Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

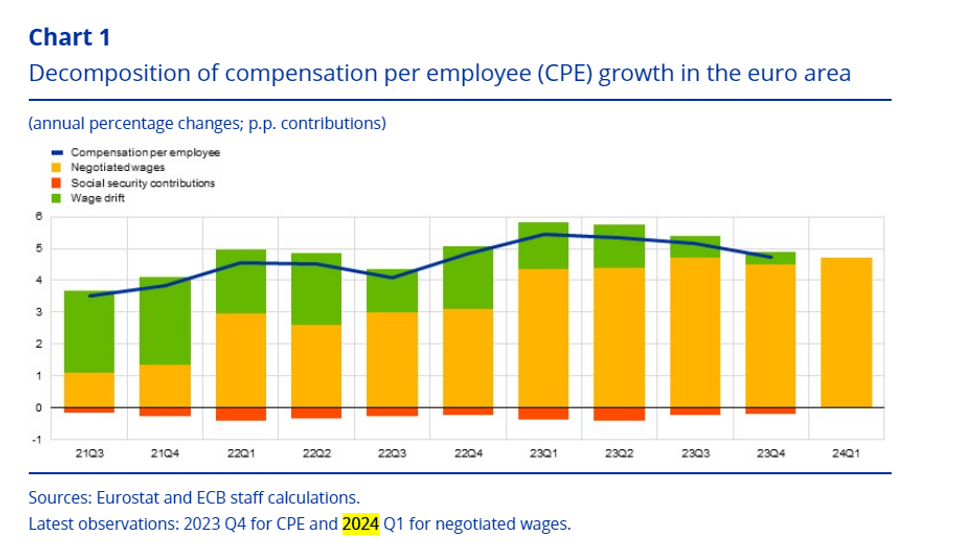

The ECB’s negotiated wages indicator rose by 4.69% Y/Y, up from 4.45% in Q4. An acceleration had been expected by some analysts following yesterday’s German March negotiated wages data (which were 11.7% Y/Y vs 5.9% in Feb).

- Prior to the German data, general consensus was for a modest deceleration to around 4.3% Y/Y. However, we note that the German data was inflated by one-off payments but still showed underlying strength.

- Taken alongside the preliminary Q1 labour cost index on Tuesday (which was 4.9% Y/Y vs 3.4% in Q4), this suggests upside risks to overall Eurozone compensation per employee and by extension unit labour costs – both released as part of the full national accounts on June 7.

- However, the ECB Governing Council still expect a gradual moderation in wage growth in the quarters ahead (e.g. Schnabel yesterday evening).

- From the ECB’s blog on negotiated wages: “Negotiated wage growth is expected to remain elevated in 2024, which is in line with the persistence that has been factored into Eurosystem staff forecasts and reflects the multi-year adjustment process for wages. However, wage pressures look set to decelerate in 2024”.

- The Indeed wage tracker has continued to moderate through 2024, which should be reflected in the negotiated wage and compensation per employee data going forward.

- ECB-dated OIS contracts were little changed following the release, currently pricing 23bps of cuts through the June meeting and a cumulative 26bps through July.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok