Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS:

- USD weaker, USD Index slips through 100-dma

- Equities open gap with all time highs, US stocks poised for lower open

- Data, Speaker slate light, keeping focus on ECB, BoC decisions

US TSYS SUMMARY: Bonds Bounce as Global Equities Falter

Tsys trading marginally mixed, drop in equities to recent overnight lows (ESM1 -18.0) a tailwind for 30Y bonds as they climb off lows over last hour. SPUs following weaker global stocks: Estoxx as the index fell blow Friday's lows, Japan's NIKKEI settled down a whopping 584.99 pts or -1.97% at 29100.38.- USD bouncing off lows, VIX vol index on highs +1.30 around 18.60.

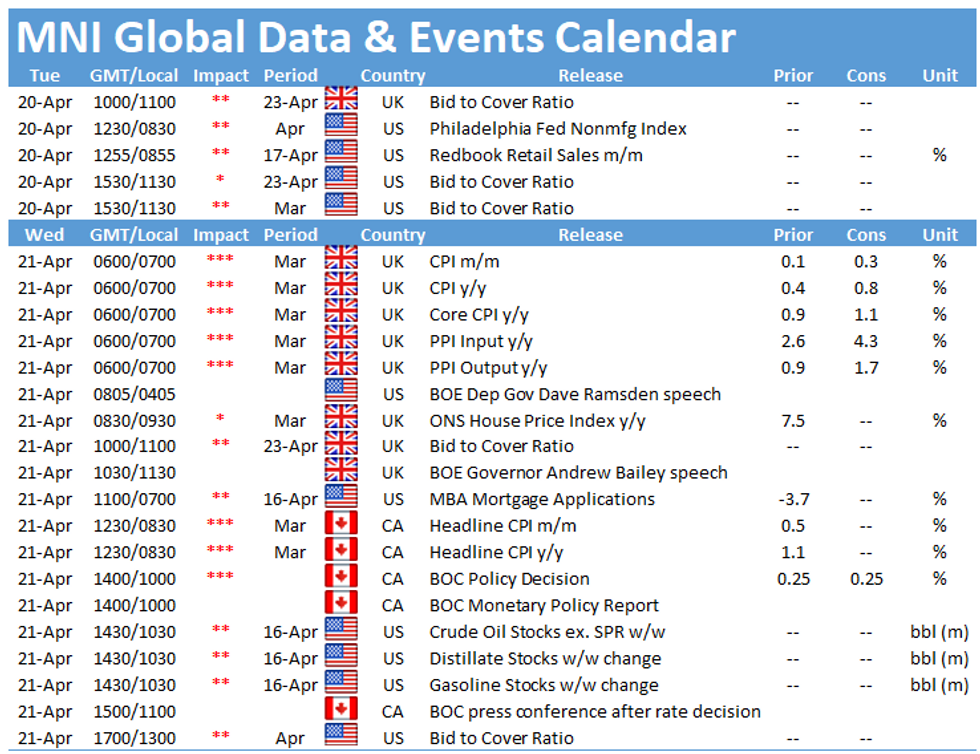

- Moderate volumes (TYM1 near 350k) on another day without significant US data or Fed speakers, the latter in media blackout until April 29. Focus turns to Bank of Canada and ECB monetary policy rate announcements on Wednesday and Thursday respectively.

- Incoming corporate issuance remains strong, banks still helping drive hedging volumes there.

- US Tsy supply: $40B 42D and $34B 52W bill auctions; NY Fed buy-operation: Tsy 20Y-30Y, appr $1.750B.

- The 2-Yr yield is unchanged at 0.1572%, 5-Yr is down 0.2bps at 0.8276%, 10-Yr is down 0.7bps at 1.5977%, and 30-Yr is down 0.6bps at 2.2902%.

EGB/GILT SUMMARY: Mixed Start

Core European sovereign bonds started the session on a weak footing following yesterday's sell-off, but have firmed through the morning alongside fresh downside for equities.

- Gilt yields are broadly 1bp lower in the belly and long-end of the curve with the 2s30s spread 1bp narrower.

- The bund curve has similarly flattened with the 2s30s spread inching down 1bp

- BTPs have continued to trade weaker with cash yields up to 1bp higher on the day and curve trading close to flat overall.

- This morning's UK labour market data was a touch better than expected with the official unemployment rate below consensus (4.9% vs 5.0% survey), while the 3m/3m employment change stood at -73k vs -145k expected.

- Supply this morning came from the UK (Gilts, GBP3.25bn), Germany (Schatz, EUR8.02bn allotted), Spain (Letras, EUR1.96bn) and the ESM (Bills, EUR1.5bn).

EUROPE ISSUANCE UPDATE:

UK DMO sells GBP3.25bln of 0.125% Jan-24 Gilt, Bid-to-cover 2.70x (Prev. 2.45x), Tail 0.2bps (Prev. 0.2bps)

Germany allots E4.085bln 0% Mar-23 Schatz, Avg yield -0.69% (Prev. -0.70%), Bid-to-cover 1.09x (Prev. 1.27x), Buba cover 1.33x (Prev. 1.61x)

Finland sells E0.986bln 0.25% Sep-40 RFGB, Avg yield 0.386%, Bid-to-cover 1.92x

Syndication: EU EFSM E4.75bln 15y syndication update (Apr-36), books in excess of E30bln, spread set at MS -7bps

Italian BTP Futura, books now exceed E3bln

EUROPE OPTIONS FLOW SUMMARY

Eurozone:

RXM1 168.50/168.00ps vs 172.50c, bought the ps, net received 9.5 ticks in 10k (-23 del)

RXM1 169/168ps, bought for 20 in 4k

RXM1 172/173cs bought for 14 in 1.5k

0RU1 100.37/100.25/100.12p ladder, bought for 0.25 in 2.5k

0RZ1 vs 0RM1 100.62c calendar, bought for 1.75 in 2.25k

FOREX: USD Index Slips Below 100-DMA Support

- The greenback remains weak, extending the recent downtrend to hit new multi-month lows early Tuesday. The USD index now trades below the 100-dma after the level held as decent support earlier in the week, keeping the USD among the weakest in G10 in early trade.

- JPY also trades poorly, with the JPY the weakest so far despite further weakness in global equity markets. The E-mini S&P has edged lower in early European trade, with futures testing yesterday's lows at pixel time.

- Commodity-tied currencies generally held up well in the Asia-Pac / European crossover, but have come under some selling pressure ahead of NY hours as commodity markets roll off their European morning highs.

- There are no tier 1 data releases Tuesday and the central bank speaker slate is similarly quiet. ECB's de Cos is the highlight, speaking at 1350BST/0850ET.

FX OPTIONS: Expiries for Apr20 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1885-00(E760mln), $1.1925-40(E1.7bln-EUR puts), $1.2000-05(E725mln), $1.2130-40(E661mln-EUR puts)

- USD/JPY: Y108.65($540mln-USD puts), Y109.95-00($515mln)

- GBP/USD: $1.3650(Gbp570mln)

- EUR/NOK: Nok10.00-10.01(E535mln-EUR puts)

- AUD/USD: $0.7765-95(A$1.2bln-AUD puts)

- USD/CNY: Cny6.40($520mln), Cny6.60($580mln)

Price Signal Summary - USD Remains Weak

- In the equity space, sentiment remains bullish. S&P E-minis are consolidating just below recent lows. The focus is on 4195.50 next, 1.618 projection of the Feb 1 - Feb 16 - Mar 4 price swing.

- In the FX world, EURUSD has rallied again today and bullish conditions remain intact following yesterday's break of 1.1990, Mar 11 high. This opens 1.2116 next, 76.4% of the Feb 25 - Mar 31 sell-off. GBPUSD rallied yesterday and cleared 1.3919, Apr 6 high. A break of 1.4017, Mar 4 high would likely trigger stronger gains and open 1.4103, 76.4%of the Feb 24 - Apr 12 downleg. EURGBP has found resistance at 0.8719, Friday's high. The support to watch is 0.8582, Apr 7 low. USDJPY has traded through 108.41, Mar 23 low and is still pressuring the 50-day EMA. A break of the average would open 107.57, trendline support drawn off the Jan 6 low

- On the commodity front, Gold maintains a bullish tone despite the pullback from yesterday's high. The focus is on $1805.7, Feb 25 high. Brent (M1) remains firm. Scope if for a climb towards $69.50, Mar 15 high. WTI (K1) is firmer too with potential for gains towards $64.88, Mar 18 high.

- In the FI space, Bunds (M1) yesterday cleared support at 170.52, Mar 18 low. This strengthens a bearish case and opens 170.05 next, 76.4% of the Feb 25 - Mar 25 rally. Support to watch in Gilts (M1) remains 127.81, Apr 14 low. Initial firm resistance is 128.93, Mar 25 high.

EQUITIES: Stocks Suffer, Gap Opens With Last Week's Highs

- US equity futures are uniformly lower, with all three major index futures indicating a lower open on Tuesday. The e-mini S&P has now opened a gap of around 45 points with the all time highs printed late last week.

- Weakness off the all time highs continues to work in favour of the VIX, which traded in the green yesterday and will likely do so at the Tuesday open as per futures markets.

- Across Europe, continental indices are similarly weak, with Spain's IBEX-35 and France's CAC-40 suffering. Europe's financials sector is the poorest performer, closely followed by both consumer discretionary and consumer staples names.

COMMODITIES: Oil Buoyed by Softer USD, Simmering Geopolitical Tension

- Both WTI and Brent crude futures trade higher, with gains of 1% apiece as USD weakness and a recovery through yesterday's highs helps to buoy prices. Tensions between the US and Russia remain a market focus, with Russia looking to restrict shipping and naval activity in the Black Sea, raising the spectre of a renewed wave of sanctions from the US.

- Tech targets for WTI sit at March 18th's $64.88 and the former trendline support drawn off Nov 2, 2020 low at $65.23.

- API inventories numbers due after-market should set the supply tone for the week, followed by tomorrow's DoE update.

- Both gold and silver are largely non-directional, with gold bouncing slightly after dipping through the Monday lows, while silver prices trades largely within the week's range.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.