Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMAN DATA

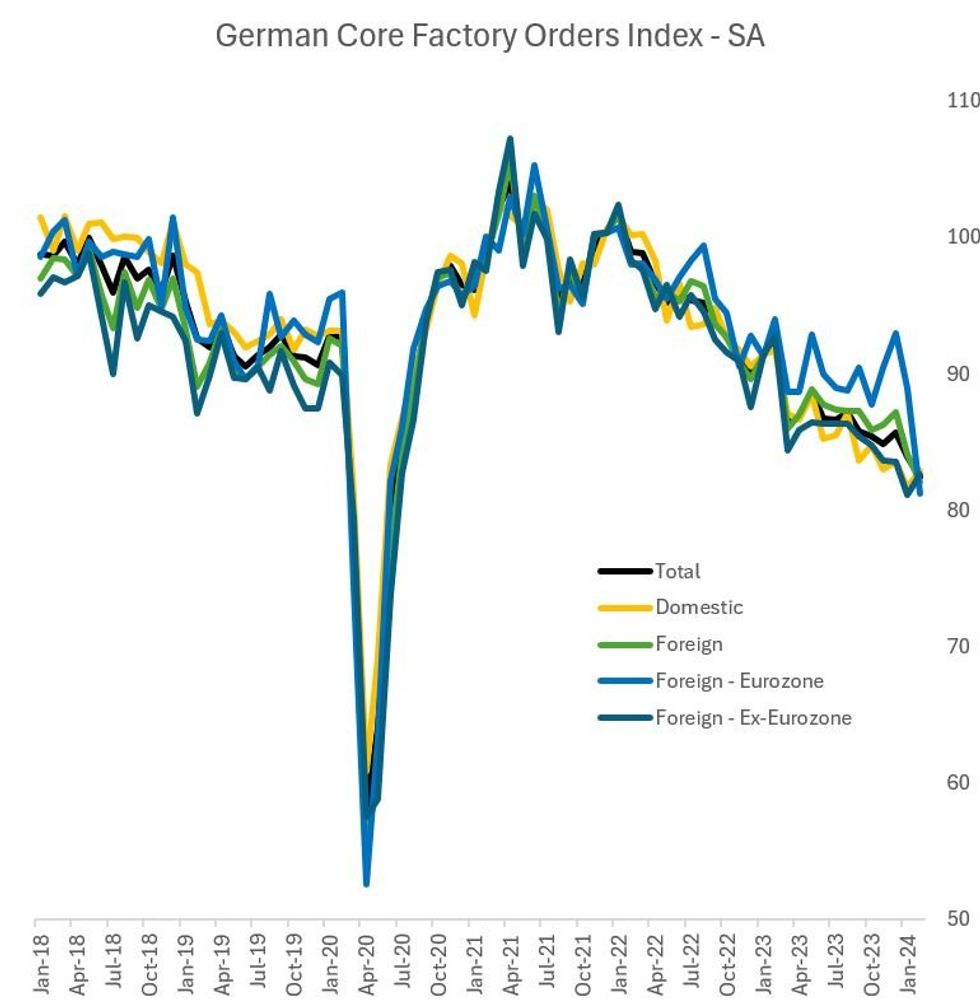

German factory orders rose 0.2% M/M in February on a price/seasonally/calendar adjusted basis, softer than the 0.7% expected and an even bigger downside miss vs consensus when considering a downward revision to January (by 0.1pp to -11.4%). This leaves factory orders more than 10% lower on a Y/Y working day adjusted basis, and while the headline number shows some stabilisation in the beleaguered industrial sector, the underlying trend in early 2024 remains to the downside.

- Core (ex-large ticket items) orders, a better measure of underlying activity, fell by 0.8% M/M after -3.0% in January - the 5th contraction in 6 months. The breakdown showed domestic core orders actually fairly robust at +1.5%, the biggest gain in 6 months (-2.3% prior). Instead it was foreign orders that dragged down the overall index, falling by 2.4% M/M after -3.6% in January. Eurozone orders led the drop, plummeting by 8.8% M/M, after -4.3% in January (foreign ex-Eurozone orders actually rose for the first time in 9 months).

- Outside of the early pandemic months of 2020, this was the biggest single-month fall in core Eurozone factory orders since at least 2010. Overall (non-core) new orders from the Eurozone fell 13.1% (after -24.3% in Jan), with total ex-euro up 7.8% and domestic up 1.5%.

- It's unclear what spurred this drop, particularly as eurozone-wide surveys suggest a nascent rebound in demand and industrial production in 1Q 2024. While the drop in overall orders is clearly linked to a pullback in capital goods orders after a surge in December on a one-off contract, the core decline will be concerning if not reversed in the months ahead.

- Manufacturing turnover rose 2.2% M/M, vs -5.2% in January - the latter of which reflects major revisions from -2.0% prior (autos and machinery/equipment saw large revisions). While there is no consensus for this figure, it could underpin expectations for continued growth in industrial production in Monday's release (currently +0.5% M/M expected vs +1.0% in Jan).

- Overall though there is no convincing sign of a turnaround in German factory activity, with the manufacturing PMI falling to a 5-month low in February and the March EC manufacturing confidence survey plumbing the lowest levels since the pandemic.

Source: Destatis, MNI

Source: Destatis, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok