Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE

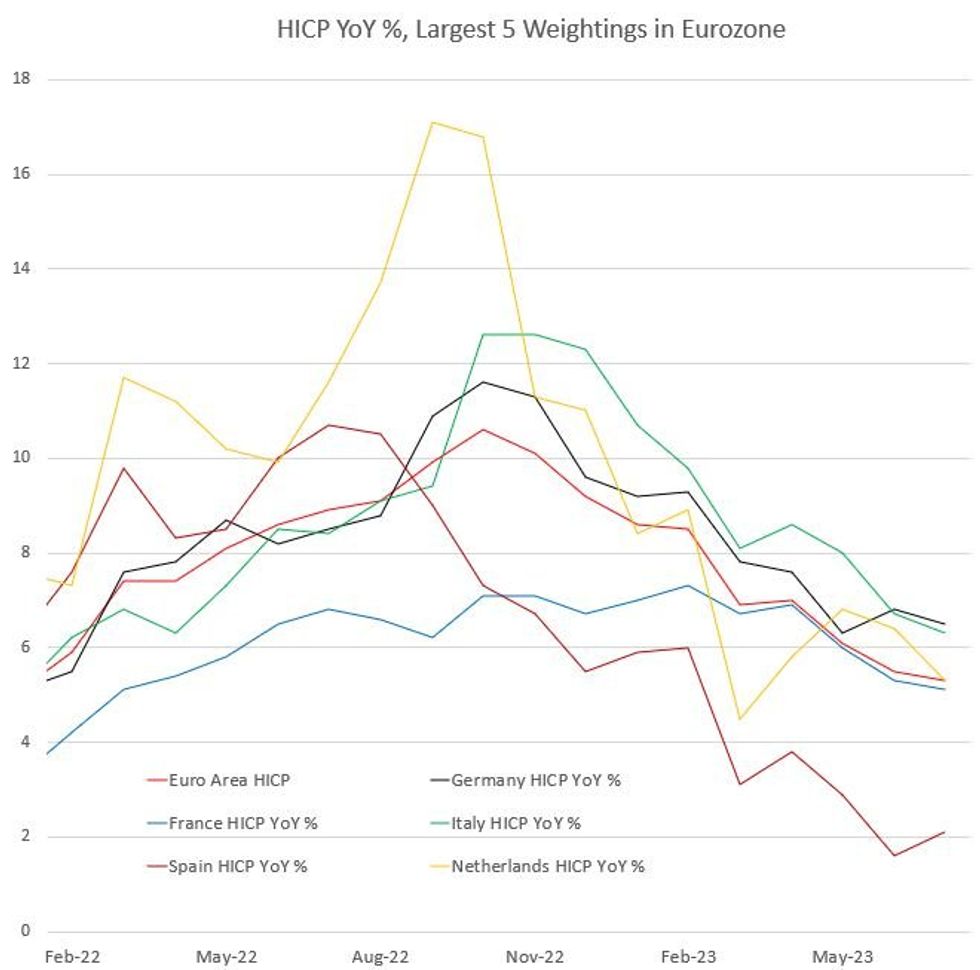

Spain (11% of EZ HICP) – 0800UK Wed 30 Aug

- CPI: 2.5% Y/Y (vs 2.3% prior); 0.5% M/M (vs 0.2% prior).

- Core CPI: 6.0% Y/Y (vs 6.2% prior).

- HICP: 2.3% Y/Y (vs 2.1% prior); 0.5% M/M (vs -0.1% prior).

- Headline inflation is seen rising on the back of a less negative base effect, while the continuation of summer sales should put continued pressure on semi-durable goods prices (e.g. clothing and footwear).

- Nomura expect electricity and gas prices to be broadly unchanged on the month, as electricity pass-through from wholesale to retail is largely complete and changes in regulated gas prices were already introduced last month.

- Barclays: HICP 2.5% Y/Y (0.6% M/M)

- Goldman: HICP 2.5% Y/Y; core 4.3% Y/Y and 0.43% M/M

- Morgan Stanley: CPI 2.7% Y/Y and core 6.2% Y/Y

- JPM: HICP: 2.3% Y/Y; CPI 2.3% Y/Y and 0.2% M/M

- BofA: HICP 2.3% Y/Y, 0.4% M/M. CPI 2.5% Y/Y, 0.4% M/M.

Italy (17% of EZ HICP) – 1000UK Thu 31 Aug

- CPI: 5.4% Y/Y (vs 5.9% prior); 0.4% M/M (vs 0.0% prior).

- HICP: 5.6% Y/Y (vs 6.3% prior); 0.3% M/M (vs -1.6% prior).

- Analysts expect base effects to push headline inflation lower, while core is expected to remain elevated. The continuation of summer sales should put continued pressure on semi-durable goods (e.g. clothing/footwear).

- Nomura expect deflation of both electricity and gas prices, following falls in electricity market prices and more regularly updated retail gas prices (now monthly rather than quarterly).

- Barclays: HICP 5.7% Y/Y (0.3% M/M)

- Goldman: 5.7% Y/Y; core 4.3% Y/Y.

- Morgan Stanley: CPI 5.3% Y/Y, core 4.1% Y/Y

- JPM: HICP 5.6% Y/Y, CPI 5.5% Y/Y and 0.4% M/M

- BofA: HICP 5.7% Y/Y, 0.3% M/M.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok