Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

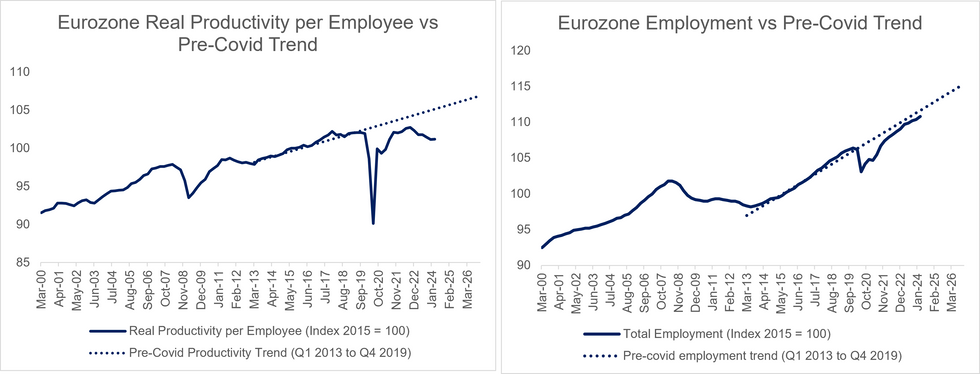

The preliminary estimate of Eurozone Q1 employment indicated growth of 0.3% Q/Q and 1.0% Y/Y. This leaves the employment index tracking a touch below the pre-covid trend. However, real productivity per employee was estimated at 0.0% Q/Q and -0.6% Y/Y. In its March projections, the ECB forecasted this metric at -0.4% Y/Y.

- All else equal, the weak productivity development increases the risk of inflation stickiness, particularly within core services components (where wages form a large proportion of total costs).

- Real productivity per employee remains well below the pre-covid trend. Yesterday, the ECB’s Knot noted the importance of the Eurozone’s weak productivity growth in pushing up unit labour costs post-covid.

- Knot, speaking on a panel alongside Fed Chair Powell, said that the Eurozone’s policies to protect jobs during the covid crisis hampered the productivity-enhancing labour market reallocation that was seen in the US.

- The preliminary GDP release does not contain information on hours worked, or the GDP deflator and its components. The ECB’s central scenario is that still-strong unit labour cost growth will be absorbed by a moderation in unit profits, enabling GDP deflator growth to soften. This is a dynamic already seen in Spain, where the relevant data for Q1 is available.

- As such, today’s data won’t stand in the way of the likely June cut, but will need to be taken alongside the final Q1 GDP release (on June 7) to determine any relevant signals for the path of rates beyond that meeting.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok