number of Fed speakers, with Harker, Daly, Barkin, Mester, Bostic and Rosengren all due.

FX OPTIONS: Expiries for Apr13 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1800-05(E504mln), $1.1885-1.1900(E643mln-EUR puts)

- USD/JPY: Y106.35($1bln), Y109.50($478mln)

- EUR/GBP: Gbp0.8560-70(E646mln-EUR puts)

- AUD/USD: $0.7595-0.7600(A$767mln-AUD puts), $0.7630(A$413mln-AUD puts)

- USD/CNY: Cny6.45($700mln), Cny6.60($730mln)

TECHS: Price Signal Summary - S&P E Minis Needle Still Points North

- In the equity space, S&P E-minis bulls are holding onto gains. The focus is 4160.13 next, 1.500 projection of the Feb 1 - Feb 16 - Mar 4 price swing.

- In the FX world, EURUSD maintains a short-term bullish tone. The focus is on 1.1938, the 50-day EMA and a key resistance area where a break is required to suggest scope for an extension higher. The GBPUSD outlook remains bearish with a firm resistance at 1.3919, Apr 6 high. The key support and bear trigger to watch is 1.3670, Mar 25 low. A brief test of this support yesterday failed to result in a clear break. EURGBP key near term resistance is 0.8731, Feb 26 high. A break of this hurdle is required to suggest scope for an extension of recent gains. USDJPY remains vulnerable near-term. The 20-day EMA has been probed. A clear break would open 108.41, Mar 23 low.

- On the commodity front:

- Gold is pulling away from recent highs. Resistance has been defined at $1758.8, Apr 8 high. Watch support at $1721.4, Apr 5 low.

- Brent (M1) key directional triggers are unchanged.

- Resistance is at $65.39, Mar 29 high with key support at $60.33, Mar 23 low and the bear trigger.

- WTI (K1) directional triggers are:

- Resistance at $62.27, Mar 30 high and support at $57.25, Mar 23 low and the bear trigger

- In the FI space, key support to watch in Bunds (M1) remains 170.52, Mar 18 low. The key resistance is at 172.66, Mar 25 high. The key support and bear trigger in Gilts (M1) is unchanged at 126.79, Mar 18 low. Initial firm resistance is at 128.93, Mar 25 high.

EQUITIES: Stocks Inch Higher, But Gains Inconsistent

- European stocks mixed early Tuesday, with mainland Eurozone indices higher (EStoxx50 +0.4%, DAX +0.3%) while the UK's FTSE-100 lags (down 0.1%).

- The e-mini S&P hit a new all time high yesterday at 4,124.50 and sits just 5 points below that mark at the European open.

- Earnings in focus this week. These are the highlights:

WEDS: Goldman Sachs, JPM, Wells Fargo

THURS: BofA, Blackrock, Citi, Charles Schwab

FRI: BNY Mellon, Morgan Stanley, State Street

COMMODITIES: Oil Parameters Unchanged For Now

- Both WTI and Brent crude futures sit in minor positive territory, although they're yet to top the Monday highs as the USD index puts out an unimpressive performance.

- A break above yesterday's $60.77 for WTI crude futures would open the April highs of $61.75 initially, but further catalysts may be needed to support the price in what's been an uninspiring session so far.

- Elsewhere, spot gold traded at a new weekly low of $1723.77 this morning as the retreat from the failed test of the 50-dma extends. That level crosses today at $1754.19 and remains a key hurdle for gold bulls going forward.

- Silver continues to oscillate either side of the upwardly-trending 200-dma at $25.15, with this week's early dip bought to keep the gravitational pull of the level intact ahead of US CPI.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.