Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

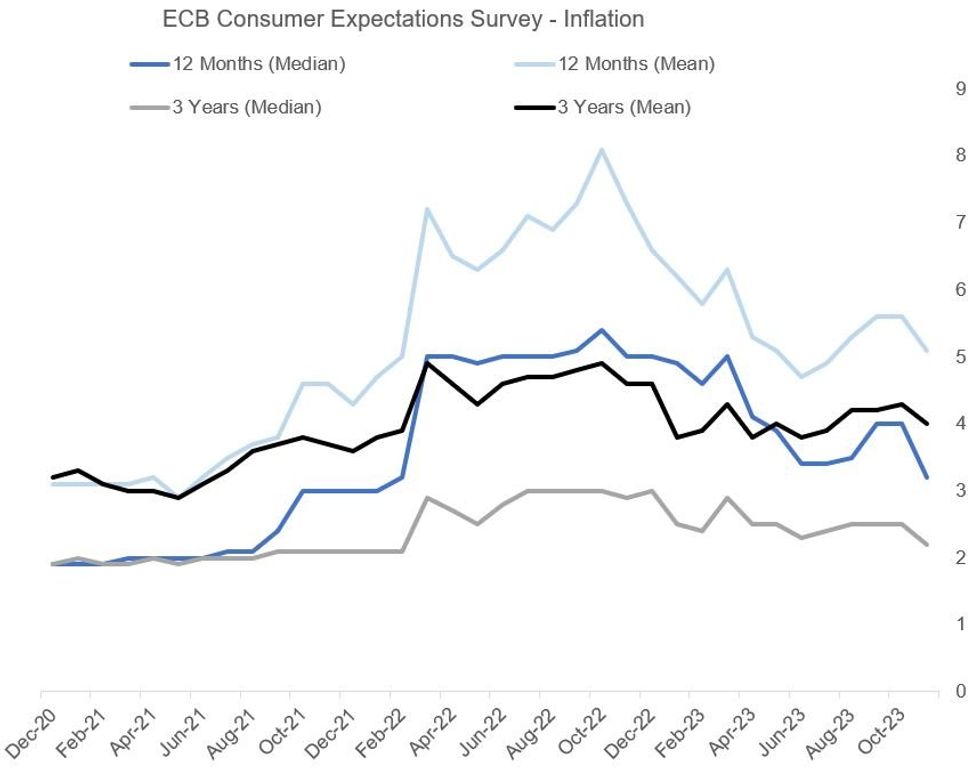

Eurozone consumer inflation expectations fell sharply in November, as measured by the ECB's CES survey. As usual, we wouldn't read deeply into the month-to-month survey results, but in isolation the latest reading suggests that public inflation expectations are less likely to restrain ECB policymakers from easing policy in 2024.

- The most notable pullback was in the 12-month ahead median expectation of 3.2% (from 4.0% in both Sept and Oct), marking the lowest since the Russia-Ukraine conflict began in February 2022.

- But each of the other key metrics showed progress as well: the 12 month mean expectation dropped to 0.5pp to 5.1% (lowest since Jul 2023), while the longer-term metrics also showed notable falls: 3-year ahead median down 0.3pp to 2.2% (lowest since Feb 2022), with the 3-year mean down 0.3pp to 4.0% (lowest since Jul 2023).

- Spanish inflation expectations remained an outlier to the upside (12-month ahead inflation seen at close to 5%), but respondents in the all 6 economies in the survey (incl Germany, Italy, Belgium, France, Netherlands) saw flat/lower expectations over a 3-year horizon.

Elsewhere in the survey, household spending and income expectations were relatively steady, as were economic growth expectations for the next 12 months.

- Employment expectations were steady, if anything with a bias toward greater strength vs previous months (eg median probability of finding a job ticked higher).

- One unusual standout was a jump in the percentage who applied for credit over the previous 3 months to a survey high just below 18% (which in turn appeared to be driven by rises in Spain and Germany), alongside drops in perceived access to credit.

Source: ECB CES, MNI

Source: ECB CES, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok