Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

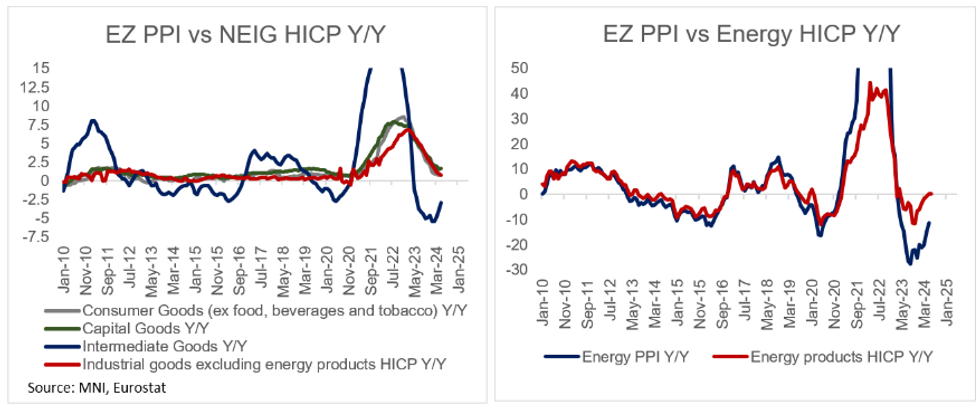

Eurozone PPI for May remained in deflation for the twelfth successive month, although the energy component saw another increase in the Y/Y rate for the third consecutive month (entirely driven by base effects). This pushed the Y/Y PPI figure up to -4.2% Y/Y, although a tenth below consensus (vs -5.7% prior).

- On a monthly basis PPI also fell a tenth more than consensus had expected, down 0.2% (vs -0.1% consensus, -1.0% prior).

- The energy component remained in deflation at -11.4% Y/Y, the highest since April 2023, although as noted above this was driven by base effects as on a monthly basis it saw its seventh consecutive fall at -1.1% M/M.

- Intermediate goods also remained in deflation for the thirteenth consecutive month, printing -2.9% Y/Y (vs -3.9% prior). Although the pace of deflation continues to decline as the M/M reading was positive for the third successive month at 0.1% M/M.

- Meanwhile, Capital goods, durable and non-durable consumer goods saw prices increase on an annual basis, with both Capital goods and Non-durable consumer goods edging up to 1.6% Y/Y (vs 1.5% prior) and 1.1% Y/Y (vs 1.0% prior). Durable consumer goods disinflated to 0.5% Y/Y (vs 1.0% prior) - returning to the August 2017 lows. This could potentially lead to further disinflation for non-energy industrial goods in the coming months HICP readings - although at some point that disinflation would still be expected to stall.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok