Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SWEDEN

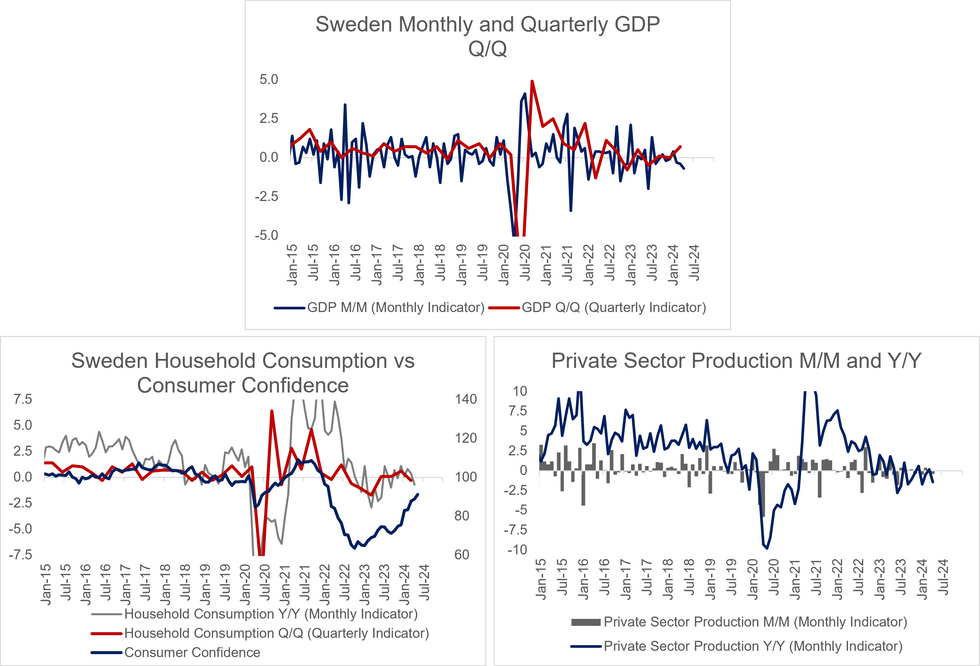

Swedish April monthly activity data began Q2 on a weak note, with a fall in GDP (-0.7% M/M SWDA vs -0.4% prior) in May driven by declines in both household consumption (-0.4% vs -0.4% prior) and private sector production (-0.4% vs -0.1% prior).

- Overall, the data suggests that final domestic demand, although recovering, remains soft. A reminder that the Q1 GDP “beat” was largely driven by inventories, with household consumption a negative contributor to the 0.7% Q/Q print.

- There was no consensus for the data, and the likelihood of future revisions and imperfect correlation with actual quarterly GDP means caution should be taken with the initial interpretation (as usual).

- The 1.4% Y/Y WDA fall in private sector production was driven by the industrial and construction sectors, with services production flat in April 2024 vs a year ago.

- On the consumption side, restaurant, café and hotel consumption was weak on both an annual (-6.1% Y/Y WDA) and monthly (-2.0% M/M SWDA) basis. While the working day adjustment to the data attempts to account for the early Easter in 2024, there still may be a lingering impact from this timing which dragged in the index lower in April.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok