Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- MNI: Fed Keeping 50 BP Option Open For Later -- Ex-Staffers

- MNI INTERVIEW: Energy Prices Pose Risk For US Mfg Growth--ISM

- MNI SOURCES: Brussels To Delay Decision On Fiscal Rules Return

- MNI BRIEF: Bostic Says Fed Hikes Won't Stop Job Growth

- NATO FOREIGN MINISTERS TO HOLD EMERGENCY MEETING FRIDAY, Bbg

- Second Round Of Russia-Ukraine Talks Planned On March 2 - Tass Cites A Russian Source - Reuters

- World's biggest shipping company (Maersk) suspends container shipments to/from Russia, Business Insider

US

FED: The Federal Reserve is set to lift off from its near-zero setting with a quarter-point interest rate increase in March but 50bp hikes later this year are under consideration as inflation pressures worsen, former central bank staffers told MNI.

- The war in Ukraine is pushing up energy and commodities prices at a time when U.S. inflation continues to surprise to the upside. The Cleveland Fed's nowcast expects February CPI to accelerate by three-tenths to 7.8%, which would be a fresh 40-year high for the index.

- "There is an institutional bias towards doing things at a steady pace and that suggests a series of 25-basis point hikes," said Kenneth West, a University of Wisconsin economist who's been a visiting scholar at several regional Fed banks.

- However, "one factor that keeps inflation expectations anchored is conviction, and confidence that the Fed is committed to not letting inflation get out of control, so floating doing 50bp later is part of that," he said. Dovish Fed officials, such as Mary Daly of San Francisco, have said a 50bp move may be needed at some point down the road.

- "I don't feel that tension right now in terms of our thinking about policy," Bostic said in a discussion about the central bank's dual mandate, while noting he sees maybe four hikes this year. "It's a real strong signal that the economy has legs to stand on its own, and there's a momentum that is carrying through that will allow us to continue to see job growth through the course of this year as we think about getting our policy in a more regular stance."

- "I'm definitely concerned about that," Fiore said, when asked about oil prices rising above USD100 a barrel. "Eventually, that is the thing that really puts the brakes on, when prices get to a certain level because they go into everything."

- "At USD 100 it starts to get difficult," said Fiore, hopeful that the prices will incentivize developers to enter the market over the medium-term. But the ISM chief expressed confidence that the prices paid measure will continue to steadily fall in coming months and that supply chains will continue to improve in coming months.

EU: Council Pres. Says EU Must Take 'Serious Look' At Ukraine Membership Request

European Council President Charles Michel has stated that the EU must take a 'serious look' at Ukraine's membership request, officially signed by President Volodymyr Zelensky yesterday.

- Speaking to the European Parliament plenary Michel stated on Ukraine's request that, 'It'll be up to us to act in accordance with the times. It's going to be difficult. The Council will have to seriously look at the symbolic, political and legitimate request & make the appropriate choices in a determined & clearheaded manner.'

- Should be noted that while a path for accession could be cleared, the strict conditionality applied to membership applications makes the prospect of Ukraine being brought into the EU any time soon a slim one,

- Michel: "This [the Russian invasion] is geopolitical terrorism". Calls on Russia to, "stop the war, go home, let's talk." Says sanctions will "impose a cost on us, this is a price worth paying."

- EU High Representative for Foreign Affairs and Security Josep Borrell states in his speech that "I think this is the moment in which the geopolitical union is being born".

US TSYS

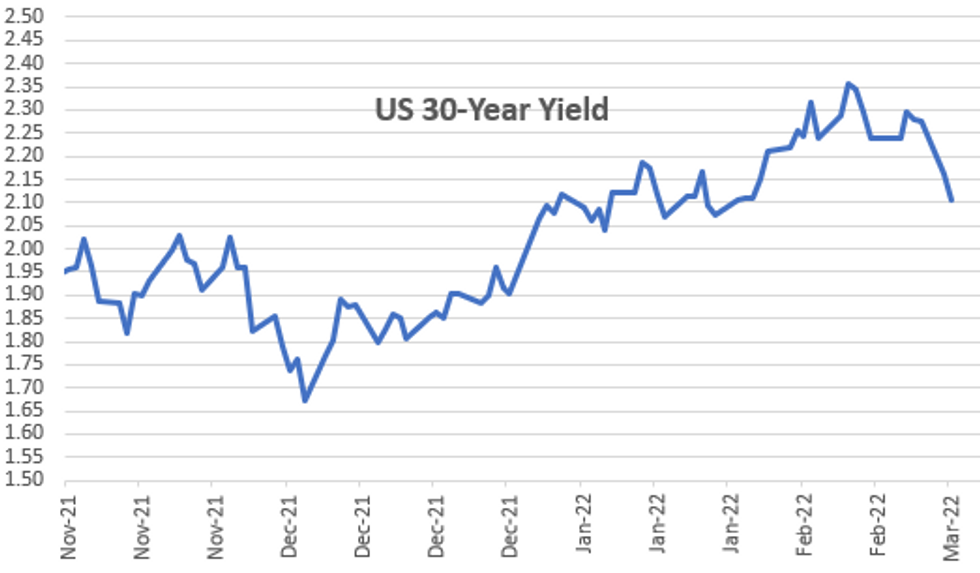

Tsy yields revisited midday lows in late trade, 30YY slipped to 2.0660%L, 2.1157% last (-.0454); 10YY 1.6800L, 1.7173% last -.1077.

- Knock-off affect of Russia's ground war in Ukraine and subsequent wide-ranging sanctions are leaving their mark. Induced stagflation?

- Hearing growing opinion that current events will/may derail central bank plans to hike rates as risk-off/safe-haven buying forces yields lower -- while economic growth falters due knock-off effects of sanctions on Russia having broader ripple effect on food and gas prices.

- Concerns over the Russia/Ukraine conflict getting worse/out of hand quickly more likely the main safe-haven driver -- not a more considered (esoteric) front-running of period of stagflation.

- In the meantime, shares of global banking, shipping, oil producers/distributors, defense contractors alternately being pulled higher/lower due to positive/negative risk exposure to Russia sanctions as well.

- Two days of falling Treasury yields and heavy buying in short end Eurodollar futures (Whites: EDH2-EDZ2 +0.19-0.22; Reds: EDH3-EDZ3 +0.430-0.470) has provided enough of a shift in narrative to draw traders off the sidelines Tuesday. By the close, chances of no hike by the Fed this month had risen to 12%.

- The 2-Yr yield is down 10.8bps at 1.3248%, 5-Yr is down 15.1bps at 1.5665%, 10-Yr is down 10.9bps at 1.7156%, and 30-Yr is down 6.4bps at 2.097%.

OVERNIGHT DATA

- US FINAL FEB MFG PMI 57.3r; JAN 55.5

- US FINAL MFG REVISED DOWN FROM 57.5 FOR FEB

- US REDBOOK: FEB STORE SALES +14.1% V YR AGO MO

- US REDBOOK: STORE SALES +13.4% WK ENDED FEB 26 V YR AGO WK

- US REDBOOK: WILL RESUME MONTH-TO-MONTH DATA COMPARISON IN MARCH

- US ISM PURCHASING MANAGERS MANUF INDEX 58.6 FEB VS 57.6 JAN

- US ISM PRICES PAID INDEX 75.6 FEB VS 76.1 JAN (NSA)

- US ISM NEW ORDERS INDEX 61.7 FEB VS 57.9 JAN

- US ISM EMPLOYMENT INDEX 52.9 FEB VS 54.5 JAN

- US ISM PRODUCTION INDEX 58.5 FEB VS 57.8 JAN

- US ISM SUPPLIER DELIVERY INDEX 66.1 FEB VS 64.6 JAN

- US ISM ORDER BACKLOG INDEX 65.0 FEB VS 56.4 JAN (NSA)

- US ISM INVENTORIES INDEX 53.6 FEB VS 53.2 JAN

- US ISM CUSTOMER INV INDEX 31.8 FEB VS 33.0 JAN (NSA)

- US ISM EXPORTS INDEX 57.1 FEB VS 53.7 JAN (NSA)

- US ISM IMPORTS INDEX 55.4 FEB VS 55.1 JAN (NSA)

- US JAN CONSTRUCT SPENDING +1.3%

- US JAN PRIVATE CONSTRUCT SPENDING +1.5%

- US JAN PUBLIC CONSTRUCT SPENDING +0.6%

- CANADIAN Q4 GROSS DOMESTIC PRODUCT +6.7% ANNUALIZED

- CANADIAN Q3 REVISED GDP +5.5% ANNUALIZED

- CANADIAN Q4 GDP +1.6% ON QOQ BASIS

- CANADA FLASH JAN GDP +0.2% MOM- STATSCAN

MARKETS SNAPSHOT

Key late session market levels:

- DJIA down 774.31 points (-2.28%) at 33163.85

- S&P E-Mini Future down 92 points (-2.11%) at 4282.25

- Nasdaq down 309.3 points (-2.2%) at 13457.88

- US 10-Yr yield is down 10.9 bps at 1.7156%

- US Jun 10Y are up 38.5/32 at 128-20.5

- EURUSD down 0.0093 (-0.83%) at 1.1127

- USDJPY down 0.17 (-0.15%) at 114.83

- WTI Crude Oil (front-month) up $8.64 (9.03%) at $104.42

- Gold is up $36.24 (1.9%) at $1945.41

- EuroStoxx 50 down 158.38 points (-4.04%) at 3765.85

- FTSE 100 down 128.05 points (-1.72%) at 7330.2

- German DAX down 556.17 points (-3.85%) at 13904.85

- French CAC 40 down 262.34 points (-3.94%) at 6396.49

US TSY FUTURES CLOSE

- 3M10Y -11.194, 139.092 (L: 134.257 / H: 152.885)

- 2Y10Y -1.467, 37.406 (L: 37.208 / H: 45.123)

- 2Y30Y +2.898, 75.379 (L: 70.742 / H: 83.581)

- 5Y30Y +7.603, 51.775 (L: 42.552 / H: 56.907)

- Current futures levels:

- Jun 2Y up 6/32 at 107-25.625 (L: 107-16.25 / H: 107-31.5)

- Jun 5Y up 23.75/32 at 119-0.75 (L: 118-03 / H: 119-10.75)

- Jun 10Y up 1-4.5/32 at 128-18.5 (L: 127-06 / H: 128-31.5)

- Jun 30Y up 2-9/32 at 158-31 (L: 156-10 / H: 159-22)

- Jun Ultra 30Y up 2-25/32 at 188-23 (L: 185-08 / H: 190-06)

US 10Y FUTURES TECH: (M2) Extends Recent Gains

- RES 4: 129-13 3.00 proj of the Feb 10 - 14 - 15 price swing

- RES 3: 129-00 Round number resistance

- RES 2: 128-23 High Jan 13

- PRICE: 128-12+ @ 11:43 GMT Mar 1

- SUP 1: 126-24 20-day EMA

- SUP 2: 125-29 Low Feb 25

- SUP 3: 125-14+ Low Feb 10 and the bear trigger

- SUP 4: 125-06+ Low May 30 2019 (cont)

Treasuries are firmer today as the contract extends the recovery that started Feb 10 off 125.14+. Price has cleared both the 20- and 50-day EMAs and the break of the latter EMA strengthens the current bullish theme. Resistance at 128-17, Jan 24 high has been tested. A clear break would signal scope for a climb towards the 129-00 handle next. On the downside, the 20-day EMA is seen as an initial firm support. It intersects at 126-24.

US EURODOLLAR FUTURES CLOSE

- Mar 22 +0.010 at 99.355

- Jun 22 +0.095 at 99.015

- Sep 22 +0.145 at 98.745

- Dec 22 +0.165 at 98.440

- Red Pack (Mar 23-Dec 23) +0.20 to +0.220

- Green Pack (Mar 24-Dec 24) +0.20 to +0.220

- Blue Pack (Mar 25-Dec 25) +0.170 to +0.20

- Gold Pack (Mar 26-Dec 26) +0.125 to +0.160

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- O/N -0.00014 at 0.07700% (-0.00014/wk)

- 1 Month -0.00686 to 0.23457% (+0.00400/wk)

- 3 Month +0.00657 to 0.51086% (-0.01214/wk) ** Record Low 0.11413% on 9/12/21

- 6 Month -0.04085 to 0.76386% (-0.06485/wk)

- 1 Year -0.11129 to 1.17671% (-0.15400/wk)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 0.08% volume: $65B

- Daily Overnight Bank Funding Rate: 0.07% volume: $236B

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 0.05%, $1.052T

- Broad General Collateral Rate (BGCR): 0.05%, $369B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $351B

- (rate, volume levels reflect prior session)

NY Fed Purchase Operation: The Desk plans to purchase approximately $20 billion, ending Thu, March 9.

- TIPS 7.5Y-30Y, appr $601M accepted vs. $2.413B submission

- Next scheduled purchases

- Thu 03/03 1100-1120ET: Tsy 7Y-10Y, appr $1.625B vs. $3.225 prior

- Tue 03/08 1010-1030ET: Tsy 22.5Y-30Y, appr $1.825B steady

- Thu 03/09 1010-1030ET: Tsy 2.25Y-4.5Y, appr $4.025B

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage recedes to $1,552.950B w/ 77 counterparties vs. $1,596.052B prior session -- remains well off all-time high of $1,904.582B on Friday, December 31.

PIPELINE: $4B American Express 3Pt Launched

$4B Amex 3-parter lion's share of $14.4B expected to price Tuesday- Date $MM Issuer (Priced *, Launch #)

- 03/01 $4B #American Express $1.75B 3Y +80, $500M 3Y SOFR+93, $1.75B 5Y +100

- 03/01 $3B *European Investment Bank 7Y SOFR +32

- 03/01 $3B #Schwab $1.5B 5Y +90, $500M 5Y FRN/SOFR+105, $1B 10Y +120

- 03/01 $2.5B #Capital One $1.25B 4NC3 +115, $1.25B 4NC3 FRN/SOFR, 8NC7 +160

- 03/01 $1.15B #Duke Energy Carolinas $500M 10Y +115, $650M 30Y +145

- 03/01 $750M #CME Group 10Y +98

FOREX: Souring Risk Sentiment Weighs On Euro, EURUSD Prints Below 1.1100

- Amid the ongoing Russia/Ukraine warfare, market expectations of the first ECB rate hike were pushed back to 2023, in turn weighing on the Euro throughout Tuesday’s session.

- Euro weakness was fairly broad based with notable extensions lower in EURJPY and EURCHF, the latter sinking to the lowest point since shortly after the removal of the floor in January 2015.

- EURUSD (-0.84%) also plunged to fresh recent lows, printing below the 1.11 handle to 1.1090. Having temporarily breached support and the bear trigger through 1.1106, the next targets are 1.0976, 2.00 projection of the Jan - Jun - May ‘21 price swing and 1.0871 Low May 25, 2020.

- EURUSD weakness and renewed selling pressure in equities lent support to the dollar index which climbed around 0.7%. Heavy euro crosses and the continued surge in commodity prices prompted relative resilience in the likes of AUD (-0.17%), NZD (-0.34%) and to an extent CAD (-0.45%).

- EURGBP weakness also kept GBP on a relatively firm footing, however, cable played catch up to the broad USD strength, shooting down from 1.34 to within close proximity of the 1.33 handle.

- In emerging markets, PLN, HUF and CZK were all offered throughout the session amid the single currency weakness and their direct exposure to the Ukraine crisis. Both Hungarian and Polish central banks took the opportunity to verbally intervene, dragging the local currencies off the worst levels.

- Australian GDP data kicks off Wednesday’s APAC session before the European docket is highlighted by Eurozone HICP Inflation flash estimates. Later on Wednesday, the Bank of Canada are expected to commence lift-off with a quarter point hike to 0.5%.

Wednesday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 02/03/2022 | 0001/0001 | * |  | UK | BRC Monthly Shop Price Index |

| 02/03/2022 | 0700/0700 | * | | UK | Nationwide House Price Index |

| 02/03/2022 | 0855/0955 | ** |  | DE | unemployment |

| 02/03/2022 | 1000/1000 | ** | | UK | Gilt Outright Auction Result |

| 02/03/2022 | 1000/1100 | *** |  | EU | HICP (p) |

| 02/03/2022 | 1000/1100 | | EU | ECB Schnabel at BMAS roundtable | |

| 02/03/2022 | 1100/1200 | | EU | ECB de Guindos Q&A at Universidad Carlos III | |

| 02/03/2022 | 1200/0700 | ** |  | US | MBA Weekly Applications Index |

| 02/03/2022 | 1315/0815 | *** | | US | ADP Employment Report |

| 02/03/2022 | 1400/0900 | | US | Chicago Fed's Charles Evans | |

| 02/03/2022 | 1430/0930 | | US | St. Louis Fed's James Bullard | |

| 02/03/2022 | 1500/1000 | *** |  | CA | Bank of Canada Policy Decision |

| 02/03/2022 | 1500/1000 | | US | Fed Chair Pro Tempore Jerome Powell | |

| 02/03/2022 | 1530/1030 | ** | | US | DOE weekly crude oil stocks |

| 02/03/2022 | 1600/1700 | | EU | ECB Lane lecture at Hertie School Berlin | |

| 02/03/2022 | 1630/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 02/03/2022 | 1830/1830 | | UK | BOE Tenreyro speech to Economic Research Council | |

| 02/03/2022 | 1900/1400 | | US | Fed Beige Book | |

| 02/03/2022 | 2000/2000 | | UK | BOE Cunliffe speech at Oxford Union | |

| 02/03/2022 | 2130/1630 | | US | New York Fed's Lorie Logan | |

| 03/03/2022 | 2200/0900 | * |  | AU | IHS Markit Final Australia Services PMI |

| 03/03/2022 | 0030/1130 | ** | | AU | Trade Balance |

| 03/03/2022 | 0030/1130 | * | | AU | Building Approvals |

| 03/03/2022 | 0030/0930 | ** |  | JP | IHS Markit Final Japan Services PMI |

| 03/03/2022 | 0145/0945 | ** |  | CN | IHS Markit Final China Services PMI |

| 03/03/2022 | 0700/0200 | * |  | TR | Turkey CPI |

| 03/03/2022 | 0730/0830 | ** |  | SE | Manufacturing PMI |

| 03/03/2022 | 0730/0830 | ** | | SE | Services PMI |

| 03/03/2022 | 0730/0830 | *** |  | CH | CPI |

| 03/03/2022 | 0815/0915 | ** |  | ES | IHS Markit Services PMI (f) |

| 03/03/2022 | 0845/0945 | ** |  | IT | IHS Markit Services PMI (f) |

| 03/03/2022 | 0850/0950 | ** |  | FR | IHS Markit Services PMI (f) |

| 03/03/2022 | 0855/0955 | ** | | DE | IHS Markit Services PMI (f) |

| 03/03/2022 | 0900/1000 | ** | | EU | IHS Markit Services PMI (f) |

| 03/03/2022 | 0930/0930 | ** | | UK | IHS Markit/CIPS Services PMI (Final) |

| 03/03/2022 | 1000/1100 | ** | | EU | retail sales |

| 03/03/2022 | 1000/1100 | ** | | EU | unemployment |

| 03/03/2022 | 1000/1100 | ** | | EU | PPI |

| 03/03/2022 | 1330/0830 | ** | | US | WASDE Weekly Import/Export |

| 03/03/2022 | 1330/0830 | ** | | US | Jobless Claims |

| 03/03/2022 | 1330/0830 | ** | | US | Non-Farm Productivity (f) |

| 03/03/2022 | 1445/0945 | *** | | US | IHS Markit Services Index (final) |

| 03/03/2022 | 1500/1000 | *** | | US | ISM Non-Manufacturing Index |

| 03/03/2022 | 1500/1000 | ** | | US | factory new orders |

| 03/03/2022 | 1500/1000 | | US | Fed Chair Pro Tempore Jerome Powell | |

| 03/03/2022 | 1530/1030 | ** | | US | Natural Gas Stocks |

| 03/03/2022 | 1630/1130 | ** | | US | NY Fed Weekly Economic Index |

| 03/03/2022 | 1630/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 03/03/2022 | 1630/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 03/03/2022 | 1630/1130 | | CA | BOC Governor Macklem speech, "Economic Progress Report." | |

| 03/03/2022 | 2030/1530 | | CA | BOC Governor Macklem testifies at House committee. | |

| 03/03/2022 | 2130/1630 | | US | New York Fed's Lorie Logan | |

| 03/03/2022 | 2300/1800 | | US | New York Fed's John Williams |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.