Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

MNI (London)

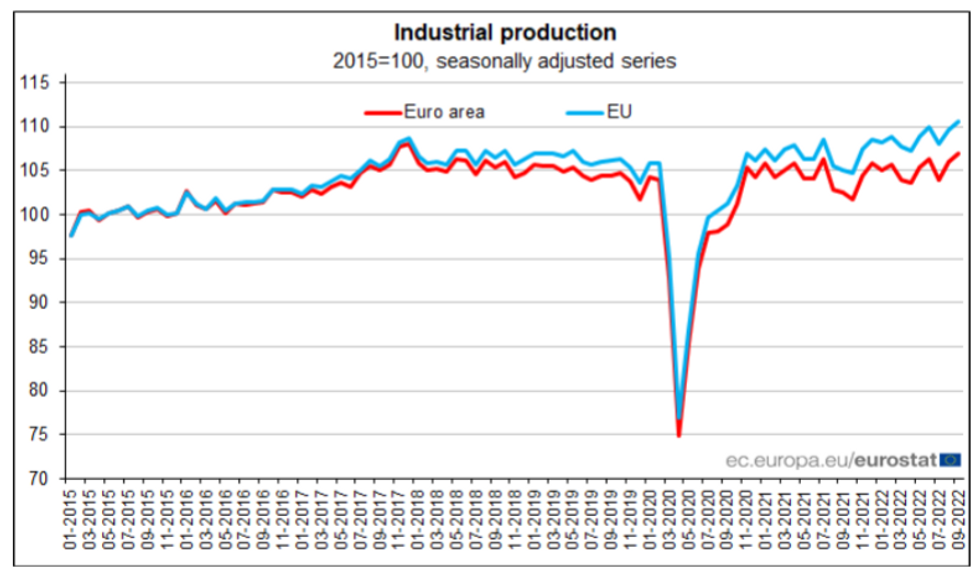

EUROZONE SEP IND PROD +0.9% M/M (FCST +0.5%); AUG +2.0%r M/M

EUROZONE SEP IND PROD +4.9% M/M (FCST +3.0%); AUG +2.8%r Y/Y

- Euro area industrial production recorded an upside surprise in September, expanding by +0.9% m/m after robust +2.0% m/m growth in August. Compared to 2021, September IP grew by +4.9% y/y, in part reflecting Covid base effects of slow production. Germany was a key upwards driver for the bloc.

- The month reported substantial divergence across categories. Non-durables were up +3.6% m/m, implying stronger domestic agricultural production as global food prices soar.

- The +1.5% m/m uptick in capital goods is an optimistic indication of robust investment appetite towards the end of Q3. Yet the -0.9% m/m fall in consumer and intermediate goods reflects cooling current demand.

- Looking forward, the euro area manufacturing PMI signalled a fourth month of contraction in October. Output fell at the fastest pace since the 2020 pandemic onset as demand dissipated. All eyes will be on developments in energy markets headed into the winter months, as the energy-intensive industry watches profit margins rapidly shrink.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok