Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

ECB

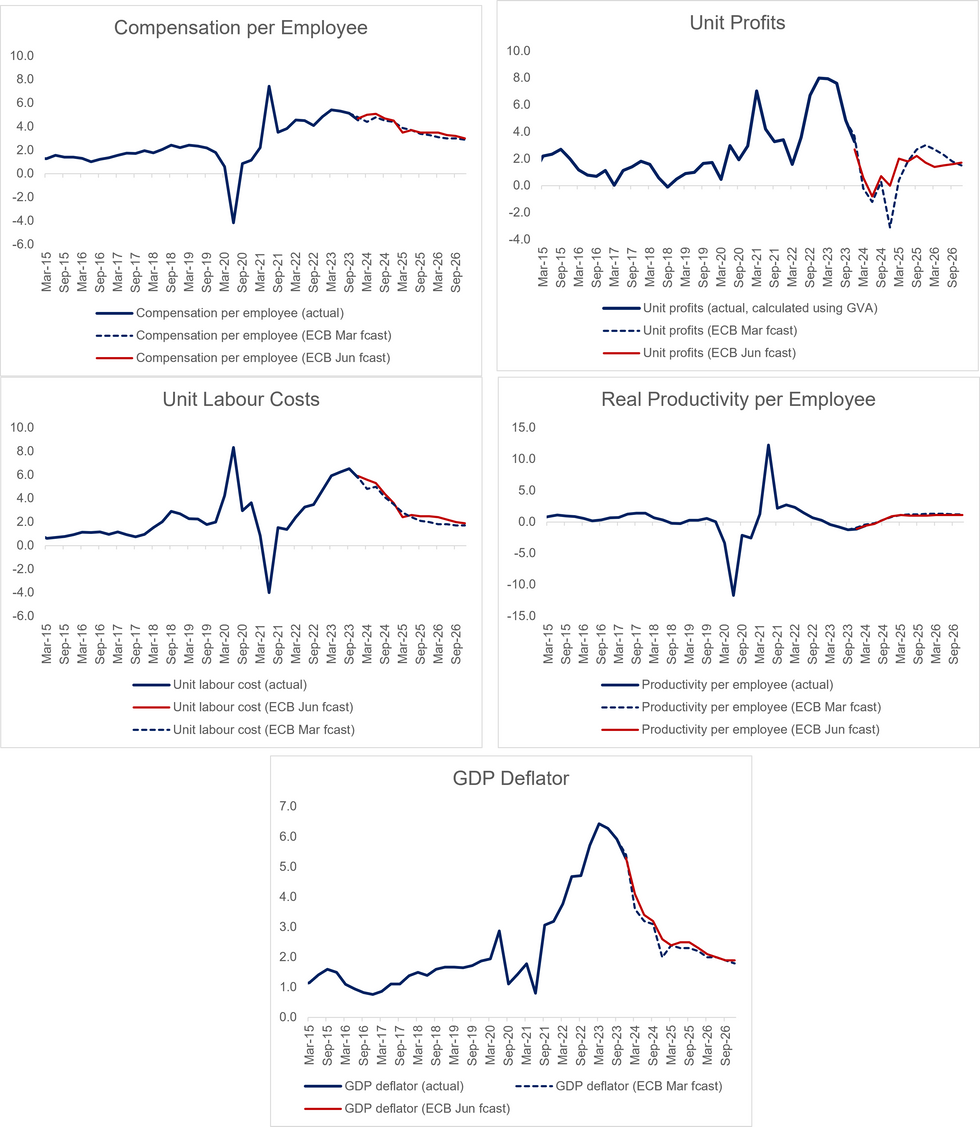

The ECB’s June macroeconomic forecasts record an upward revision to GDP deflator growth through 2024, with unit labour cost and unit profit growth revised higher.

- The higher unit labour cost projection comes as 2024 compensation per employee was revised higher and real productivity per employee was revised lower.

- This likely drove the upward revision to the ECB's core inflation forecasts, which were above analyst's median estimates coming into the decision.

- The upward revision to compensation per employee growth “reflects the impact of incoming data, a slightly better cyclical position and a higher wage drift, and is in line with a tighter labour market, especially towards the end of the projection horizon”.

- 2024 annual unit profit growth was revised 1.1pp higher relative to the March forecasts.

- However, the ECB still note that unit profits are “expected to remain notably below growth in unit labour costs throughout 2024, which implies that profit margins are buffering the relatively strong labour cost growth”.

- This expected dynamic is relatively unchanged compared to March, though the GDP deflator is now projected to moderate at a slower pace.

- Q1 deflator growth is seen at 4.1% Y/Y (vs 5.3% in Q4 2023 and a 3.6% forecast in the March projections).

- Tomorrow sees the release of the final Eurozone national accounts for Q1, which will allow us to benchmark the ECB’s latest projections immediately.

- A reminder that the June projections were compiled by Eurosystem staff (i.e. from national central banks), not the ECB staff themselves.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok