Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

Highlights:

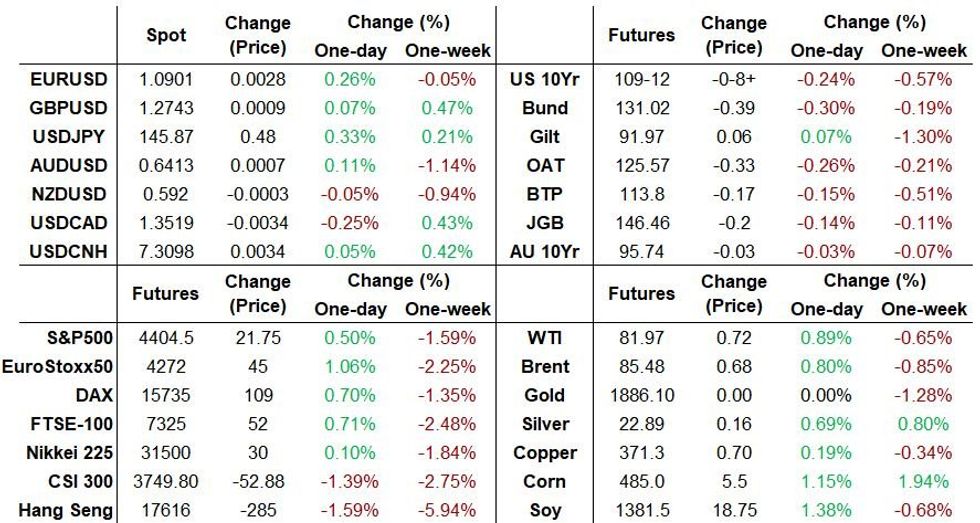

- An initial risk-off move overnight - after China cut key lending rates by less-than-expected - has faded.

- CNH reversed earlier losses against USD, equity futures have bounced, and Tsys have bear steepened.

- The week's focus is on August flash PMIs Wednesday and Jackson Hole into the weekend.

US TSYS: Bear Steeper After China Policy Action, Flow

- Cash Tsys have bear steepened, having come under pressure along with core FI more generally in Asian trade after China held the 5-Year LPR steady at 4.20% (vs 15bp cut expected), with 1-Year LPR cut 10bp (vs 15bp cut expected).

- An initial paring of losses has since been reversed with major benchmarks pushing lower again, aided by recent futures flow including a 7.9k block FV sale, and with further flow/headlines likely driving the upcoming session amidst a very light docket.

- 2YY +3.0bp at 4.973%, 5YY +3.8bp at 4.423%, 10YY +4.8bp at 4.302%, and 30YY +6.0bp at 4.435%. The steepening pushes 2s10s back to -67bps to move closer to Thursday’s -64bps for highs since May.

- TYU3 trades 10 ticks lower at 109-10+ off session lows of 109-09 as the bear cycle remains in play, albeit under lower than recent average volumes with 260k after last week’s more elevated activity. Support is seen at 109-03+ (Aug 17 low) after which lies 109-00 before a major support at 108-26+ (Oct 21, 2022 low).

- Bill issuance: US Tsy $69B 13W, $62B 26W bill auctions (1130ET)

STIR: Fed Cut Expectations At Low End Of Recent Ranges

- Fed Funds implied rates have firmed marginally since Friday’s close, with a still familiar +2.5bp for Sep (unch) and cumulative +9.5bp for Nov (+0.5bp) to a terminal 5.43%.

- Sightly larger increases in 2024 implied rates sees cut expectations remain at the low end of recent ranges with 47bp from terminal to Jun’24 and 113bp from terminal to Dec’24.

- A quiet docket to start the week sees attention on external factors including China policymaking (1y LPR cut 10bp & 5Y LPR steady vs 15bp cut expected for both) today before domestic data and especially Jackson Hole later this week comes into focus.

CHINA: Liquidity Squeeze Bolsters Yuan, USD/CNH Approaches Session Lows

Spot USD/CNH has unwound its earlier gains after hitting resistance around the 7.3360 mark, with the overnight session headlined by the surprisingly conservative Loan Prime Rate (LPR) fixing. The pair is now back to virtually unchanged levels, last sitting at 7.3062.

- The market was caught off guard as the PBOC kept the 5-Year LPR unchanged at 4.20% (versus 4.05% expected) and trimmed the 1-Year LPR by 10bp to 3.45% (versus 3.40% expected). 5-Year LPR is the benchmark rate for most mortgages in China, while 1-year LPR is used as a reference for most household and corporate loans. The failure to meet market expectations comes after signals anticipating more forceful stimulus for the flagging economy, including last Friday's meeting in which the PBOC asked local lenders to boost loans.

- Another stronger than expected USD/CNY mid-point fixing (880-pip bias versus BBG estimate) did little to shield the redback during local hours, with the conservative LPR fixing sowing confusion. The PBOC effectively signalled reluctance to support credit markets despite the ongoing turmoil.

- Offshore yuan has recouped most overnight losses amid a liquidity squeeze, with forward points rallying into the European morning. Bloomberg cited trader sources as attributing this to "a combination of less CNH supply from big Chinese names in offshore yuan swap market since last week, and liquidity demand derived from PBOC's bill sales tomorrow." They also pointed to "borrowing demand from some market players (...) after 3pm local time (...) aside from dollar sales by the overseas branches of Chinese banks."

- CNH 3-month forward points have surged to best levels since February; 12-month forward points are at best levels since May.

FOREX: USDJPY Edges Higher Following Corrective Pullback

- Currency markets have had a subdued session on Monday with the USD index holding a very narrow 20 pip range, sliding into moderate negative territory as we approach the NY crossover.

- The Japanese Yen remains on the back foot with USDJPY trading at fresh session highs of 145.73 in recent trade, edging further away from the 144.93 pullback lows on Friday. The overall technical uptrend in USDJPY remains intact and short-term pullbacks are considered corrective. Moving average studies are in a bull mode condition, highlighting current positive sentiment. The focus is on 147.49, a Fibonacci projection.

- USDCNH reached as high as 7.3361 overnight as concerns surrounding the Chinese economy continue to dampen sentiment. Reactions were exacerbated by no change in the 5-yr LPR rate, which kept onshore equities on the back foot on Monday with consensus looking for a 15bps cut to boost the under pressure growth backdrop.

- However, in recent trade the Yuan has been bolstered by source reports that major state-owned banks were seen mopping up offshore yuan liquidity on Monday and a large squeeze in front end CNH forward points. In similar vein, the likes of the Euro and AUD have recovered off the lows and are now trading in positive territory.

- The Fed's Jackson Hole conference is the week's key event, with announced speakers so far including Chair Powell and ECB Pres Lagarde on Friday. Key data will be Wednesday’s European flash PMIs.

EUROPE ISSUANCE UPDATE:

Belgium OLO auction results:

- E1.225bln of 0.10% Jun-30 OLO, Avg Yield 3.034% (1.73x bid-to-cover)

- E1.575bln of 3.00% Jun-33 OLO, Avg Yield 3.273% (1.72x bid-to-cover)

FX OPTION EXPIRY

Of note:

EURUSD 4.36bn at 1.0835/1.0900.

USDJPY 1.56bn at 145.00 (wed).

USDJPY 1.56bn at 145.00 and 1.79bn at 146.00 (thu).

USDCNY: 3.44bn at 7.30 (thu).

- EURUSD: 1.0835 (258mln), 1.0840 (538mln), 1.0845 (688mln), 1.0850 (310mln), 1.0855 (430mln), 1.0885 (409mln), 1.0900 (1.73bn), 1.0910 (327mln), 1.0925 (662mln).

- USDJPY: 145.00 (421mln), 145.50 (460mln).

- USDCAD: 1.3510 (478mln).

- AUDUSD: 0.6400 (292mln), 0.6440 (300mln), 0.6450 (218mln).

- USDCNY; 7.30 (386mln).

EQUITIES: Bearish Theme in E-Mini S&P Remains Present

A bearish theme in Eurostoxx 50 futures remains present and last week’s sell-off reinforces current conditions. The contract last week breached support at 4276.00, the Aug 8 and 15 low and Friday’s move lower resulted in a break of 4220.00, the Jul 7 low. This opens 4177.40, a Fibonacci retracement. Key short-term resistance is unchanged at 4420.00, the Aug 10 high. Initial firm resistance is 4348.20, the 50-day EMA. A bearish theme in the E-mini S&P contract remains intact and Friday’s sell-off reinforces this theme. Last week’s extension lower resulted in a break of the 50-day EMA and the contract breached channel support drawn from the Mar 13 low. 4368.50, the Jun 26 low, was breached Friday and attention turns to 4344.28, a Fibonacci retracement. Initial firm resistance to watch is at the 50-day EMA - at 4455.92.

COMMODITIES: WTI Trend Needle Points North

- Gold is trading at its recent lows and the outlook remains bearish. Price has breached key support at $1893.1, the Jun 29 low. The clear break strengthens bearish conditions and signals scope for $1865.8, 76.4% of the Feb 28 - May 4 bull leg. Moving average studies remain in bear mode condition, highlighting current bearish sentiment. On the upside, initial firm resistance to watch is $1935.7, the 50-day EMA. First resistance is at $1920.7, the 20-day EMA.

- In the oil space, the uptrend in WTI futures remains intact and the recent pullback appears to be a correction. Firm support to watch lies at $78.33, the Aug 3 low. A clear break of this level would signal scope for a deeper short-term retracement. For bulls, a resumption of gains would refocus attention on the next objective at $85.24, the 1.236 projection of the Jun 28 - Jul 13 - Jul 17 price swing. Moving average studies are in bull-mode condition, highlighting an uptrend.

| Date | GMT/Local | Impact | Flag | Country | Event |

| 21/08/2023 | 1530/1130 | * |  | US | US Treasury Auction Result for 13 Week Bill |

| 21/08/2023 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 22/08/2023 | 0600/0700 | *** |  | UK | Public Sector Finances |

| 22/08/2023 | 0600/0800 | ** |  | NO | Norway GDP |

| 22/08/2023 | 0800/1000 | ** |  | EU | EZ Current Account |

| 22/08/2023 | 0900/1000 | * | | UK | Index Linked Gilt Outright Auction Result |

| 22/08/2023 | 1000/1100 | ** | | UK | CBI Industrial Trends |

| 22/08/2023 | - | * |  | FR | Retail Sales |

| 22/08/2023 | 1230/0830 | ** | | US | Philadelphia Fed Nonmanufacturing Index |

| 22/08/2023 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 22/08/2023 | 1400/1000 | *** | | US | NAR existing home sales |

| 22/08/2023 | 1400/1000 | ** | | US | Richmond Fed Survey |

| 22/08/2023 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 22/08/2023 | 1830/1430 | | US | Chicago Fed's Austan Goolsbee | |

| 23/08/2023 | 2300/0900 | *** |  | AU | Judo Bank Flash Australia PMI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.