Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS:

- Initial US curve flattening reverses, short-end outperforms

- Stocks stronger, but bounce is shallow

- Markets geared for more central bank speak

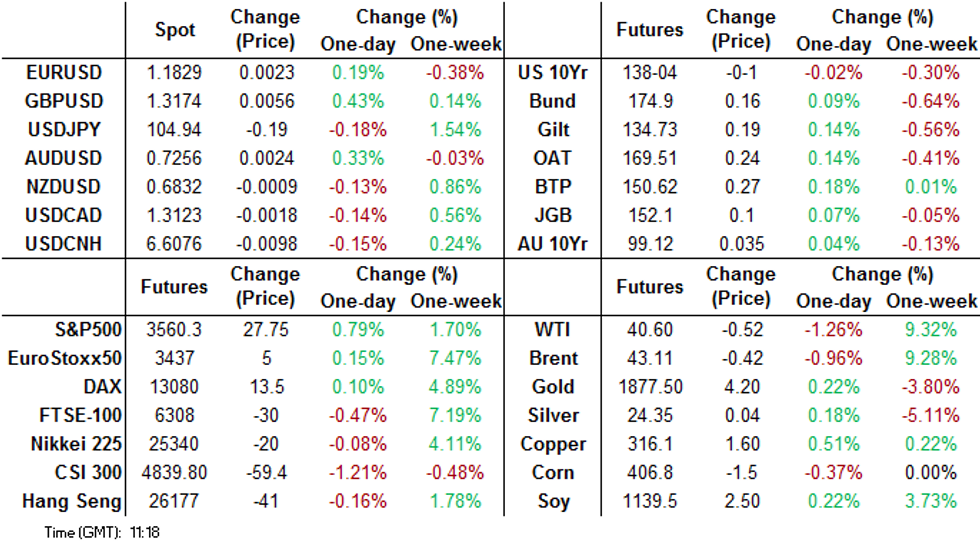

US TSYS SUMMARY: Overnight Flattening Reverses

Treasuries weakened in European trading following a modest uptick in Asia-Pac hours, alongside equities steadily gaining ground and the dollar weakening. Michigan sentiment data and Fed speakers feature on Friday's schedule.

- Overall, largely net unchanged on the day: Dec 10-Yr futures (TY) steady at 138-5 (L: 138-02.5 / H: 138-10.5), with volumes slightly on the stronger side (>330k).

- Early flattening has reversed, with the short end now outperforming. The 2-Yr yield is down 0.4bps at 0.173%, 5-Yr is up 0.5bps at 0.3966%, 10-Yr is up 0.5bps at 0.8865%, and 30-Yr is up 0.4bps at 1.6422%.

- Not really any themes dominating; Thursday's rotation into pandemic (out of post-vaccine) plays doesn't seem to be occurring again today, note Nasdaq and S&P futs performing roughly equally (+0.7% apiece).

- The calendar opens at 0700ET with NY Fed's Williams in a webinar; we get St Louis' Bullard at 0830ET.

- In data, Oct PPI at 0830ET, with Nov Michigan sentiment at 1000ET.

- NY Fed buys ~$8.825B of 2.25-4.5Y Tsys.

EGB/GILT SUMMARY: European Sovereigns Firmer Amid Mixed Equities

European sovereign bonds have traded firmer alongside mixed trading in equities.

- Gilts have strengthened with cash yields within 1bp of yesterday's close.

- Bunds are similarly firmer with the curve close to flat.

- OATs have marginally outperformed with cash yields 1-2bp lower.

- Preliminary Q3 GDP data for the eurozone was marginally weaker than expected (12.6% Q/Q vs 12.7% consensus). The final October CPI prints for France and Spain were marginally better than the initial estimates.

- ECB policymaker comments hit the wires this morning with Isabel Schnabel indicating that the intensify of asset purchases will be discussed, while Pablo Hernandez de Cos warned that the risks to the eurozone are tilted to the downside.

- Following an outbreak of bitter infighting in Downing St, which triggered the resignation of the Director Communications, there is speculation in the media that PM Boris Johnson's close advisor Dominic Cummings could be planning to leave by year-end.

BTP: Futura update

Issuance for the retail-only 8-year BTP Futura now stands a bit over EUR5.4bln.

- We have seen roughly EUR2.5bln demanded on Monday, EUR1.5bln Tuesday, EUR1.0bln Wednesday, just under E0.5bln Thursday and today there have been another EUR50mln or so orders so far.

- Just a reminder that the first BTP Futura (a 10-year issue) saw demand total EUR6.1bln in July. So the second BTP Futura will probably end up being a little smaller in size.

OPTIONS FLOW RECAP

Eurozone:

ERU1 100.50/100.62/100.75c fly 1x3x2, bought for 1.25 in 2k

ERM1 100.625/ERU1 100.75 c calendar sold at 0.5 in 3k

ERU2 100.50^, bought for 26 in 2.5k

0RU1 100.37/20/12p ladder, bought for 0.25 in 7.5k

Eurozone Bank Stock Index:

SX7E Dec 62.5p/75c combo, bought the put for 0.25 in 6k

UK:

LZ1 100c vs LM1 100c, sold the Dec at 4.75 in 6k total

LM1 100.00/12/25/37c condor, bought for 2.5 in 4k

FOREX: Sterling Staging Tepid Bounce So Far

Comments from the Italian finance ministry drew some attention in early European hours, after the Director General signalled that it's currently 15-20bps cheaper to fund in USD vs. EUR, which helped buoy EUR/USD through yesterday's highs of 1.1823 (effectively pointing out how undervalued the euro is versus the dollar on this basis).

- There's been plenty more EUR-centric commentary, with ECB's Schnabel indicating that December's 'recalibration' of policy will likely include a discussion surrounding "the intensity of asset purchases". EUR is outperforming slightly, rising against most others in G10.

- After several sessions of underperformance, GBP is bouncing in early trade off the weekly low printed late yesterday at 1.3106. Markets may be taking the view that the departure of key Johnson aide Cummings could smooth the path to a free trade deal in the ongoing Brexit negotiations.

- US PPI and Uni. of Michigan releases are the data highlights Friday. Speaker slate includes ECB's Rehn, Fed's Williams & Bullard and BoE's Tenreyro, Cunliffe & Bailey.

FX option highlights for today's NY cut (1000ET-1500GMT/Source DTCC)

- Mixed EUR/USD interest between $1.1795/1.1800 for E1.4bln, with the area between $1.1840-55 holding E1.8bln of mixed interest. (current level $1.1804)

- EUR/GBP has E807mln of mixed interest rolling off between Gbp0.9045-50.(current level Gbp0.8996)

- AUD/USD has mainly AUD calls rolling off from $0.7300(A$599mln), $0.7325-35(A$710mln), $0.7400(A$568mln). (current level $0.7231).

- USD/CAD has $900mln of C$1.3125 mixed interest, $620mln of USD calls. (current level C$1.3161)

Option expiries for Nov13 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1600(E703mln), $1.1735-40(E935mln),

$1.1770-75(E522mln), $1.1795-00(E1.4bln), $1.1840-55(E1.8bln), $1.1870-75(E952mln), $1.1900(E512mln),

$1.2000(E1.78bln-EUR calls) - USD/JPY: Y101.00($995mln-USD puts), Y104.65-75($502mln), Y105.50($560mln)

- EUR/GBP: Gbp0.8950(E586mln), Gbp0.9045-50(E807mln)

- AUD/USD: $0.7300(A$599mln-AUD calls), $0.7325-35(A$763mln), $0.7400(A$568mln-AUD calls)

- USD/CAD: C$1.3125($900mln)

- USD/CNY: Cny6.51($500mln), Cny6.60($1.1bln), Cny6.75($600mln)

EQUITIES: Stocks Off Lows, But Bounce is Shallow

Equities across continental Europe and futures in the US are stronger, but the bounce leaves little to be desired when compared to Monday's initial sharp rally.

Peripheral European markets outperform, with Italian and Spanish indices higher by 0.6-1.2%, while UK's FTSE-100 lags on GBP strength.

Tech firms are outperforming in Europe in a further reversal of the reflation trades that made up much of the activity on Monday. Financials and utilities aren't far behind.

The e-mini S&P recovery touched 3569.00 this morning before fading slightly - resistance is seen firmer headed into 3576.75, the late Nov 11 highs.

COMMODITIES: Oil Continues To Slide

Oil continues to fade after Thursday's surprise build of DoE inventories, but WTI still above $40.00/bbl (support at $39.41).

- WTI Crude down $0.35 or -0.85% at $40.69

- Natural Gas up $0 or +1.02% at $2.973

- Gold spot up $2.08 or +0.11% at $1878.9

- Copper up $1.7 or +0.54% at $315.5

- Silver up $0.03 or +0.14% at $24.2732

- Platinum up $8.6 or +0.97% at $888.83

GOLD TECHS: Hovering Above Key Support

- RES 4: $1992.5 - High Sep 1

- RES 3: $1973.6 - High Sep 16

- RES 2: $1965.6 - High Nov 9 and the bull trigger

- RES 1: $1901.3 - 50-day EMA

- PRICE: $1879.2 @ 06:55 GMT Nov 13

- SUP 1: $1850.5 - Low Nov 9

- SUP 2: $1848.8 - Low Sep 28 and the bear trigger

- SUP 3: $1837.1 - 38.2% retracement of the Mar - Aug rally

- SUP 4: $1818.0 - High Jul 8

Gold is consolidating and still appears vulnerable following the Nov 9 sharp sell-off. While the move lower this week is bearish, we note that the yellow metal has yet to clear a key near-term support at $1848.80, Sep 28 low and a bear trigger. A breach of this support is required to confirm bearish conditions and open $1837.1, the 38.2% retracement of the Mar - Aug rally. A stronger intraday recovery would expose $1965.6, Nov 9 high.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.