Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

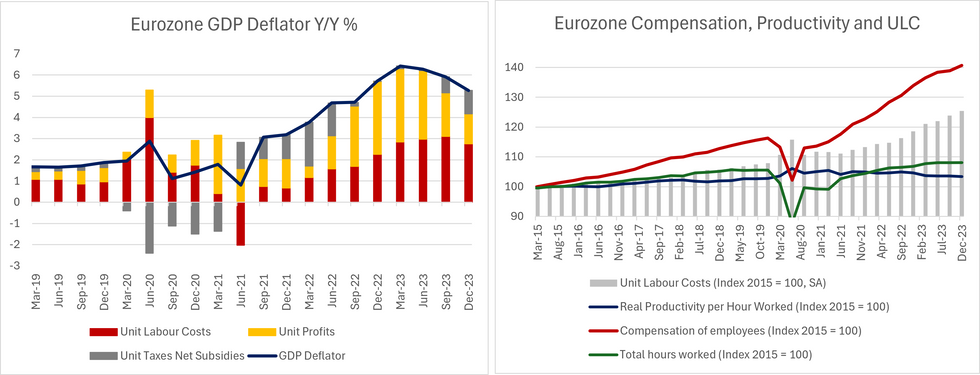

The final Q4 national accounts confirmed a deceleration of the Eurozone GDP deflator to 5.3% Y/Y (vs 5.9% in Q3). Details suggest that unit profits buffered rises in unit labour costs (ULCs), consistent with the ECB's central projections in its updated forecasts.

- However, the Q4 readings of wage growth and productivity remain incompatible with the 2% HICP inflation target, underscoring the majority of the Governing Council's view that an analysis of Q1 2024 developments is required before starting the policy easing cycle.

- The ECB's March macroeconomic projections looked for a Q4 GDP deflator rise of 5.4% Y/Y.

- Of the 5.3% Y/Y rise in the GDP deflator, MNI's calculations suggest ULCs contributed 2.75pp (vs 3.11pp in Q3), while unit profits contributed 1.42pp (vs 2.04pp in Q3).

- ULCs rose 5.8% Y/Y in Q4 (vs 6.5% in Q3) and 1.3% Q/Q (vs 1.6% prior). The Y/Y rise was in line with the ECB's projections.

- The moderation in ULCs came after the growth in total compensation of employees fell to 5.0% Y/Y from 6.3%, while real productivity per hour worked (-1.2% Y/Y fall) and total hours worked (1.2% Y/Y rise) broadly offset each other.

- Total compensation per employee, which the ECB forecasts rather than total compensation overall, moderated to 4.6% Y/Y (vs a downwardly revised 5.1% prior). Yesterday's projections saw this at 4.8% Y/Y.

- As indicated in the preliminary national accounts last month, real productivity per employee was -1.1% Y/Y, below the March ECB forecast of -0.9% Y/Y.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok