Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

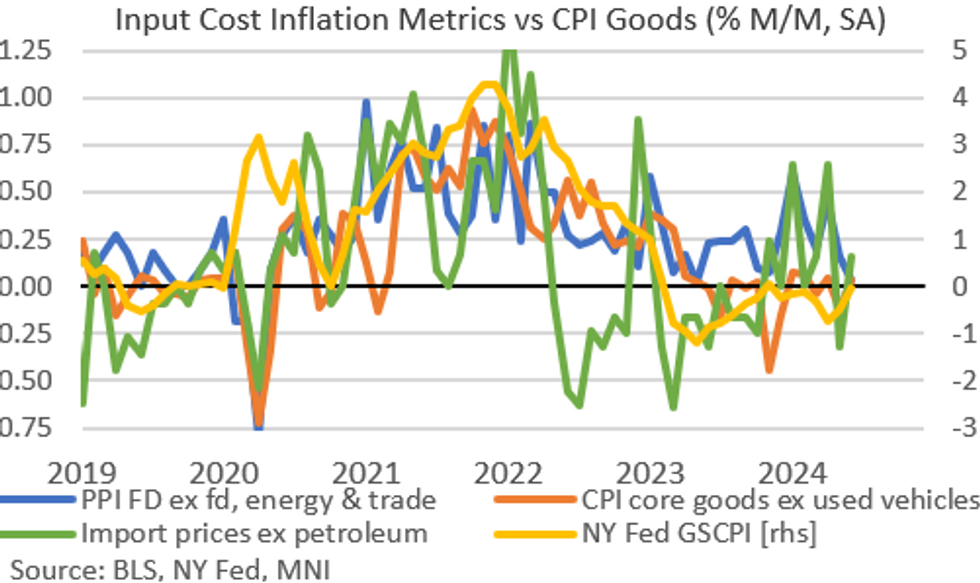

Import price inflation was stronger than expected in June, coming in flat M/M (-0.2% expected, -0.2% prior rev from -0.4%), with the ex-petroleum prices +0.2% (-0.2% expected, -0.3% prior, unrev). Export prices conversely were softer than expected, at -0.5% M/M (-0.1% expected, -0.7% prior rev from -0.6%).

- The upside import surprise has two potential implications for monetary policy. The first is the read-through to June PCE inflation, for which the import price index provides the final albeit very small piece of the puzzle after CPI and PPI.

- The second is that the Fed appears to have been concerned with stubbornness in import price inflation earlier this year (the June FOMC meeting minutes noted "A few participants also highlighted the strong increases recorded this year in core import prices").

- That comment came after a 0.6% increase in April, which appeared to have been mitigated after the meeting by the -0.3% drop recorded for May, but prices are now back in positive territory.

- These monthly figures are erratic and not seasonally adjusted so should be taken with a grain of salt. But while import prices are not increasing at a worrying pace, at the margins it takes away some of the disinflationary impulses seen previously from imported goods.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok