Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMAN DATA

MNI (London)

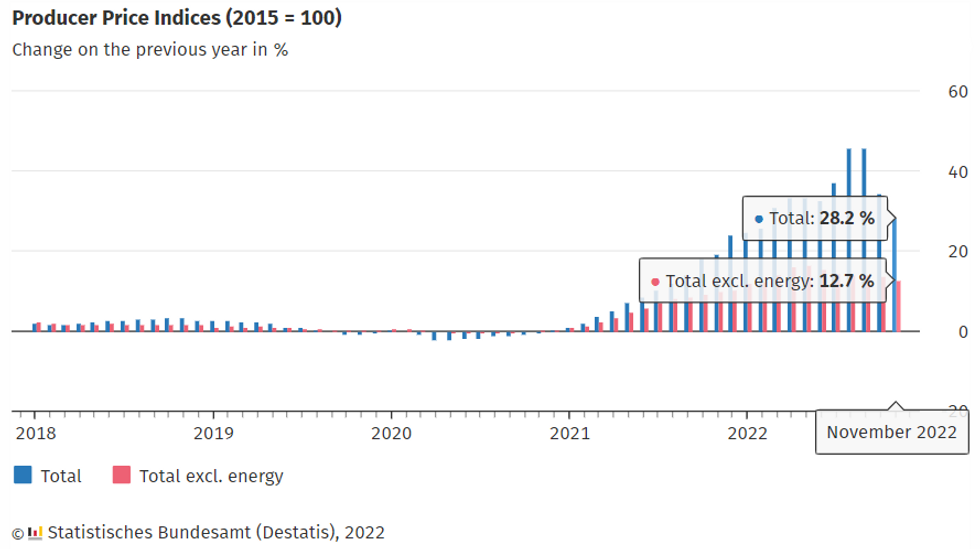

GERMANY NOV PPI -3.9% M/M (FCST -1.7%); OCT -4.2% M/M

GERMANY NOV PPI +28.2% Y/Y (FCST +31.1%); OCT +34.5% Y/Y

- Factory-gate inflation recorded a more pronounced decline than anticipated in November. Prices fell by -3.9% m/m and 6.3pp on the annualised print to +28.2% y/y.

- This is the lowest year-on-year reading since February and a substantial slowdown from the Aug-Sep record peak of +45.8% y/y. Lower energy prices and weak demand conditions are evidently feeding through into easing price pressures.

- Falling energy prices remain the key downward driver (down 9.6% m/m), however, core PPI also showed continued signs of easing. Ex. energy, annualised PPI slowed for the sixth consecutive month, cooling by 1pp to +12.6% y/y.

- Higher food prices pushed non-durable goods prices up by +0.2% m/m, whilst intermediate goods prices moderated by -0.7% m/m, helped by lower metal prices.

- The December manufacturing PMIs suggest continued slowing in PPI into year-end. Aggregate eurozone PPI figures for November are due on Jan 5 and are projected to follow a similar trajectory.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok