Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY:

- EQUITIES AND OIL HIGHER, DOLLAR WEAKER IN OVERNIGHT TRADE

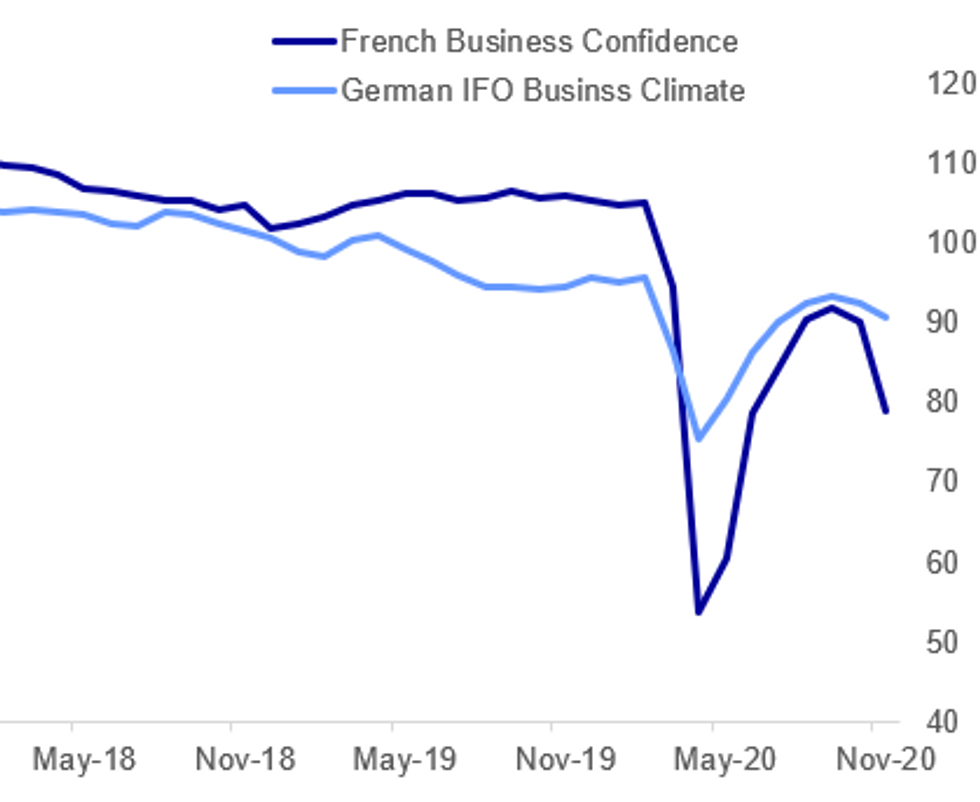

- FRENCH, GERMAN BUSINESS CLIMATES WEAKEN IN NOV. AS LOCKDOWNS TAKE TOLL

- E.C.B. WARNS OF ECONOMIC HIT IF PANDEMIC SUPPORT IS PHASED OUT

- GERMANY EXPECTS SOLUTION ON E.U. BUDGET ROW WITHIN DAYS

Fig.1: Lockdowns Weigh On Business Climate

BBG, MNI

BBG, MNI

NEWS:

GERMAN DATA: The Ifo business climate indicator fell to 90.7 in Nov, coming in slightly stronger than markets expected (BBG: 90.2)

- Both current conditions and expectations eased in Nov amid the second wave ofCovid-19 which interrupted the German economy's recovery.

- Expectations led the decline as companies are significantly more pessimistic, with falls seen in every sector.

- Manufacturing held up well in Nov with current conditions up markedly as order rose, but expectations for the coming months cooled.

- The service sector took the largest hit in Nov, falling back in negative territory for the first time since June.* Both the assessment of the current conditions and expectations decreased with hospitality and hotels seeing the largest decline.

- Trade business climate worsened as well, while it eased to a slower extent in the construction sector.

- Retail trade and service business climate took the largest hit of the newly introduced second lockdown with retail trade sentiment plummeting 23pt to 72,while service sector business confidence dropped 12pt to 77.

- Both indicators declined to their lowest levels since May

- Sub-sectors particularly affected by the lockdown such as accommodation and catering, firms specialized retail trade, automobile trade and repair saw the largest drops, while food retail trade in food offset some these falls.

- Manufacturing sentiment eased as well in Nov, however the indicator only fell by 2pt to a three-month low of 92.

- Employment climate eased further in Nov, falling 6pt to 83 and registering far below the pre-crisis level of 105.

- Employment prospects declined markedly in the retail trade and service sector and eased slightly in the industrial sector, while construction saw employment prospects holding up.

EUROZONE/E.C.B. (RTRS): The European Central Bank warned on Tuesday of painful "cliff effects" for households and companies if governments and regulators phase out the economic support they have provided to cushion the impact of the coronavirus pandemic. The ECB estimates the euro zone's five largest economies will lose 2% to 4% of their gross domestic product if these measures, ranging from loan guarantees and moratoria to short-time working schemes, are left to expire by the end of 2021."The simultaneous termination of policy measures could trigger a protracted downward shift in the recovery path," the ECB said. "Such cliff-edge effects would be concentrated in the first half of 2021."

BREXIT/BANKS (BBG): Goldman Sachs Group Inc. is planning a European stock trading platform to ensure its clients can still buy and sell shares even without a post-Brexit agreement to allow dealing in London. The Wall Street bank has applied to French regulators to start a Paris-based trading venue called SIGMA X Europe, according to the company. It intends to open before Jan. 4 subject to regulatory approvals.

FOREX: Citi's prelim month-end rebalancing model indicates an above average USD sell signal into Monday 30th November. They write that this month's USD sell signal is almost entirely driven by foreigners' needs to hedge gains in US equities. The contribution to the USD sell signal from US fixed income hedges is only adding marginally this month, while US-based investors will to a lesser degree be USD buyers to hedge gains in their foreign assets.DATA:

FIXED INCOME: Back to flat

After a soft start to the day for core we have seen a bid emerge since around 9:15GMT/4:15ET although there appears to be little in the way of headline drivers behind the move. This has led to Treasuries, gilts and Bunds being largely unchanged on the day.

- German Q3 GDP was revised a little higher and the IFO current assessment component was higher than expectations but the IFO expectations component disappointed. There was little immediate market reaction to either release, however.

- Looking ahead we have a number of central bank speakers including ECB's Lagarde, Lane, Schnabel, Rehn, de Cos; Fed's Clarida, Williams, Bullard and the BoE's Haskel.

- TY1 futures are flat today at 138-10 with 10y UST yields up 0.4bp at 0.859% and 2y yields down -0.1bp at 0.161%.

- Bund futures are down -0.06 today at 175.35 with 10y Bund yields up 0.8bp at -0.574% and Schatz yields up 0.3bp at -0.758%.

- Gilt futures are down -0.05 today at 134.90 with 10y yields up 0.9bp at 0.326% and 2y yields up 1.0bp at -0.24%.

FOREX: NZD Surges as House Prices Could Be Added to Policy Remit

After posting a decent rally on Monday, USD's role has reversed this morning, with the greenback the weakest currency in G10. Many are pinning the pullback in the dollar on news that Trump has granted Biden's team access to transition materials including briefings and initial protocols. While Trump is yet to formally concede and has vowed to continue to fight the election results, this is the clearest sign yet that a formal transition process could be underway.

EUR/USD is within range of yesterday's highs ahead of the NY crossover, but antipodean FX is where the USD weakness is most notable. NZD/USD topped out at a multi-year high of above $0.70, the highest level since mid-2018 on reports that the NZ government could add house prices to the RBNZ's policy remit. AUD is stronger in sympathy.

Datapoints are few and far between Tuesday, with no tier one releases on the docket. The speaker schedule should be of more interest, with BoE's Haskel, ECB's Lagarde & Lane, Fed's Bullard, Williams & Clarida and BoC's Wilkins all due.

EQUITIES: Optimism On Multiple Fronts Boosts Stocks Again

As was the case Monday, equities have risen to start Tuesday amid optimism on COVID vaccines and Brexit negotiations, combined with slightly diminished political uncertainty following news that President-elect Biden would formally be allowed to begin his transition to the office.

- Asian stocks closed mixed (in Japan's return from holiday), with Japan's NIKKEI up 638.22 pts or +2.5% at 26165.59 and the TOPIX up 35.01 pts or +2.03% at 1762.4. China's SHANGHAI closed down 11.667 pts or -0.34% at 3402.823 and the HANG SENG ended 102 pts higher or +0.39% at 26588.2.

- European equities are higher, with the German Dax up 117.62 pts or +0.9% at 13202.46, FTSE 100 up 55.15 pts or +0.87% at 6376.19, CAC 40 up 65.79 pts or +1.2% at 5542.32 and Euro Stoxx 50 up 36.98 pts or +1.07% at 3490.98.

- U.S. futures are stronger, with the Dow Jones mini up 278 pts or +0.94% at 29824, S&P 500 mini up 27 pts or +0.76% at 3603, NASDAQ mini up 41.5 pts or +0.35% at 11946.75.

COMMODITIES: Oil Breaks Higher

Industrial commodities are the standout performers, with WTI breaking through resistance at $43.33 though off session highs (next resistance at $44.15). Silver and Gold are weaker despite a lower USD.

- WTI Crude up $0.36 or +0.84% at $43.42

- Natural Gas up $0.02 or +0.63% at $2.728

- Gold spot down $13.98 or -0.76% at $1826.82

- Copper up $5 or +1.53% at $332.8

- Silver down $0.19 or -0.82% at $23.4058

- Platinum up $9.4 or +1.01% at $940.23

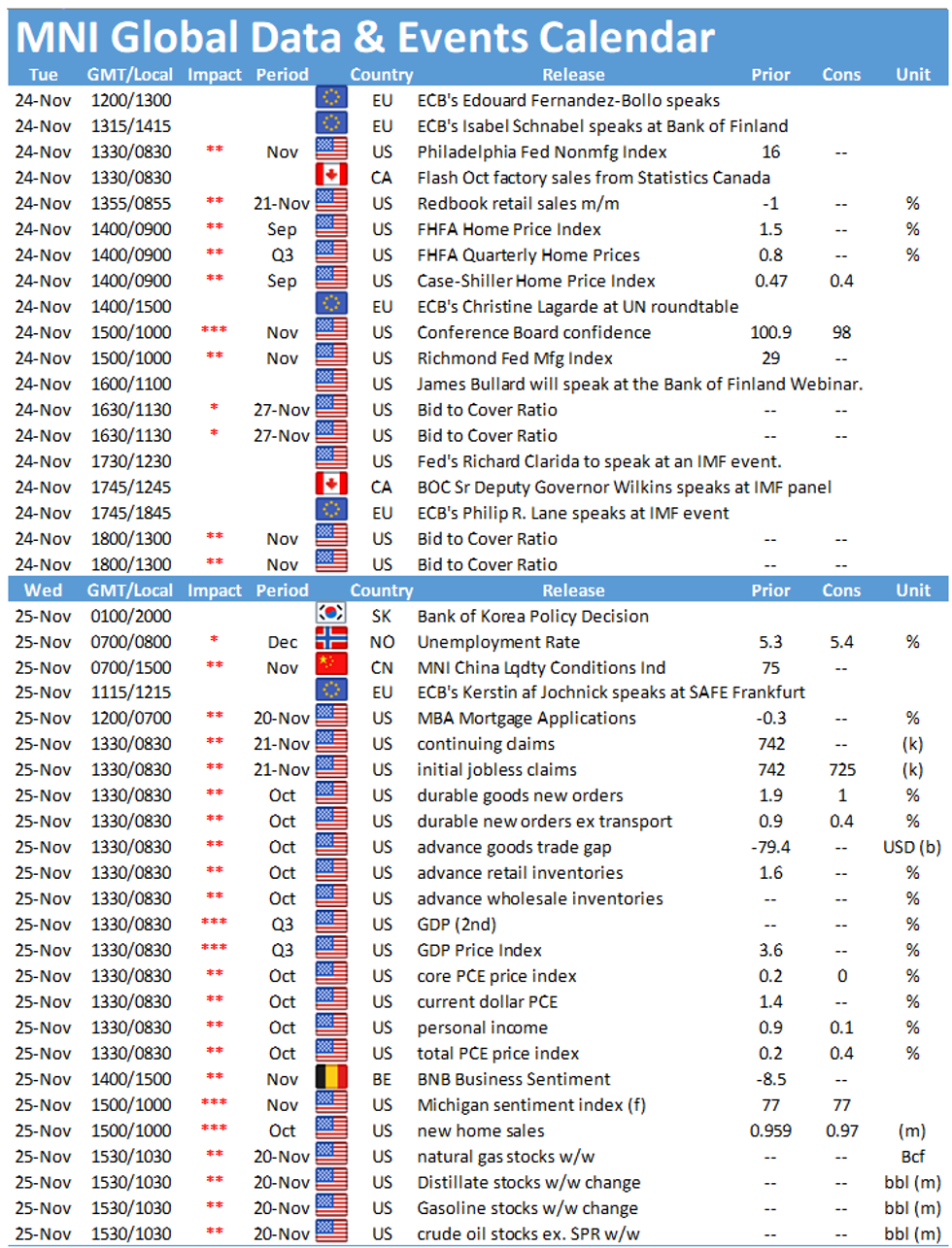

LOOK AHEAD:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.