Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SPAIN DATA

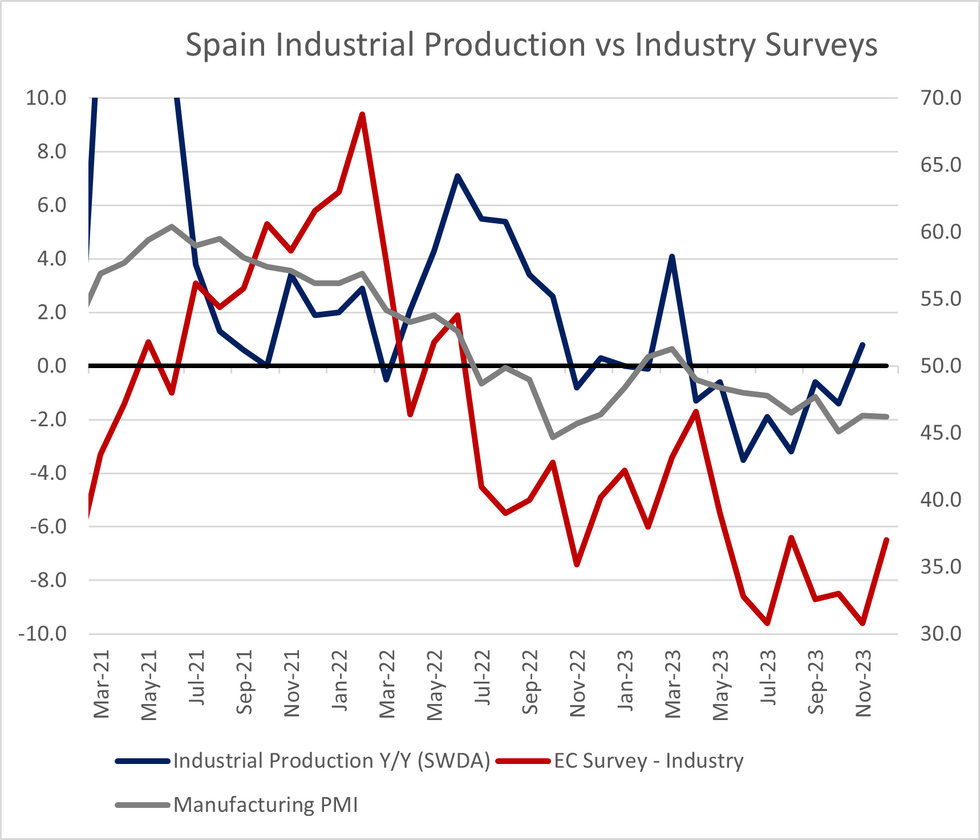

Spanish industrial production for November grew on an annual basis for the first time in 8-months, at +0.8% Y/Y (SWDA, vs a downwardly revised -1.4% prior). There was no consensus for the annual print.

- The industrial/manufacturing outlook in Spain appears somewhat brighter than in Germany (which this week reported a 6th consecutive Y/Y fall), but remains weak according to the latest survey data. The Spanish manufacturing PMI remained sluggish below 50 in December, and while the latest EC Industry survey picked up to -6.5 (vs -9.6 prior), it was the 18th consecutive reading below zero.

- On a sequential monthly basis, production exceeded consensus to rise +1.0% M/M (vs +0.2% cons, a downwardly revised -0.7% prior). The level of the SWDA index remains just over 2% below the post-covid peak seen in June 2022.

- The 3MMA of the monthly series also grew 1.0% vs October, after negative prints in the five months prior.

- All sub-components of the index rose in November, with capital goods rising +2.0% M/M (vs -1.7% prior) and consumer goods +1.7% M/M (vs -0.6% prior).

- On an annual basis, energy production ended a 7-month streak of negative prints to grow +1.7% M/M. Note that the index is measured in volume terms.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok