Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

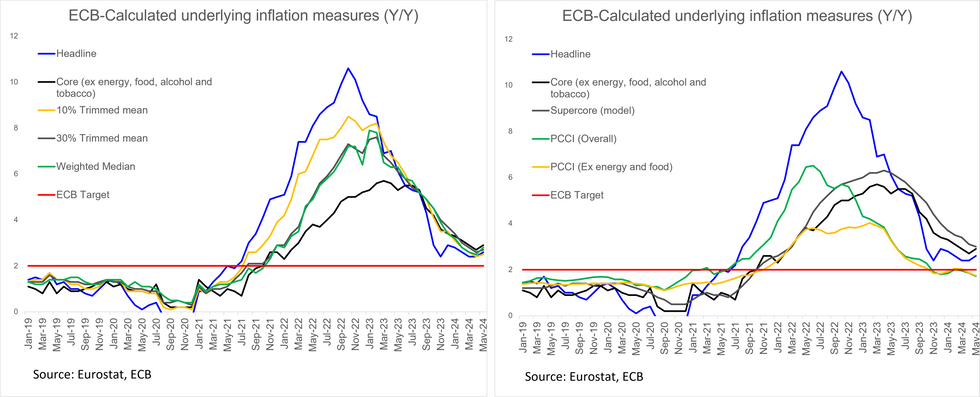

The ECB’s preferred underlying inflation metric reached its lowest level since July 2021 in May, in contrast to the acceleration seen in headline, core and services metrics.

- PCCI ex-energy and food was 1.74% Y/Y, down from 1.86% in April and 2.03% in March. Headline PCCI also moderated to 1.71% Y/Y from 1.85% prior, the lowest since December 2020.

- Supercore - the other model-based underlying inflation measure produced by the ECB - also softened a touch to 3.0% Y/Y (vs 3.1% prior).

- In contrast, the weighted median and 10/30% trimmed mean measures each ticked up between 0.1 and 0.3pp.

- This divergence can be explained by the model-based measures “stripping out” temporary effects that may have pushed up core and headline inflation in May, an example being the removal of German public transport ticket base effects.

- JP Morgan noted that the final May inflation print “suggested that the timing of Easter had an (upward) impact in May, but that the underlying trajectory in services was solid even without this”.

- As such, although Governing Council members will welcome the moderation in some of the underlying measures, further evidence of services disinflation will be required before entertaining a second rate cut this year.

- ECB-dated OIS contracts price just 1bp of easing through the July meeting, with several speakers having pointed to projection meetings (e.g. September) as the more likely gatherings to make policy rate adjustments.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok