Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMAN DATA

Germany (28% of EZ HICP - 1300UK Wed 29 November (after state-level data in the morning)

Consensus:

- HICP: 2.5% Y/Y (3.0% prior) / -0.5% M/M (-0.2% prior)

- CPI: 3.5% Y/Y (3.8% prior) / -0.1% M/M (0.0% prior)

German CPI saw a broad-based decline in October across energy, goods and services as well as an improvement in MNI’s inflation breadth metrics (where 31% of components had annual rates below 2% Y/Y vs 20% in September). November is also expected to show disinflation on both headline and core.

- The core print is expected to be pulled down by seasonal effects, most notably in the package holidays component due to basket weighting effects.

- Energy prices will see slow underlying declines after last year’s high wholesale prices locked many consumers in costly long-term contracts, which will be phased out over time. However, government subsidies from last winter will very likely trigger a tick up in December as base effects kick in, even with PPI still deeply in deflationary territory.

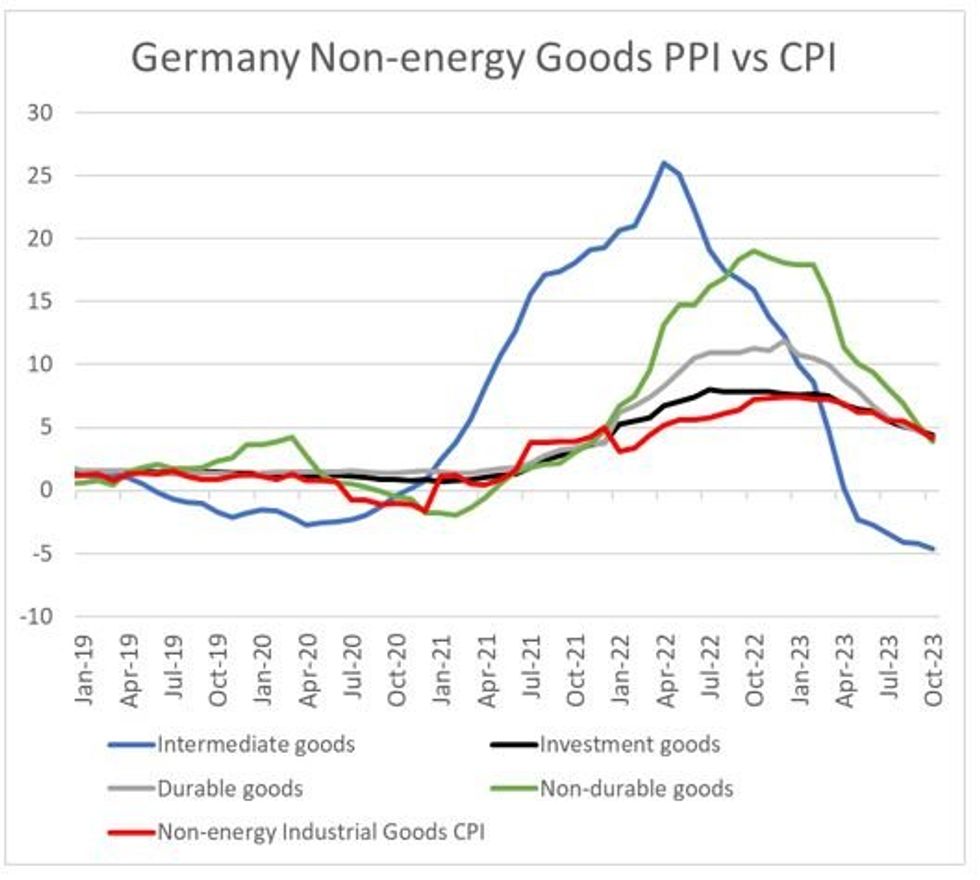

- October PPI continued to show disinflation/deflationary dynamics in the core goods pipeline, though the November flash PMI signalled output prices rising for both manufacturing and services (in spite of input costs continuing to fall in the manufacturing sector).

The early focus will be on the state-level data as always, with North-Rhine Westphalia CPI published at 0630UK time. One way to benchmark the data when it comes out: Barclays forecasts NRW headline +0.07% M/M NSA vs -0.08% Oct, with core +0.06% vs +0.17% Oct (core goods +0.48%/+0.45% Oct; core services -0.18% /0.00% Oct), which they see translating to -0.93% M/M / -1.02% M/M core German HICP.

Source: Destatis, Eurostat, MNI

Source: Destatis, Eurostat, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok