Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS:

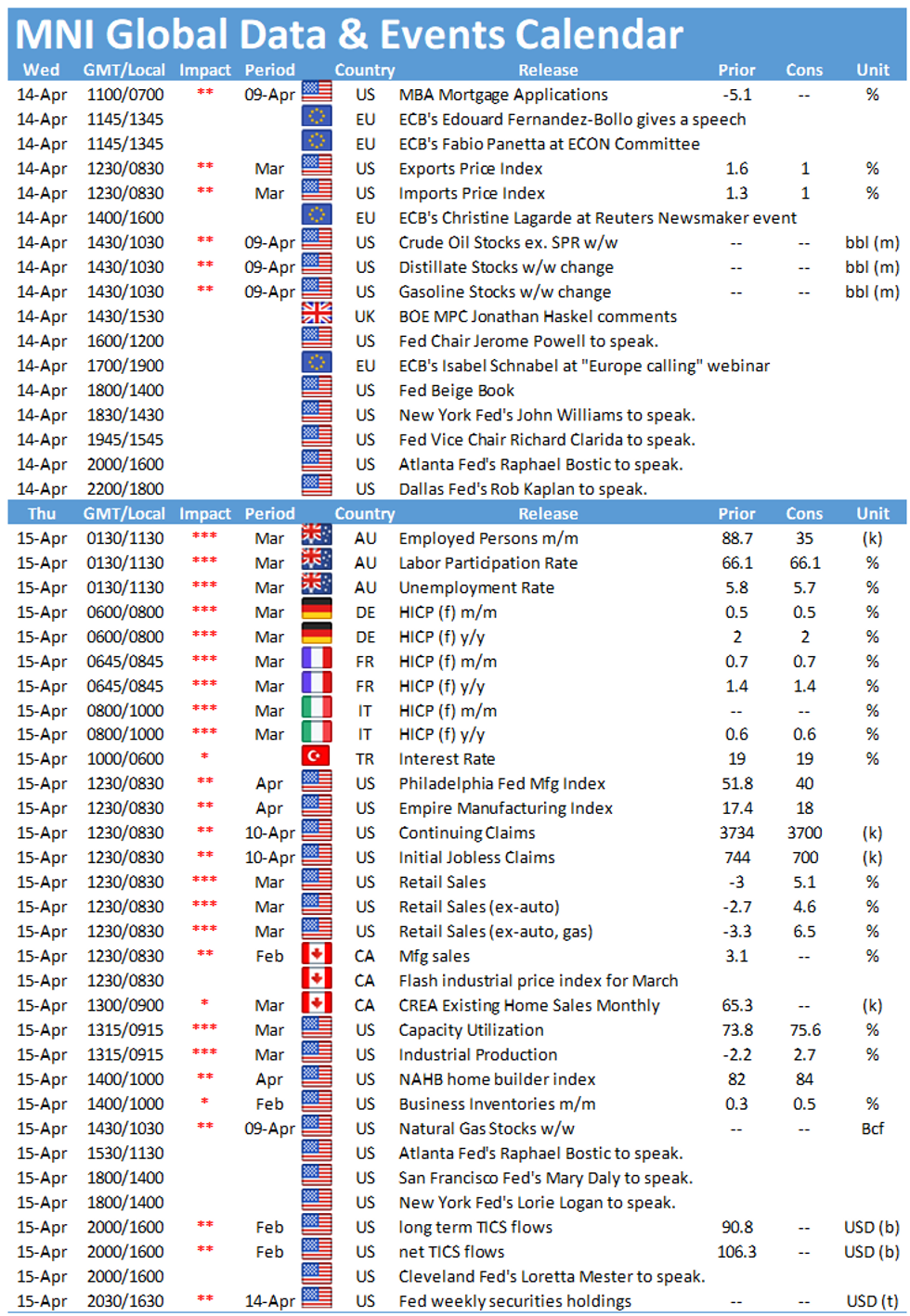

- Bank earnings in focus, JPM, Goldman Sachs, Wells Fargo all cross

- Busy speaker slate, with Lagarde, Powell, Clarida all due

- USD Index retreats to new April lows

US TSYS SUMMARY: Fed Speakers And Bank Earnings Eyed

Treasuries have pared gains after TY futures hit an April high in Asia-Pac trading, with the curve mildly steeper. Attention ahead is on Fed speakers and bank earnings (JPM, WF, GS before the bell).

- Jun 10-Yr futures (TY) down 3.5/32 at 131-31 (L: 131-28.5 / H: 132-06). 2-Yr yield is up 0.2bps at 0.161%, 5-Yr up 1.9bps at 0.8548%, 10-Yr up 1.8bps at 1.6323%, 30-Yr up 1.6bps at 2.3101%.

- A long Fed speaker list again: Dallas' Kaplan at 0915ET, Chair Powell at 1200ET (no text, but Q&A), NY's Williams at 1430ET (text not expected, but Q&A), VC Clarida at 1545ET (text and Q&A), and Atlanta's Bostic at 1600ET. Beige Book out at 1400ET as well.

- Powell, Williams and Clarida most in focus - would be interesting if they say anything about recent topics incl the Mar CPI report / possible 'tweak' in Tsy purchases / vaccination criteria for tapering.

- A light day for data (a respite between Tuesday's CPI and Thursday's Retail Sales / Ind Prod / jobless claims). March import/export prices at 0830ET. And supply ratchets down after a busy start to the week: just $35B of 119-day bills selling at 1130ET.

- NY Fed - which released its forward operational purchase schedule Tuesday afternoon (with no changes to purchase composition)- buys ~$12.825B of 0Y-2.25Y Tsys today.

EGB/GILT SUMMARY: Focus on Lagarde later

- EGBs and gilts have largely reversed early weakness with gilts largely unchanged and Bunds a little higher on the day.

- Peripheral spreads are generally a little tighter, with a few exceptions.

- Eurozone industrial production was a little better than expected while the final print of Spanish HICP was unchanged from the preliminary print.

- Issuance this morning has seen decent German 30y Bund and UK 30-year linker auctions while Slovakia is holding a 15-year syndication with books of E5.6bln as per the latest update.

- The most significant news has been the release of more details for the NextGenEU issuance plans. It has been confirmed that both auctions and syndications will take place with 6-monthly funding updates and with issuance due to start in the summer.

- Later today we will hear from Lagarde in a fireside chat at 15:00BST, Schnabel in a webinar at 18:00BST and the BOE's Haskel at 15:30.

- Gilt futures are up 0.06 today at 128.27 with 10y yields up 0.1bp at 0.778% and 2y yields up 0.2bp at 0.045%.

- Bund futures are up 0.15 today at 171.41 with 10y Bund yields down -0.7bp at -0.300% and Schatz yields down -0.2bp at -0.709%.

- BTP futures are up 0.27 today at 148.48 with 10y yields down -1.3bp at 0.735% and 2y yields up 0.2bp at -0.362%.

- OAT futures are up 0.21 today at 161.94 with 10y yields down -1.1bp at -0.46% and 2y yields down -0.7bp at -0.672%.

EUROPE ISSUANCE UPDATE

Germany allots E1.287bln 30-year 1.25% Aug-48 Bund, Avg yield 0.22% (Prev. 0.10%), Bid-to-cover 1.08x (Prev. 1.08x), Buba cover 1.26x (Prev. 1.31x)

UK DMO sells GBP600mln nominal of 0.125% Mar-51 linker, Avg yield -1.979% (Prev. -2.023%), Bid-to-cover 2.31x

Syndication:

Slovakia 15y update (Apr-36 SlovGB)

- Spread set at MS +9 bps

- Books now in excess of E5.6bln (DJ)

EUROPE OPTIONS FLOW SUMMARY

Eurozone:

3RZ1 100.00/99.875 put spread vs 100.50/100.625 call spread, buys the p/s for 1 in 4k on the day

UK:

0LZ1 99.875/100.00/100.125/100.25 1x1x0.5x0.5 call condor sold at 1 in 7k

2LZ1 99.25 put (v 99.33) sold at 3k in 15

FOREX: USD Softer Pre-Powell, Clarida Speeches

- The greenback trades lower across the board, with the USD index hitting new April lows this morning and eyeing the key support at the 91.578 50-dma. Antipodean currencies are the main beneficiaries, with AUD and NZD outperforming ahead of NY hours.

- The RBNZ rate decision overnight saw rates unchanged, but some sell-side outfits eyed less dovish language in the policy statement, as the bank no longer stressed the possibility of negative interest rates going forward. The subsequent NZD strength is erasing the late-March weakness, with NZD/USD nearing the 100-dma at 0.7148 which becomes the first target.

- Risk sentiment is positive, with the e-mini S&P holding just below the late Tuesday highs which marked a new record. Futures are universally positive in the US, with tech-led NASDAQ futures outperforming relative to both the S&P and Dow.

- Focus turns to central bank speak, with key missives due from both Fed's Powell and Clarida later today. The data schedule is lighter, with just US import/export price indices on the docket.

FX OPTIONS: Expiries for Apr14 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1795-00(E855mln), $1.1900(E1.1bln-EUR puts), $1.1925(E1.3bln-EUR puts), $1.1945-60(E1.46bln-EUR puts), $1.1975-80(E430mln-EUR puts)

- USD/JPY: Y108.00($831mln), Y108.50($525mln), Y108.75-80($477mln), Y108.95-00($868mln)

- GBP/USD: $1.3840-50(Gbp792mln-GBP puts), $1.4050(Gbp762mln)

- EUR/GBP: Gbp0.8600-15(E1.1bln)

- AUD/USD: $0.7700(A$700mln-AUD puts)

- USD/CAD: C$1.2465-70($750mln), C$1.2500($1.2bln-USD puts)

Price Signal Summary - BTPs Remain Heavy

- In the equity space, S&P E-minis bulls continue to dominate. The focus is on 4160.13 next, 1.500 projection of the Feb 1 - Feb 16 - Mar 4 price swing.

- In the FX world, the USD is weaker. EURUSD has cleared the 50-day EMA strengthening a short-term bullish argument. The focus is on 1.1990, Mar 11 high and a key resistance. The GBPUSD outlook remains bearish with a firm resistance at 1.3919, Apr 6 high. The key support and bear trigger to watch is 1.3670/69, Mar 25 and Apr 12 low. EURGBP key near term resistance is 0.8731, Feb 26 high. A break of this hurdle is required to suggest scope for an extension of recent gains. USDJPY remains vulnerable near-term. The 20-day EMA has been breached and attention is on 108.41, Mar 23 low.

- On the commodity front:

- Gold remains below recent highs. Resistance has been defined at $1758.8, Apr 8 high. Watch support at $1721.4, Apr 5 low.

- Brent (M1) is firmer this morning.

- Resistance to watch is at $65.39, Mar 29 high. Key support is unchanged at $60.33, Mar 23 low.

- WTI (K1) is edging higher too.

- Key resistance is at $62.27, Mar 30 high and support is unchanged at $57.25, Mar 23 low.

- In the FI space, key support to watch in Bunds (M1) remains 170.52, Mar 18 low. The key resistance is at 172.66, Mar 25 high. Initial resistance is at 172.12, Apr 8 high. The key support and bear trigger in Gilts (M1) is unchanged at 126.79, Mar 18 low. Initial firm resistance is 128.93, Mar 25 high. BTPs (M1) cleared support yesterday at 148.36, Mar 18 low. This opens 147.68 next, 76.4% retracement of the Feb 26 - Mar 11 rally.

EQUITIES: Stocks Hold Lofty Heights Pre-Earnings

- US index futures trade mixed early Wednesday, in a holding pattern as they sit just below this week's all time highs. Earnings a focus today, with reports due from JPMorgan, Goldman Sachs and Wells Fargo from 1200BST/0600ET onwards. Full schedule for this week here: https://roar-assets-auto.rbl.ms/documents/9444/MNI...

- Across Europe, stock performance has been similarly inconsistent, with France's CAC-40 outperforming while Germany's DAX and UK's FTSE-100 put in less impressive performances.

- Early Wednesday trade has European tech trading well, while utilities and industrials are at the bottom-end of the pile.

COMMODITIES: WTI, Brent Crude Futures Supported on Geopolitical Tensions, Weaker Greenback

- Commodity markets are seeing decent support from the weaker dollar so far Wednesday, a move which sees USD Index retreat to its lowest levels of the month and near the first key support at the 91.580 50-dma.

- As a result, WTI and Brent crude futures are higher by near 2% apiece, with further support coming from the ratcheting higher of geopolitical tensions as Russia formally launch military drills in the Black Sea ahead of the arrival of US ships in the region. Today's oil strength has put WTI and Brent crude futures on the best footing since early April, with $62.27 the next hurdle for WTI.

- Weekly DoE crude oil inventories data is next up. Markets expect a draw of 2.5mln bbls this week.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.