Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

The official PMIs, in aggregate, suggest China's economy lost momentum in July, with the composite index slipping to 51.1 (from 52.3). However, the manufacturing reading beat expectations, with some positive details as well. The market may also look through the weaker services read, given efforts in recent weeks to boost consumption growth and potentially easier housing market restrictions. The market reaction has generally been positive post the prints, with local equities tracking higher, CNH and AUD firmer (albeit away from best level).

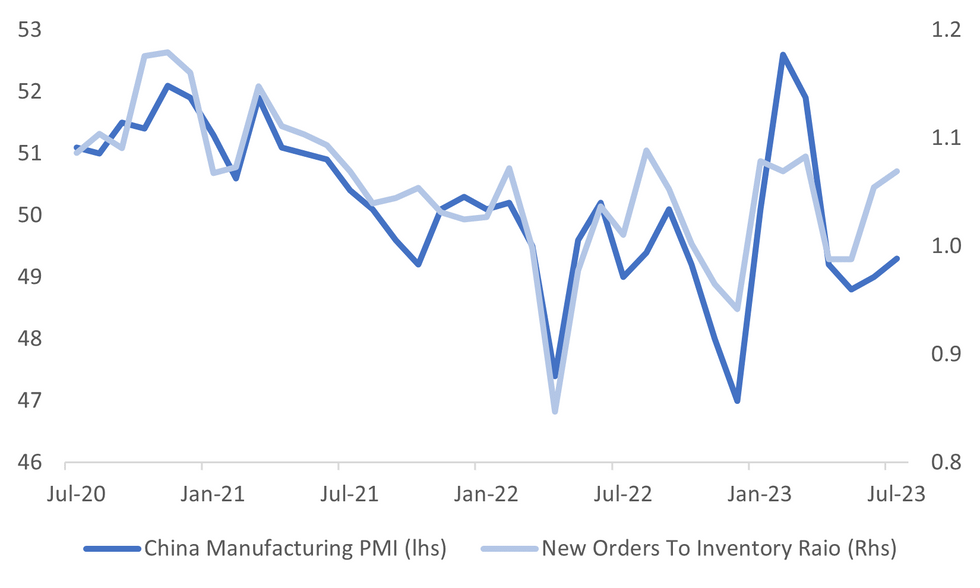

- The manufacturing PMI printed a touch above market expectations (49.3, 48.9 Bloomberg consensus). This was also a slight improvement on prior outcome of 49.0 in June. The detail showed steady output (50.2, 50.3 prior), but new orders bounced to 49.5, the highest since March of this year.

- The new orders to inventory ratio climbed back to early 2023 highs, which suggests we could see further improvement in the headline index in the near term, see the chart below.

- Other detail was less positive though. The employment index was down a touch to 48.1, while new export orders softened to 46.3.

- Input and output prices spike though. Input prices to 52.4 from 45.0, with firmer commodity prices likely playing a role. By scale of enterprise, we saw the most notable improvement in the small sector, albite from a low base, to 47.4 from 46.4.

Fig 1: China Manufacturing PMI Index Versus New Orders To Inventory Ratio

Source: MNI - Market News/Bloomberg

- On the non-manufacturing side, we saw a decent downside miss of 51.5, versus 53.0 forecast (53.2 prior). The detail showed weaker new orders (48.1 versus 49.5 prior), while employment slipped to 46.6 from 46.8. Overall, this suggests that the services side lost further momentum in July.

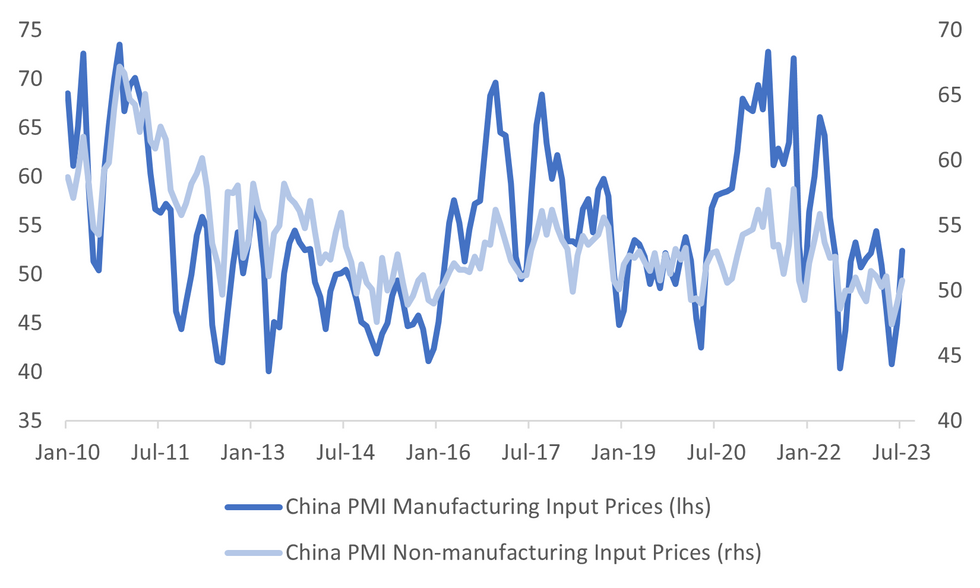

- In terms of prices, we saw a decent bounce in input and selling prices, which was a similar result to manufacturing.

- The second chart below plots input measures for both the manufacturing and non-manufacturing sides. This is line with a firmer spot commodity price backdrop in July, and at the margin may calm some fears around weaker China inflation for H2.

Fig 2: China Manufacturing and Non-manufacturing PMIs Input Price Indices

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.