Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SWEDEN

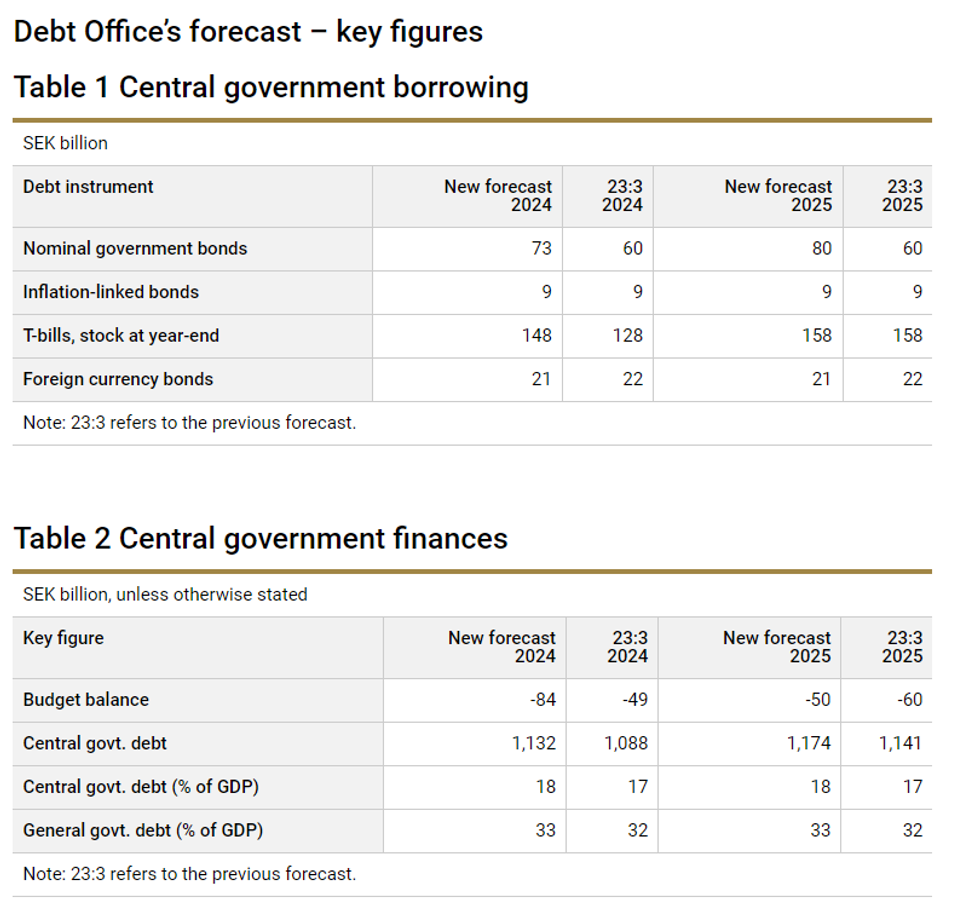

The Swedish National Debt office's revised borrowing forecast indicates an increase in bond issuance and debt levels in both 2024 and 2025, with the 2024 increase in part due to the Riksbank's recapitalisation.

- As with the last publication in October, a budget deficit is forecast in both 2024 and 2025, but the revised set of forecasts see the distribution of the deficit more heavily weighted to 2024: 2024 budget balance seen at -SEK84bln (vs -SEK49bln prior) and 2025 seen at -SEK50bln (vs -SEK60bln prior).

- Per the press release: "This year’s deficit is among other things due to an assumption of a capital contribution of SEK 40 billion to the Riksbank, as well as to higher expenditure in other areas and slow economic growth".

- The Recapitalisation is accounted for in the 2024 debt increase, even as the "Debt Office assumes that the injection of capital will occur in late 2024".

- A reminder that the SEK40bln is in line with the Riksbank's latest estimate of the required capital injection. In a recent piece, we assigned a 70% probability that they would petition for a SEK40bln injection to the Riksdag in March (though there is some risk they petition for a larger amount, see here).

- The increase in central Government debt is funded via nominal government bonds (increasing issuance volumes to SEK3.5bln per auction as of March and then SEK4bln as of August, from SEK3bln prior) and treasury bills.

- The NDO estimates a small increase in the central/general government debt to GDP ratio, but this remains at a historically low level.

- The NDO's macroeconomic forecasts appear more optimistic than the Riksbank's November MPR: GDP is forecast at +0.5% Y/Y (vs Riksbank -0.2% Y/Y) in 2024 and +2.3% Y/Y (vs Riksbank +2.1% Y/Y) in 2025, while unemployment is forecasted lower than the Riksbank in both years.

- The NDO sees CPIF inflation at 1.7% Y/Y in both 2024 and 2025 (vs Riksbank 2.3% in 2024 and 1.7% in 2025).

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok