Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CHINA DATA

China CPI for Feb came in well below expectations, rising just 1.0% y/y, versus 1.9% expected. The detail looked soft (see this link for more details), while the core measure eased back to 0.6% y/y from 1.0% in Jan.

- The first chart below overlays the core print against the 2yr government bond yield. At face value this suggests downside pressure on yields, but the general theme from the NPC has been fresh stimulus may not materialize in the near term. This was hinted at by the modest growth target and in recent PBoC commentary (see this link). The NDRC stated CPI will within the target of around 3% this year.

- Today's outcome may reinforce calls that the authorities have some space to ease from an inflation standpoint. The authorities may want to see further prints though, particularly given the March PMIs pointed to rising inflation pressures.

Fig 1: China Core CPI & 2yr Bond Yields

Source: MNI - Market News/Bloomberg

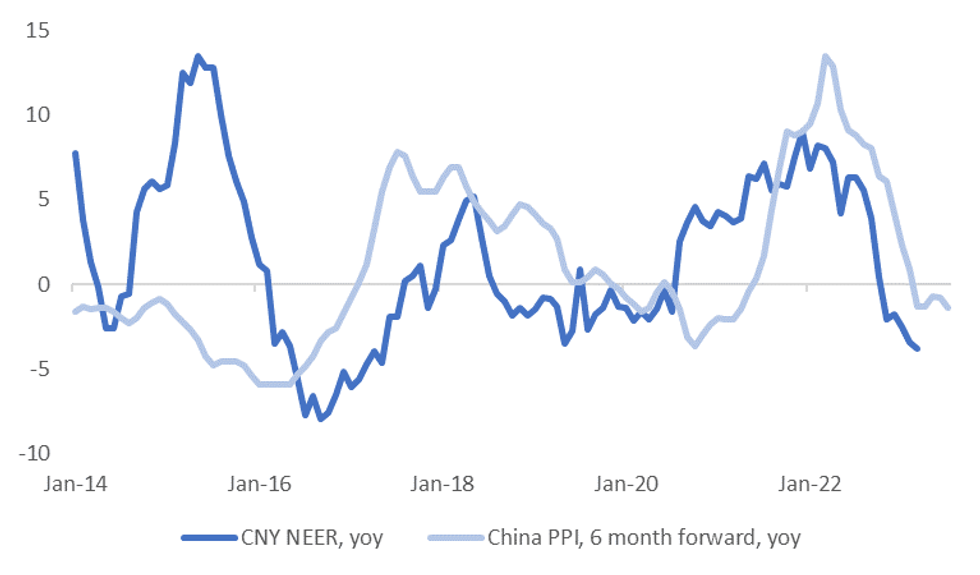

- The PPI also printed lower than expected, -1.4% y/y, versus -0.8% forecast. The second below overlays this metric (6 months forwards) against y/y changes in the CNY NEER.

- Lack of a sharp rebound in upstream price pressures doesn't point to the need for any sharp tightening in China financial conditions.

- USD/CNH has moved higher post the release, last near 6.9800, although broader USD sentiment has also found a firming footing.

Fig 2: China PPI Versus CNY NEER Y/Y

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok