Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

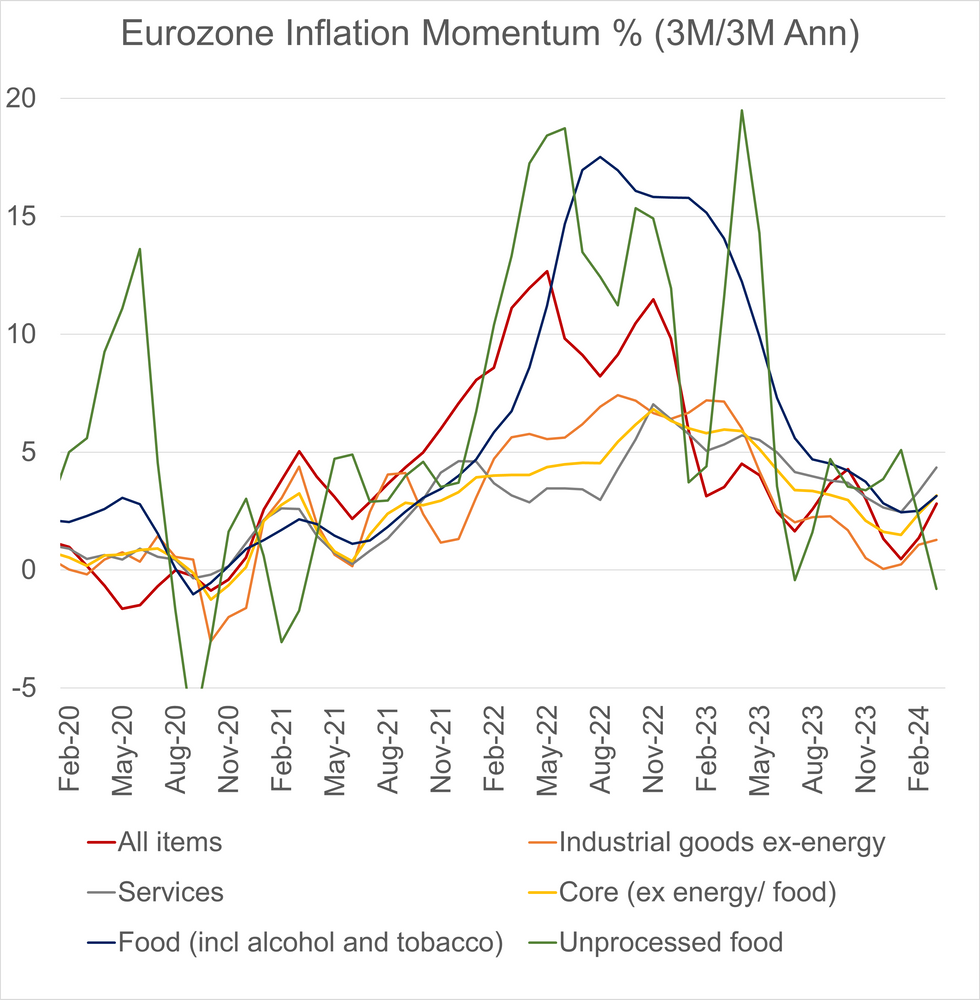

The ECB’s seasonally adjusted data indicates that core and headline inflation momentum rose for the second consecutive month in March. However, sequential monthly inflation was lower than February across core categories.

- On a SA sequential monthly basis, core inflation was 0.24% M/M (vs 0.38% prior), with services (0.42% M/M vs 0.46% prior) and NEIG (-0.02% M/M vs 0.12% prior) also moderating.

- A reminder that Bundesbank’s estimate of SWDA German CPI saw sequential services CPI at 0.4% M/M (as in February) while NEIG pulled back to 0.0% M/M (vs 0.4% prior).

- Core inflation momentum, measured as the 3m/3m saar, was 3.16% in March (vs 2.40% in February), the highest since September 2023.

- This was driven by rises in both services (4.35% vs 3.33% prior) and NEIG (1.29% vs 1.07% prior) momentum.

- The ECB’s data is working day and seasonally adjusted, but there remains some uncertainty as to how well the Easter-related calendar effects have been accounted for.

- In their inflation preview, JP Morgan, found that “the [ECB’s] seasonal adjustment (unsurprisingly) does not correct the noise generated by the early timing of Easter”.

- Nonetheless, the strength in services inflation (on an annual NSA and inflation momentum basis) may prompt the ECB to tone down expectations of a June rate cut at next week’s meeting and continue to maintain a data dependent approach until key Q1 macroeconomic data is released.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok