Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

FED

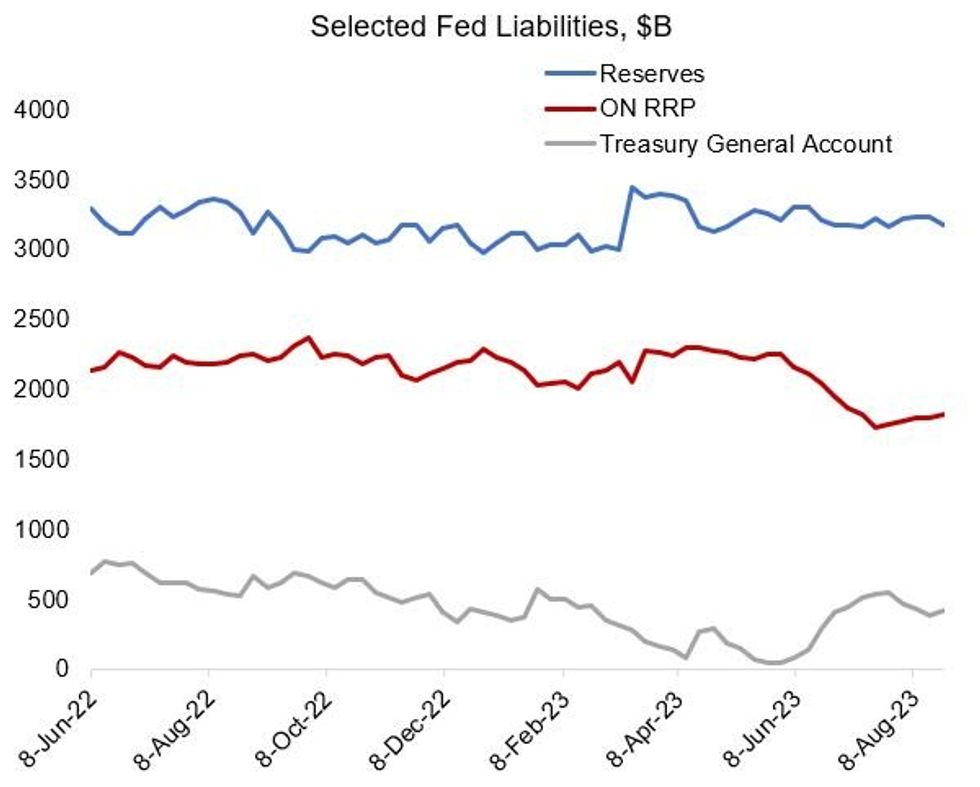

Despite concerns over bank reserve scarcity emerging as the Treasury rebuilds its cash pile at the Fed and QT continues, there is no evidence that this is happening so far. System reserve levels are basically unchanged at $3.2T since the debt limit was suspended in early June (down $28B at $3.18T), with the TGA up $368B and overnight RRP usage down $438B. The ostensible reason for this is the benign scenario so far for reserves: soaring Bill supply has been met by demand from money market funds parked at ON RRP.

- St Louis Fed economists are the latest to weigh in on the topic, in a note out this week called “The Mechanics of Fed Balance Sheet Normalization” (link here).

- "As QT-II continues at an accelerated pace, the Fed is likely to reassess the optimal level of reserves in the near future...Earlier this year, Governor Christopher Waller suggested that ON RRP balances could drop to zero without impairing market liquidity. If this is the case, the Fed can continue QT for some time without draining reserves too low. However, there is a risk that ON RRP balances remain sizable and bank reserves represent the majority of the contraction of Fed liabilities as QT continues. In this case, regulatory banking constraints could start binding sooner than expected…”

- They suggest that optimal reserves (before liquidity constraints begin to force money market rates higher) could be as low as $1.9-2T, though “desired liquidity may be something closer to 10% to 12% of nominal GDP ($2.7 trillion to $3.3 trillion), with the current level of reserve balances already around the upper bound of the estimate”.

- Pressure on ON RRP will continue with Treasury’s $650B end-Sept cash target implying continued heavy bill issuance ahead, and the real test will begin emerging closer to then – but there’s no evidence for concern just yet.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok