Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

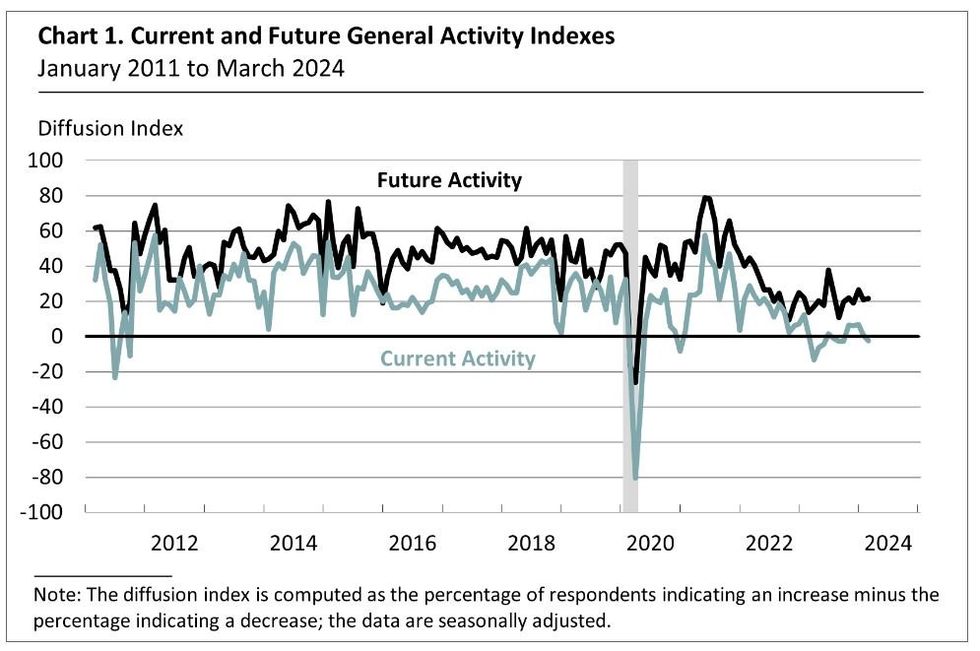

The Philadelphia Fed's Nonmanufacturing Business Outlook Survey showed a negative turn in activity in the region in March, coming in at -18.3 vs -8.8 prior.

- That was the lowest print since April 2023 and included fairly weak details: new orders remained negative, sales/revenues fell to a near-zero reading, full-time employment growth was "less widespread", and the price indexes "continued to indicate overall increases in prices".

- The current activity diffusion index fell to -2.3, the first negative reading since October 2023, from 0.8 in February.

- The most positive aspect of the report was in the future general activity indices which "continued to suggest firms expect growth over the next six months", at 21.7 (fairly steady from 21.2 prior).

- The special questions are often of note in these surveys: in response to "How will your firm’s total sales/revenues for the first quarter of 2024 compare with that of the fourth quarter of 2023?", 22.4% of firms saw a decline of 10% or more; though overall, 46.9% reported an increase, with 36.7% reporting a decrease.

- Overall this was a weak report, though should be taken in the context of the usual volatility of the series.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok