Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

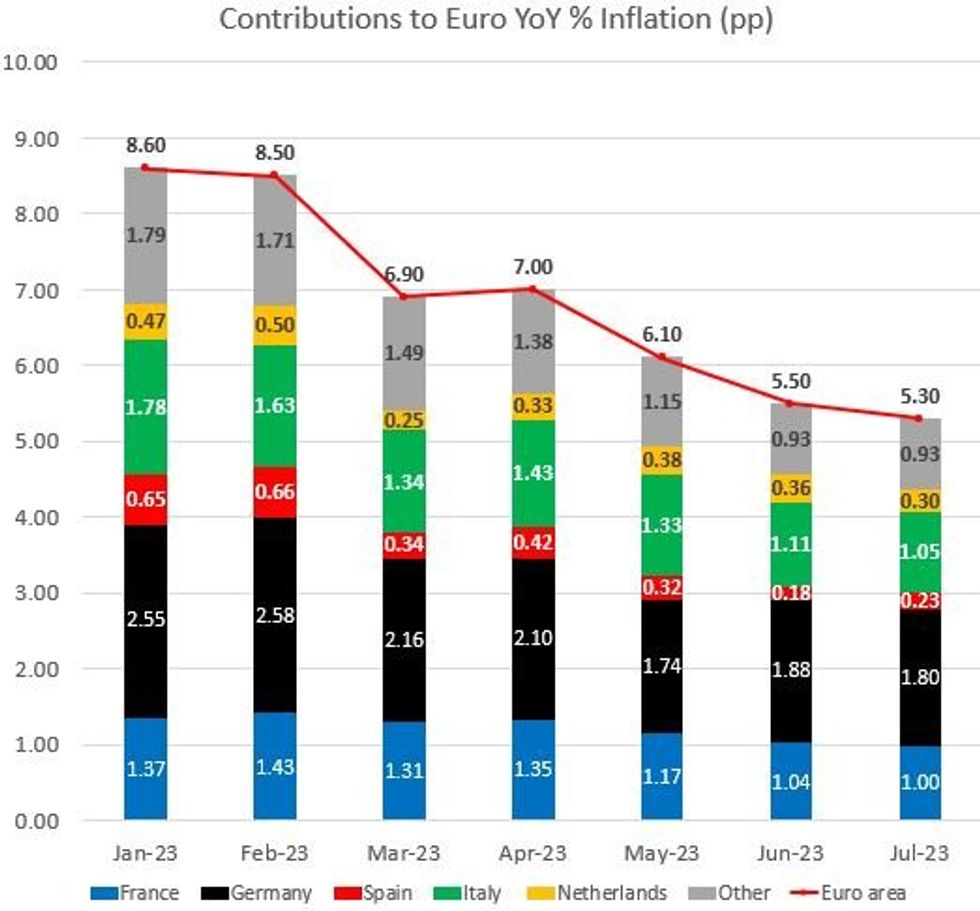

EUROZONE

Below are median estimates of flash August inflation for the 4 biggest eurozone countries by HICP weighting, starting with Germany and France:

Germany (28% of EZ HICP) – 1300UK Wed 30 Aug (after state-level data in the morning)

- HICP: 6.3% Y/Y (6.5% prior) / 0.3% M/M (0.5% prior)

- CPI: 6.0% Y/Y (6.2% prior) / 0.3% M/M (0.3% prior)

- German inflation is seen moderating from recent Y/Y services and core figures which have been driven in part by base effects from the 2022 travel ticket and the upward pressure provided by package holidays (which are more highly weighted in 2023 than in 2022) in the summer months. German electricity / gas prices are set to fall M/M, helping keep a lid on headline prices.

- August Flash PMIs showed an increase in inflationary pressures, driven by accelerated cost and price increases in the service sector, with Input cost and output prices rose for the first time in 11 / 7 months, respectively.

- Barclays: HICP 6.4% Y/Y (0.4% M/M)

- Goldman: HICP 6.5% Y/Y; core 6.2% Y/Y

- Morgan Stanley: HICP 6.2% Y/Y; CPI 6.1% Y/Y and 5.5% Core

- JPM: HICP 6.4% Y/Y, CPI 6.1% Y/Y and 0.3% M/M

- BofA: HICP 6.3% Y/Y, 0.3% M/M. CPI 6.2% Y/Y, 0.3% M/M.

France (20% of EZ HICP) – 0745UK Thu 31 Aug

- HICP: 5.4% Y/Y (5.1% prior) / 1.0% M/M (0.0% prior)

- CPI: 4.6% Y/Y (4.3% prior) / 0.8% M/M (0.1% prior)

- French measured electricity prices are set to soar as France adjusts its price cap, contributing heavily to overall Eurozone energy inflation in August; gas prices are seen as disinflationary.

- August flash PMIs showed inflation rates continued on their downward trajectory, with overall input price inflation down to a 29-month low, and selling price inflation slowing to its weakest since April 2021. However that masked mixed sectoral dynamics: manufactured goods output prices fell but services charges rose.

- Barclays: HICP 5.7% Y/Y (0.3% M/M)

- Goldman: 5.7% Y/Y; core 4.0%.

- Morgan Stanley: CPI 4.6% Y/Y

- JPM: HICP 5.6% Y/Y, CPI 4.7% Y/Y and 0.8% M/M

- BofA: HICP 5.5% Y/Y, 1.0% M/M; CPI 4.9% Y/Y, 1.0% M/M.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok