Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

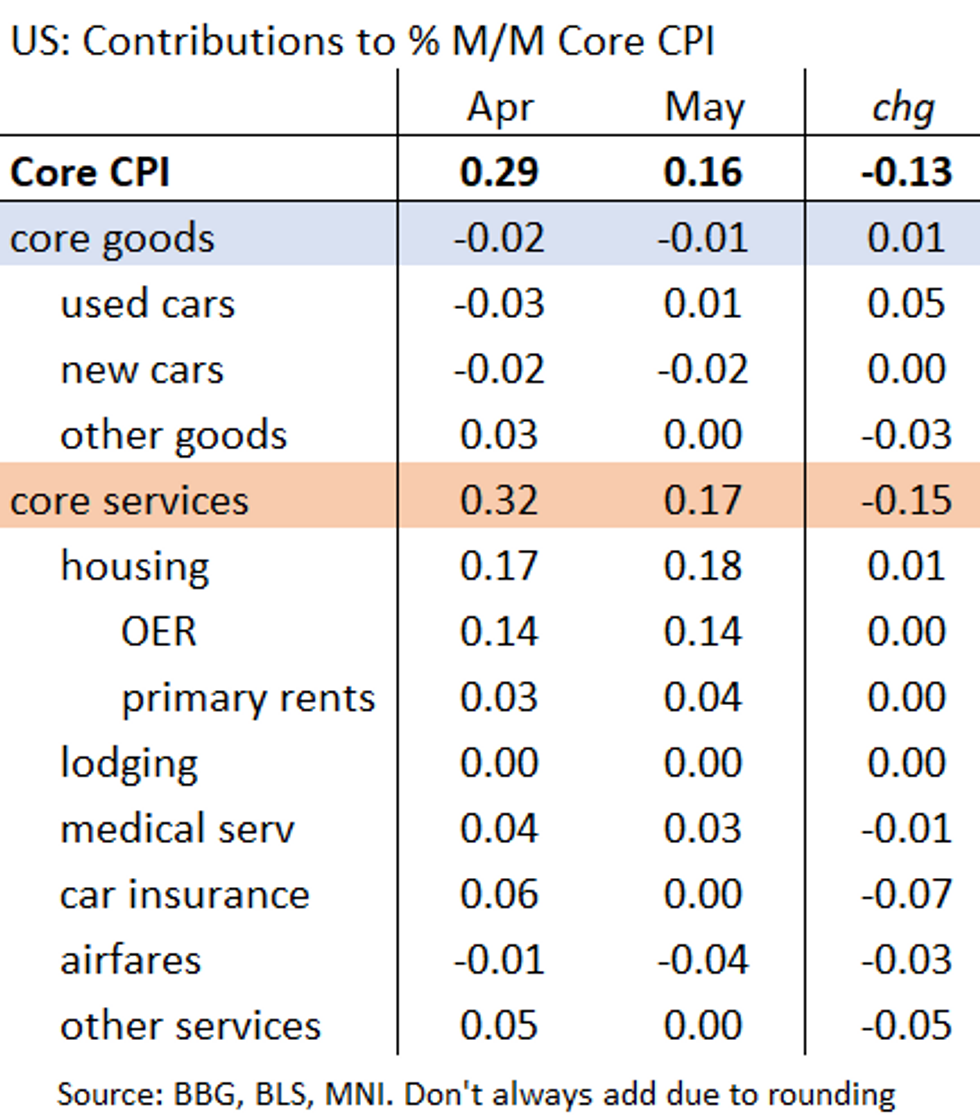

The core CPI inflation pullback was, obviously, driven by a drop in core services outside of housing, ie supercore. See table below.

- Core services overall once again contributed more than 100% to the core CPI reading of 0.16% (at 0.17pp), with core goods again in slight deflation (subtracting 0.01pp from core CPI).

- Airfares subtracted 0.04pp alone from core CPI in the softest reading since July 2023; car insurance made no contribution BUT versus April, it made 0.07pp less of a contribution (and it was the weakest auto insurance inflation since Oct 2021).

- Lodging/medical services contributed about the same to core as they did before.

- Services outside of the major categories contributed nothing to core CPI, 0.05pp less of a contribution than in April.

- Note for core goods, used car inflation picked up a little more than expected, adding 0.01pp to core (vs -0.03pp last month). But this was offset elsewhere for the in-line core goods figure of 0.0% M/M (-slightly negative unrounded).

- Apparel pulled back as expected, to a 4-month low -0.3%, pulling down core by under 0.01pp.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok