Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

PORTUGAL

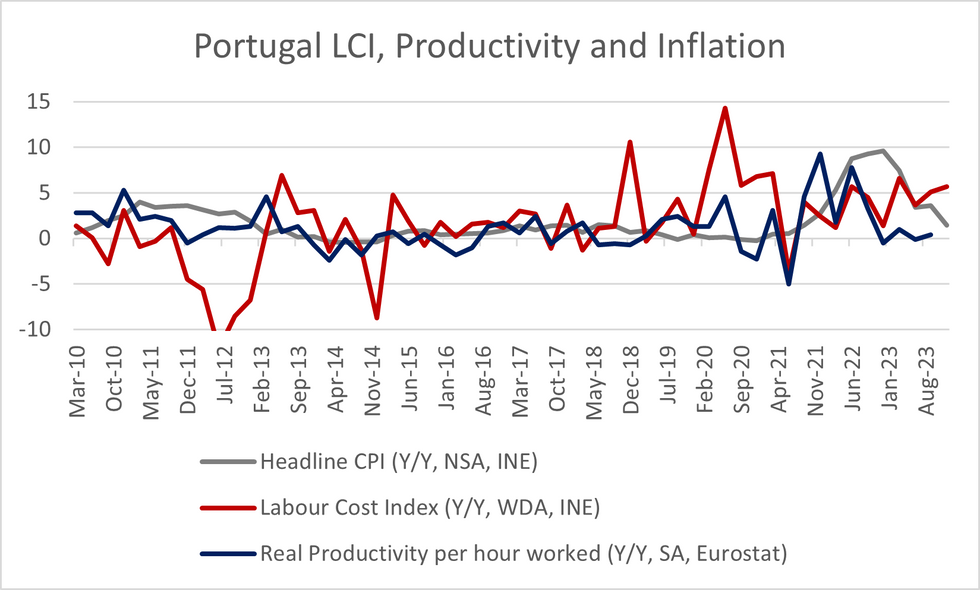

The Portuguese Q4 Labour Cost Index (per hour worked, WDA) rose +5.7% Y/Y, from an upwardly revised +5.1% prior. While Portugal is not a major Eurozone economy in terms of weighting (for context, it is only 2.4% of the EZ 2023 HICP weighting), it provides support to the view that the ECB will need to assess Q1 '24 wage pressures before comfortably being able to begin their easing cycle.

- The rise in the LCI came as average costs per employee rose at a faster rate than total hours worked per employee, with the former rising +6.1% Y/Y (vs +6.6% prior) and the latter +0.4% Y/Y (vs +1.6% prior).

- Breaking down the Q4 LCI figure, wage costs (per hour worked) rose +5.5% Y/Y (vs +4.8% prior) while other labour costs (per hour worked) rose +6.8% Y/Y (vs +6.4% prior).

- At a sector level, services saw the largest increase in wage costs per hour (+5.8% Y/Y) though the smallest rise in other labour costs (+6.1% Y/Y).

- With respect to inflation, we see that LCI growth has outpaced real productivity per hour worked since Q3 '22. This will have pushed up unit labour costs and has likely contributed to sticky services inflation in Portugal. Services CPI rose to 4.51% Y/Y in January '24 (vs 4.15% in December).

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok