Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CONSUMER CYCLICALS

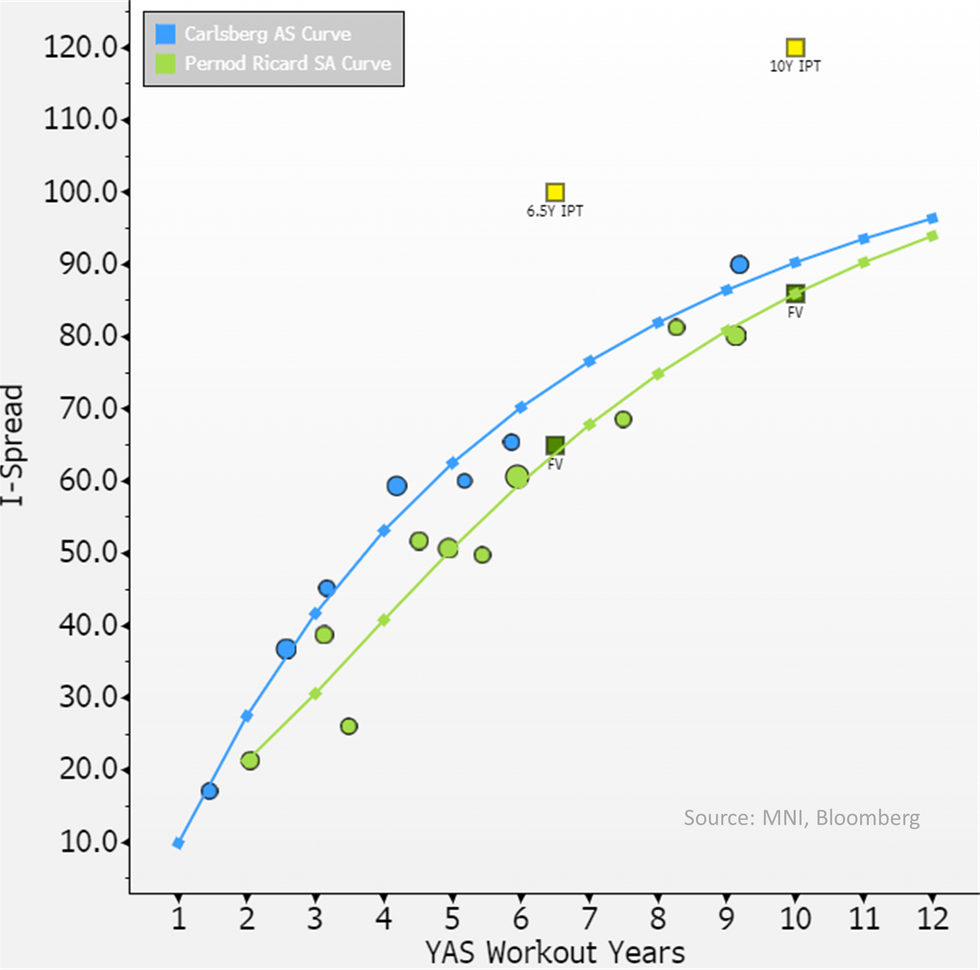

6.5Y FV +65 (IPT+100) & 10Y +86 (+120) - coming-in line.

- Similar to Danone on Friday, hard to get excited about RIFP's secondary. We flagged in Mid-Feb it was trading tighter than brewer curves despite its higher exposure to China (exposed to trade policy changes) - China was down 9% in Q3 on "challenging macro". Its moved wider of Heineken since but still inside Carlsberg - which we see no reason for.

- Q3 results were weak though volumes did increase, FY guidance is left broad, medium term guidance left unch and is firmer.

- Net leverage was at 3.3x in 1H24 - we don't see that moving close to FY23 levels (2.7x) yet - Moody's already had 2.7x at top end of its threshold - we don't expect downgrade for now - mgmt did cut back on buybacks but interim dividend did look a tad above normal last week.

- Negative outlook from Moody's is a possibility particularly on still weak US/China sales in Q4.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok