Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

AUSTRALIA

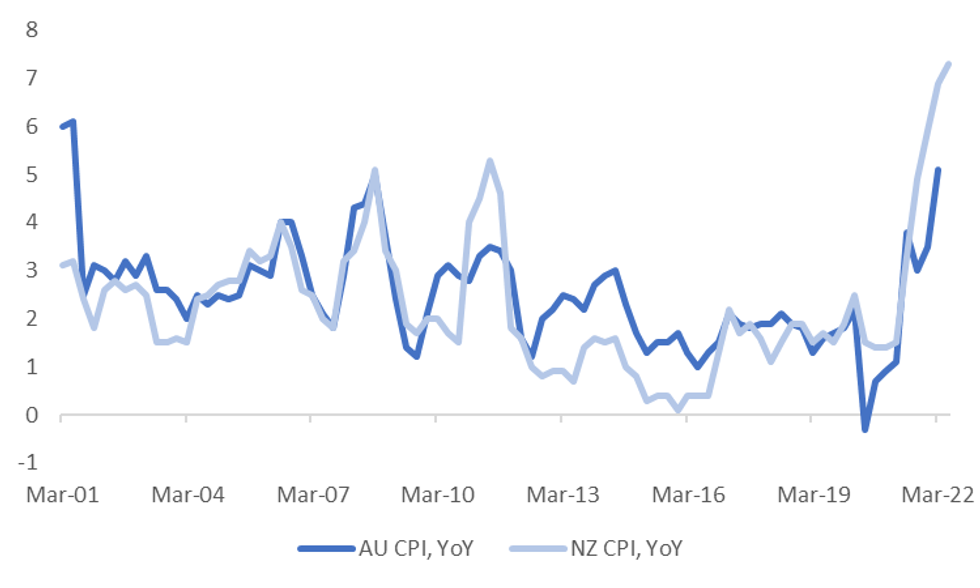

Next Wednesday's Q2 CPI data will be the key focus point next week. To recap, the market consensus is for a further decent step up - headline to 6.2% from 5.1% in Q1, 4.7% for the trimmed mean (the RBA’s preferred core measure) versus 3.7% last quarter. The quarterly pace is expected to be more benign, at least relative to recent history. For headline the forecast is 1.9% versus 2.1% previously, while core 1.5% from 1.4% in Q1.

- The general bias towards upside inflation surprises in major economies suggests risks for the AU print rest to the upside. The Citi inflation surprise index is off its record highs but remains very elevated by historical standards.

- The recent NZ Q2 CPI print also points to upside risks. This data surprised on the upside earlier in July. The chart below plots the YoY CPI trends for both economies.

- The long run correlation (past 2 decades) for quarterly changes in headline CPI for the two economies is +56%. For the past 3 years this is +71%. Not surprisingly, these correlations are higher in YoY terms.

- For core inflation, the long run correlation (for YoY data) is 57%, but higher in recent years.

- As we noted yesterday, short term correlations for the AUD and yield spreads have picked up in recent weeks. Next week's data could certainly influence market thinking around the pace of rate hikes of the next 6 months.

Fig 1: AU & NZ CPI YOY

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok