Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

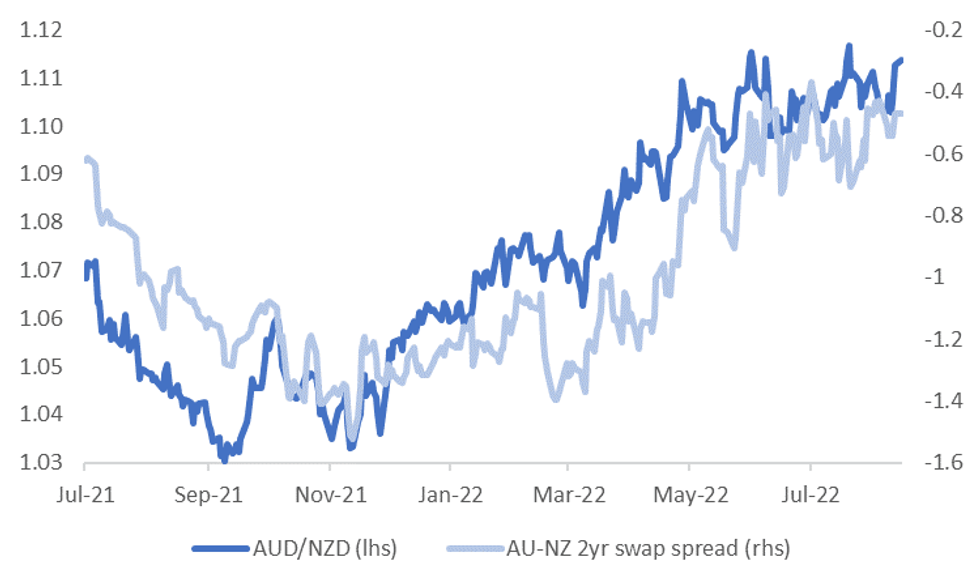

AUDNZD

The AUD/NZD cross is close to a move above 1.1150. This is not too far away from previous YTD highs, which was just shy of 1.1200 in late July. Going back to early May, the cross has had a number of attempts to break higher but has run out of momentum in the 1.1150/1.1200 range.

- As we noted late last week, it may take relative yield differentials to move convincingly higher to see the cross break above 1.1200.

- Since the RBNZ last week, yield spreads have moved in AUD's favor, but arguably the move higher in the cross has outperformed these trends, see the chart below.

- The AU-NZ 2yr swap spread is back to -46bps, up from last week's lows, but it remains well within recent ranges.

Fig 1: AUD/NZD Versus AU-NZ 2yr Swap Spread

Source: MNI/Market News/Bloomberg

Source: MNI/Market News/Bloomberg

- It's the same story in the government bond yield space. Interestingly, the levels correlation between AUD/NZD and yield differentials in the pass month is negative. It remains strongly positive though for 2022 as a whole and higher than other macro drivers.

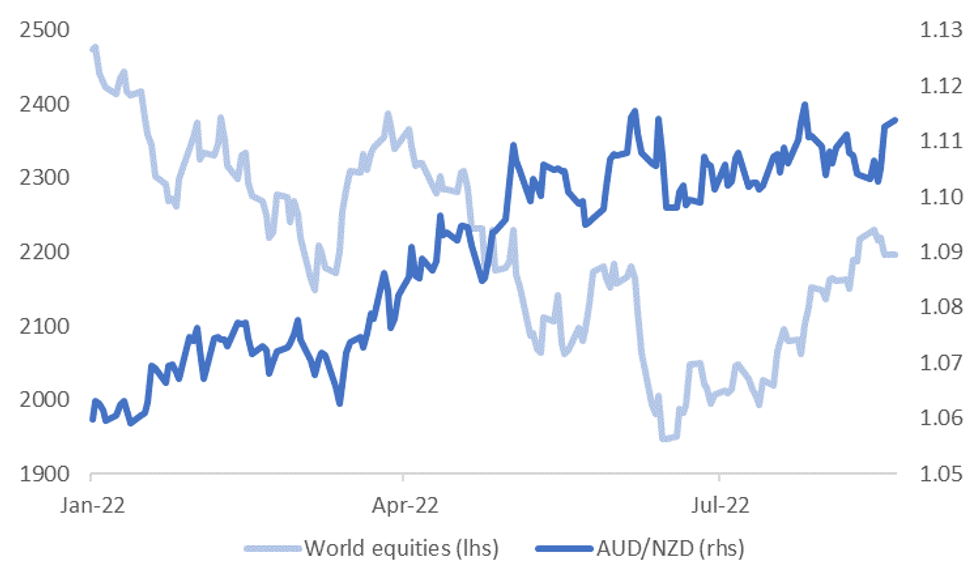

- One possible driver of the rebound in AUD/NZD is the recent decline in global equities. The second chart below plots the cross against global equities performance. The correlations here are negative.

- This likely reflects the fact that Australia's trade position is in a much stronger position relative to NZ's, and therefore in a better position to withstand external headwinds from a current account funding standpoint.

- However, our sense is that risk off in equities may only take the AUD/NZD cross so far. The more risk off we see in equities the greater the risk that this spills over into commodity prices, all else equal, particularly if the source of risk aversion is related to the health of the global economy.

- AUD/NZD maintains a positive correlation both with relative commodity prices to NZ and aggregate commodity prices. Correlation levels are noticeably lower for the past month though.

Fig 2: AUD/NZD & Global Equities

Source: MNI/Market News/Bloomberg

Source: MNI/Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok