Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS:

- USD Index at new multi-month high, nearing 200-dma

- Equities, oil bounce off week's low

- US durable goods, Fedspeak take focus

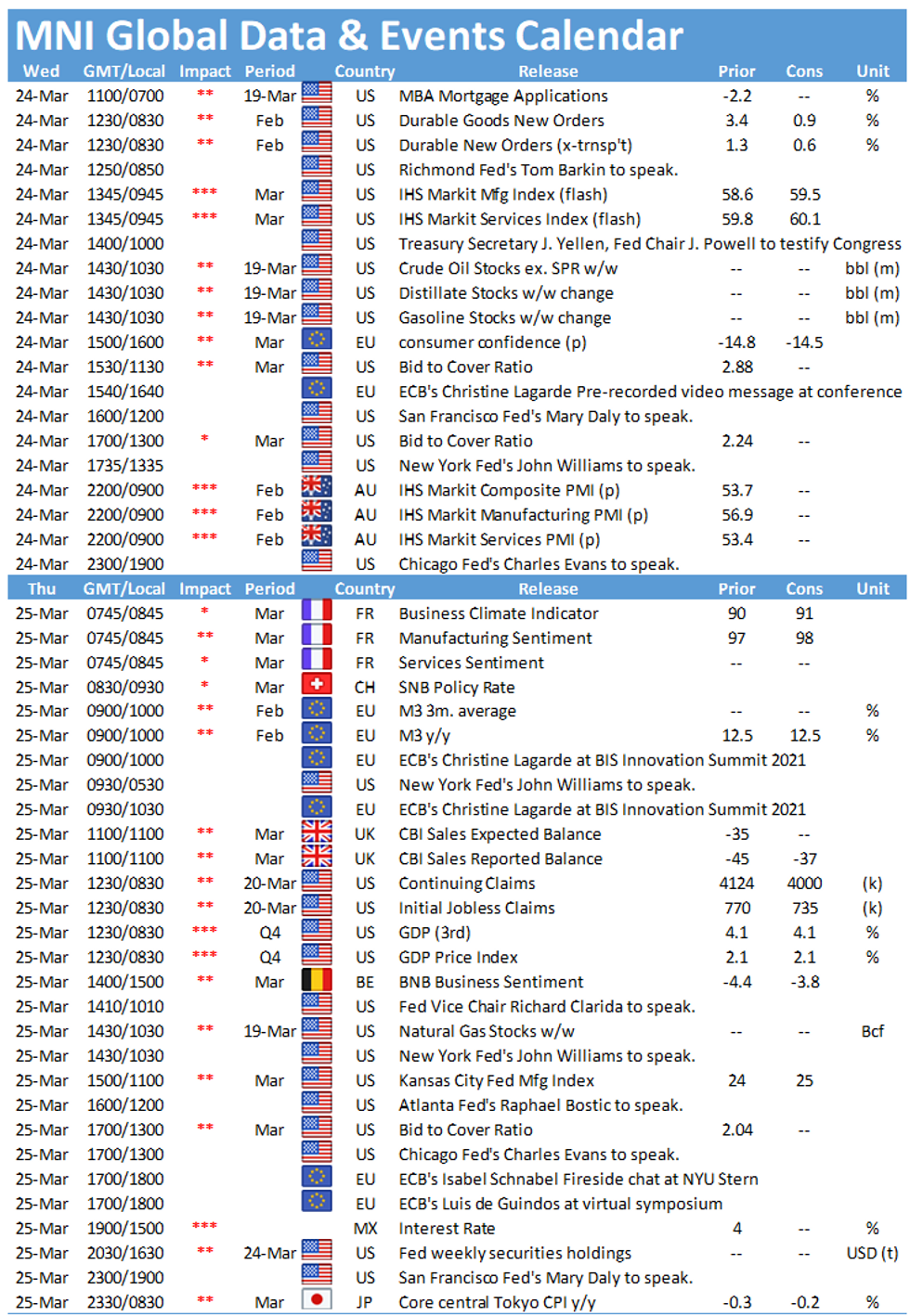

US TSYS SUMMARY: Off Highs Ahead Of Data, Supply, Speakers

A bit of a breather for Treasuries in early European trade, as strong European PMI data helped take the steam out of the global core FI rally. A busy US calendar awaits, with Fed speakers, data, and supply (2Y FRN and 5Y Note).

- The 2-Yr yield is up 0.5bps at 0.1504%, 5-Yr is up 0.3bps at 0.819%, 10-Yr is up 0.4bps at 1.6242%, and 30-Yr is down 0.4bps at 2.3226%.

- Jun 10-Yr futures (TY) up 2.5/32 at 132-0 0 (L: 131-31/ H: 132-09) Notably, TYs today touched the Mar 17 (FOMC decision) high of 132-09 before retreating.

- Fed's Powell and Tsy's Yellen go for round two of testimony in Congress, today before the Senate Banking committee starting at 1000ET. The other Fed speakers: Richmond's Barkin at 0850ET, NY's Williams at 1335ET, SF's Daly at 1500ET, and Chicago's Evans at 1900ET.

- Atlanta Fed Pres Bostic told the WSJ in an interview published this morning that he was one of 7 FOMC members who saw rate hike liftoff in 2023 in the March SEP 'dot plot'.

- In data, at 0830ET we get durable goods numbers, with March flash PMIs at 0945ET.

- In supply, $26B 2Y FRN sale at 1130ET (alongside $35B 119-day bills), with $61B 5Y Note at 1300ET. NY Fed buys ~$8.825B of 2.25-4.5Y Tsys.

EGB/GILT SUMMARY: EGBs Firmer as Risk-Off Lingers

European sovereign bonds continue to trade firm this morning as the risk-off theme lingers. Equities are generally soft, while the dollar continues to grind out against most of the G10.

- Gilts opened stronger but quickly gave back early gains, albeit with much of the curve still trading above yesterday's closing levels.

- Bund yields are broadly 1-2bp lower on the day with the curve 2bp flatter.

- OAT yields have similarly inched down 1-2bp across the middle/long end of the curve.

- BTPs trade in line with core EGBs. The 2s30s spread is 1bp narrower on the day.

- This morning's European flash PMI prints for March were better than expected and continue to show a sharp divergence between the manufacturing and service sectors. With Covid-related social restrictions being tightened in recent days, this morning's strong PMI reads will prove fleeting.

- Supply this morning came from the UK (Linker GBP350mn), and Germany (Bund, EUR3.2811bn allotted).

EUROPE ISSUANCE: UK, German Auctions

UK DMO sells GBP350mln of 0.125% Nov-56 linker, Avg yield -1.972% (Prev. -2.012%), Bid-to-cover 2.17x (Prev. 2.26x)

Buba allots E3.2811bln of the 0% Feb-31 Bund, Avg yield -0.36% (Prev. -0.32%), Bid-to-cover 1.21x (Prev. 1.28x)

EUROPE OPTIONS SUMMARY

Eurozone:

RXK1 169p, bought for 9.5 in 2kRXK1 167p, bought 2.5 in 6k

RXK1 174/175/176c fly, bought for 7.5 in 2k

RXM1 175c, sold at 25 in 4k

ERZ2 100p, bought for 3.5 in 4k

3RZ1 100/99.87ps vs 100.50/100.62cs, bought the ps for flat in 3k (ref 100.265)

3RZ1 99.87p, bought for 4 in 2.5k

UK:

0LU1 99.62/75/87c fly 1x3x2, sold the 3 at 1.25 in 2k

3LU1 99.12/98.87/98.62p fly, bought for 3.25 in 5k

FOREX: Lower Than Expected Inflation Knocks GBP

- GBP is soft, trading lower against all others in G10, as GBP/USD continues the recent downtrend after yesterday's close below the 50-dma. The rate now targets the 100-dma at 1.3619, a level not closed below since late June last year. Soft inflation numbers were largely responsible, with CPI and RPI both missing expectations for February.

- Elsewhere, commodity-tied FX is firmer, with NOK and CAD improving as equity futures and oil markets bottom out and point higher ahead of NY hours.

- Focus turns to prelim February US durable goods orders, which are expected to slow to 0.5% from 3.4% previously. Prelim March PMI data also could prove interesting, with the US release due just after the Wall Street opening bell.

- The speaker slate is again busy, with Fed's Powell appearing in front of the Senate alongside Treasury Secretary Yellen. Fed's Williams, Daly, Evans & Barkin are due, as well as ECB's Lagarde on climate change.

FX OPTIONS: Expiries for Mar24 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1800(E320mln), $1.1960-75(E732mln), $1.2000-10(E615mln)

- USD/JPY: Y108.00($1.4bln-USD puts), Y108.45-50($586mln)

- EUR/NOK: Nok10.20(E844mln-EUR puts)

- AUD/USD: $0.7710-12(A$533mln)

- USD/CNY: Cny6.50($631mln-USD puts)

- USD/MXN: Mxn20.50($1.1bln-USD puts), Mxn21.25($583mln), Mxn21.48($675mln)

TECHS: Price Signal Summary - USD Extends Gains

- In the equity space, S&P E-minis are consolidating but remain vulnerable following last week's selling pressure from 3978.50, Mar 18 high. The support to watch is 3875.00, Mar 19 low. A break would confirm a breach of the 20-day EMA and reinforce short-term bearish conditions.

- In the FX space, EURUSD is weaker again this morning and has breached 1.1836, Mar 19 low. This opens 1.1800 next, the Nov 23 low. GBPUSD is weaker this morning. The pair has this week cleared 1.3779, Mar 5 low and a bear trigger. Note this also confirms a breach of the 50-day EMA and a bull channel base drawn off the Nov 2 low. The focus is on 1.3641, 38.2% retracement of the Sep 23 - Feb 24 bull cycle. USDJPY remains in an uptrend. Attention is still on 109.56, 76.4% of the Mar 2020 - Jan downleg and an important pivot resistance. Watch support at 108.34 Mar 10 low.

- On the commodity front, a bullish theme in Gold remains in place following the recovery that started Mar 8. The focus is on $1779.3, the 50-day EMA. Support is at $1719.3, Mar 18 low. Oil contracts remain in bear mode. Weakness in Brent (K1) yesterday opens $58.56, 38.2% of the Nov 2 - Mar 8 rally. In WTI (K1), scope is for a move to $55.65, also the 38.2% of the Nov 2 - Mar 8 rally.

- In the FI space:

- Bunds (M1) have probed resistance at 172.20, Mar 11 high. A clear break would open 172.51 next, Feb 16 high.

- Gilts (M1) have cleared resistance at 128.33, Mar 16 high, suggesting scope for an extension higher. The next key resistance is at 129.27, Mar 2 high.

- Treasuries (M1) remain in a downtrend and gains are considered corrective. Resistance is at 132-09, Mar 17 high and today's intraday high. .

EQUITIES: Strong Bounce Off Lows For Europe And US

- Asian stocks closed weaker, with Japan's NIKKEI down 590.4 pts or -2.04% at 28405.52 and the TOPIX down 42.9 pts or -2.18% at 1928.58. China's SHANGHAI closed down 44.448 pts or -1.3% at 3367.061 and the HANG SENG ended 579.24 pts lower or -2.03% at 27918.14.

- European stocks are lower, with the German Dax down 64 pts or -0.44% at 14570.19, FTSE 100 down 7.62 pts or -0.11% at 6683.55, CAC 40 down 17.92 pts or -0.3% at 5912.92 and Euro Stoxx 50 down 0.23 pts or -0.01% at 3820.83.

- U.S. futures are advancing, with the Dow Jones mini up 85 pts or +0.26% at 32392, S&P 500 mini up 14.75 pts or +0.38% at 3914.5, NASDAQ mini up 126.5 pts or +0.97% at 13133.75.

COMMODITIES: Oil Leads Broad-Based Bounce

- WTI Crude up $1.27 or +2.2% at $58.8

- Natural Gas up $0.02 or +0.76% at $2.529

- Gold spot up $5.11 or +0.3% at $1730.54

- Copper up $0.65 or +0.16% at $408.65

- Silver up $0.2 or +0.8% at $25.1916

- Platinum up $10.09 or +0.86% at $1175.29

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.